You might also like

- Tolentino V Sec of Finance DigestsDocument5 pagesTolentino V Sec of Finance DigestsDeb Bie100% (8)

- Question 16Document5 pagesQuestion 16Yulfaizah Mohd YusoffNo ratings yet

- 11 CUA vs. TANDocument4 pages11 CUA vs. TANRicardo100% (1)

- Motion To Release Cash Bond - SampleDocument2 pagesMotion To Release Cash Bond - SampleDeb Bie100% (6)

- Gokongwei Vs Sec DigestDocument2 pagesGokongwei Vs Sec DigestHaziell Pascua94% (18)

- Colegio Medico-Farmaceutico v. LimDocument2 pagesColegio Medico-Farmaceutico v. LimRoger Montero Jr.100% (1)

- Reburiano vs. CA G.R. No. 102965Document1 pageReburiano vs. CA G.R. No. 102965Marianne AndresNo ratings yet

- Central Textile Mills, Inc. v. National Wages and Productivity CommissionDocument1 pageCentral Textile Mills, Inc. v. National Wages and Productivity CommissionEnzoGarcia100% (1)

- CASE DIGEST - Alabang Development Corporation VS Alabang Hills Village AssociationDocument2 pagesCASE DIGEST - Alabang Development Corporation VS Alabang Hills Village AssociationGladys Cañete100% (2)

- Florete vs. Florete (2016)Document2 pagesFlorete vs. Florete (2016)mjpjore60% (5)

- China Banking Corp. v. Court of Appeals, G.R. No. 117604, March 26, 1997 by Bryce KingDocument4 pagesChina Banking Corp. v. Court of Appeals, G.R. No. 117604, March 26, 1997 by Bryce KingBryce King100% (1)

- Republic Planters Bank Vs AganaDocument2 pagesRepublic Planters Bank Vs AganaHoven Macasinag100% (2)

- Agdao V MaramionDocument3 pagesAgdao V MaramionGlenn Mikko Mendiola100% (1)

- Sme Bank Inc v. de Guzman G.R. No. 184517Document3 pagesSme Bank Inc v. de Guzman G.R. No. 184517abbyNo ratings yet

- Affidavit of Own Recognizance SAMPLEDocument2 pagesAffidavit of Own Recognizance SAMPLEDeb Bie100% (2)

- Anderson Vs Ho Case DigestDocument3 pagesAnderson Vs Ho Case DigestDeb BieNo ratings yet

- ITC Johnston Complete Family Pack Font ListDocument2 pagesITC Johnston Complete Family Pack Font ListSenthuTu0% (1)

- Procedures For The Transfer of Shares of Stock From A Deceased Stockholder To Hisher HeirsDocument1 pageProcedures For The Transfer of Shares of Stock From A Deceased Stockholder To Hisher HeirsSittie Casanguan100% (1)

- Valley Golf & Country Club, Inc. v. Rosa Vda. de CaramDocument1 pageValley Golf & Country Club, Inc. v. Rosa Vda. de CaramCheCheNo ratings yet

- 43 Calatagan Golf Club, Inc. vs. Sixto Clemente, JR.Document2 pages43 Calatagan Golf Club, Inc. vs. Sixto Clemente, JR.Arthur Archie Tiu100% (2)

- Iglesia vs. LazaroDocument3 pagesIglesia vs. LazaroRhev Xandra Acuña100% (1)

- Lao VS lAODocument2 pagesLao VS lAOJuris Renier MendozaNo ratings yet

- Sales v. SECDocument3 pagesSales v. SECclvnngcNo ratings yet

- Provident International Resources Corporation V Joaquin T. Venus, Et Al. DigestDocument4 pagesProvident International Resources Corporation V Joaquin T. Venus, Et Al. DigestHannah RosarioNo ratings yet

- Rev. Luis Ao-As, Et Al. v. Court of AppealsDocument1 pageRev. Luis Ao-As, Et Al. v. Court of AppealsCheChe100% (1)

- Yujuico v. QuiambaoDocument2 pagesYujuico v. QuiambaoFrancisco Ashley AcedilloNo ratings yet

- Lim VS MoldexDocument2 pagesLim VS MoldexMark Anjo Atienza100% (1)

- Chemphil Export V CADocument3 pagesChemphil Export V CASef KimNo ratings yet

- Majority Stockholders of Ruby Industrial V LimDocument3 pagesMajority Stockholders of Ruby Industrial V LimPatrick Manalo100% (1)

- 064 Espiritu V PetronDocument2 pages064 Espiritu V Petronjoyce100% (1)

- Nava v. Peers MarketingDocument2 pagesNava v. Peers MarketingAnonymous 5MiN6I78I0No ratings yet

- #11knecht V United Cigarette Corp (p20)Document2 pages#11knecht V United Cigarette Corp (p20)hans50% (2)

- G.R. No. 210538, March 07, 2018 - Dr. Gil J. Rich, Petitioner vs. Guillermo Paloma III, Atty. Evarista Tarce and Ester L. Servacio, Respondents.Document2 pagesG.R. No. 210538, March 07, 2018 - Dr. Gil J. Rich, Petitioner vs. Guillermo Paloma III, Atty. Evarista Tarce and Ester L. Servacio, Respondents.Francis Coronel Jr.No ratings yet

- Yujuico vs. QuiambaoDocument3 pagesYujuico vs. QuiambaoNelia Mae S. VillenaNo ratings yet

- McLeod Vs NLRCDocument2 pagesMcLeod Vs NLRCTrish Verzosa100% (1)

- Mindanao v. WillkomDocument2 pagesMindanao v. Willkomjanatot100% (2)

- Pmi Colleges Vs NLRC DigestDocument1 pagePmi Colleges Vs NLRC DigestGin FranciscoNo ratings yet

- #13. Prime White Cement Vs IAC. DigestDocument2 pages#13. Prime White Cement Vs IAC. DigestHetty HugsNo ratings yet

- YazumaDocument3 pagesYazumaNympa VillanuevaNo ratings yet

- Lipat V Pacific BankingDocument3 pagesLipat V Pacific Bankingjojo50166No ratings yet

- Facts:: BSP v. Campa JR., G.R. No. 185979, March 16, 2016Document4 pagesFacts:: BSP v. Campa JR., G.R. No. 185979, March 16, 2016Wilfredo Guerrero III100% (1)

- Ching v. SubicBayGolfCountryClub GR 174353 10sep2014Document1 pageChing v. SubicBayGolfCountryClub GR 174353 10sep2014Bennet BalberiaNo ratings yet

- Filipinas Port Vs Go - DigestDocument2 pagesFilipinas Port Vs Go - DigestArmand Patiño Alforque100% (2)

- Vicente Ponce v. Alsons Cement Corporation and GironDocument1 pageVicente Ponce v. Alsons Cement Corporation and GironCheCheNo ratings yet

- Rosario v. CoDocument2 pagesRosario v. CoDanielle DacuanNo ratings yet

- Suldao vs. CIMECH Case DigestDocument2 pagesSuldao vs. CIMECH Case DigestEhem Drp60% (5)

- Cases Castillo Vs BalinghasayDocument4 pagesCases Castillo Vs BalinghasayBerch Melendez100% (1)

- Terelay Investment v. YuloDocument2 pagesTerelay Investment v. YuloKev BayonaNo ratings yet

- TENG v. SEC DIGESTDocument3 pagesTENG v. SEC DIGESTRoger Montero Jr.100% (6)

- Associated Bank v. CA and SarmientoDocument2 pagesAssociated Bank v. CA and SarmientoChedeng KumaNo ratings yet

- 08 TCL Sales Corp v. CADocument1 page08 TCL Sales Corp v. CAYvon BaguioNo ratings yet

- Turner V Lorenzo ShippingDocument2 pagesTurner V Lorenzo ShippingChic Pabalan67% (3)

- DIGEST. Complte. Turner V Lorenzo ShippingDocument2 pagesDIGEST. Complte. Turner V Lorenzo ShippingIamIvy Donna PondocNo ratings yet

- Yu Vs YukayguanDocument1 pageYu Vs YukayguanLindsay MillsNo ratings yet

- Wee v. Wee G.R 169345 25aug2010Document1 pageWee v. Wee G.R 169345 25aug2010Bennet BalberiaNo ratings yet

- Interport Resources Corp. v. SSIDocument3 pagesInterport Resources Corp. v. SSIBryce King100% (1)

- 095 Lee Vs CADocument2 pages095 Lee Vs CAjoyce100% (3)

- Tan v. Sycip - G.R. No. 153468 (Case Digest)Document2 pagesTan v. Sycip - G.R. No. 153468 (Case Digest)Jezen Esther Pati100% (1)

- China Bank Vs CA Case DigestDocument5 pagesChina Bank Vs CA Case DigestRob Closas100% (2)

- Lao v. LimDocument4 pagesLao v. LimJayson RacalNo ratings yet

- Western Institute of Technology v. SalasDocument1 pageWestern Institute of Technology v. SalasJudy RiveraNo ratings yet

- Hall Vs PiccioDocument1 pageHall Vs PiccioLindsay MillsNo ratings yet

- Reyes v. RCPI Employees Credit Union Inc.Document2 pagesReyes v. RCPI Employees Credit Union Inc.CeresjudicataNo ratings yet

- Raniel vs. JochicoDocument1 pageRaniel vs. JochicoJanlo Fevidal100% (1)

- ABS CBN Vs Hilario DigestDocument3 pagesABS CBN Vs Hilario DigestDyannah Alexa Marie Ramacho100% (1)

- GR No. 158805Document3 pagesGR No. 158805Karen Gina DupraNo ratings yet

- Valley Golf Vs Viuda de CaramDocument3 pagesValley Golf Vs Viuda de CaramaceamulongNo ratings yet

- Compromise Agreement - SupportDocument2 pagesCompromise Agreement - SupportDeb BieNo ratings yet

- Motion For Reduction of BailDocument2 pagesMotion For Reduction of BailDeb BieNo ratings yet

- Heirs of Gallardo Vs SolimanDocument11 pagesHeirs of Gallardo Vs SolimanDeb BieNo ratings yet

- Compilation of Political Law Cases 2010-2013Document54 pagesCompilation of Political Law Cases 2010-2013Deb BieNo ratings yet

- Betoy vs. NPC Board of DirectorsDocument2 pagesBetoy vs. NPC Board of DirectorsDeb BieNo ratings yet

- 6.crim Suggested Answers (1994-2006), WordDocument300 pages6.crim Suggested Answers (1994-2006), WordDeb Bie100% (1)

- Otero v. TanDocument2 pagesOtero v. TanDeb BieNo ratings yet

- Case Digests For Remedial Law 2014Document26 pagesCase Digests For Remedial Law 2014Austin Charles100% (1)

- CIR Vs San Roque Power DigestDocument27 pagesCIR Vs San Roque Power DigestDeb Bie50% (2)

- Heirs of Gallardo vs. Soliman - Case DigestDocument8 pagesHeirs of Gallardo vs. Soliman - Case DigestDeb BieNo ratings yet

- Globe Mckay Vs CADocument13 pagesGlobe Mckay Vs CADeb BieNo ratings yet

- Atong Paglaum Vs COMELEC (GR203766)Document55 pagesAtong Paglaum Vs COMELEC (GR203766)Deb BieNo ratings yet

- Bataclan v. Medina 102 Phil 181 DigestDocument4 pagesBataclan v. Medina 102 Phil 181 DigestDeb Bie100% (2)

- # 35 Republic v. CA and Molina Case Digest: Void MarriagesDocument10 pages# 35 Republic v. CA and Molina Case Digest: Void MarriagesDeb BieNo ratings yet

- 86 - Rodriguez Vs CADocument8 pages86 - Rodriguez Vs CADeb BieNo ratings yet

- Foreign Corporation - Top-Weld Manufacturing Vs EcedDocument13 pagesForeign Corporation - Top-Weld Manufacturing Vs EcedDeb BieNo ratings yet

- Fernando v. CA 208 Scra 714Document10 pagesFernando v. CA 208 Scra 714Deb BieNo ratings yet

- WarsawDocument26 pagesWarsawDeb BieNo ratings yet

- 01 Taylor v. Manila Electric Railroad 16 Phil 8Document15 pages01 Taylor v. Manila Electric Railroad 16 Phil 8Deb BieNo ratings yet

- Rule 128 - Ortanez Vs CADocument4 pagesRule 128 - Ortanez Vs CADeb BieNo ratings yet

- Anti Money Laundering Ra 9160Document16 pagesAnti Money Laundering Ra 9160Deb BieNo ratings yet

- CIR Vs American ExpressDocument35 pagesCIR Vs American ExpressDeb BieNo ratings yet

- Mendoza vs. SorianoDocument10 pagesMendoza vs. SorianoDeb BieNo ratings yet

- Snow Optimizer For SAP Software DatasheetDocument3 pagesSnow Optimizer For SAP Software DatasheetJarosław DukałaNo ratings yet

- Meeting The Challenges of Self-Represented Litigants: A Bench Book For General Sessions Judges of The State of TennesseeDocument12 pagesMeeting The Challenges of Self-Represented Litigants: A Bench Book For General Sessions Judges of The State of TennesseeTusharNo ratings yet

- Brault PerraultDocument6 pagesBrault Perraultgrtela100% (2)

- Lacson vs. LacsonDocument10 pagesLacson vs. LacsonPMVNo ratings yet

- Turkey Turkey 00 Clar RichDocument574 pagesTurkey Turkey 00 Clar RichAbdurrahman ŞahinNo ratings yet

- Filipino IndolenceDocument3 pagesFilipino IndolenceKevin Jairo Santiago100% (2)

- Dev Evidence of CitizenshipDocument84 pagesDev Evidence of CitizenshipElisabeth JohnsonNo ratings yet

- 05 Medina v. ValdellonDocument2 pages05 Medina v. Valdellonkmand_lustregNo ratings yet

- Thayer ASEAN 40th and 41st Summits in Cambodia - 1Document4 pagesThayer ASEAN 40th and 41st Summits in Cambodia - 1Carlyle Alan ThayerNo ratings yet

- Data Privacy Protection Rules StandardsDocument4 pagesData Privacy Protection Rules StandardsJMLOGICNo ratings yet

- Ge 3.contemporary World.m2t4Document6 pagesGe 3.contemporary World.m2t4Tian XianNo ratings yet

- Aud Su7Document39 pagesAud Su7Jane GavinoNo ratings yet

- Pay Slip For The Month of January-2024: Bandhan Bank LimitedDocument1 pagePay Slip For The Month of January-2024: Bandhan Bank Limitedumeshbamaniya005No ratings yet

- What Is A Bill of LadingDocument3 pagesWhat Is A Bill of LadingThao NguyenNo ratings yet

- 2 PhysiotherapistDocument32 pages2 Physiotherapistamit2352842No ratings yet

- Eset Smart KeysDocument2 pagesEset Smart KeysDoomwillNo ratings yet

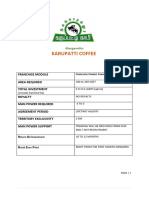

- Akc Franchise PDFDocument4 pagesAkc Franchise PDFVky SpeaksNo ratings yet

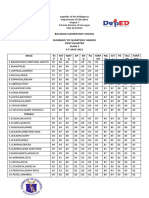

- 1ST Quarter Summary GradeDocument4 pages1ST Quarter Summary GradeTricia MorgaNo ratings yet

- SSBDocument3 pagesSSBEong Huat Corporation Sdn BhdNo ratings yet

- Differences Between Cash Dividends and Stock DividendsDocument4 pagesDifferences Between Cash Dividends and Stock DividendsUme Aiman Binte NasarNo ratings yet

- Template For Joint Venture AgreementDocument3 pagesTemplate For Joint Venture AgreementIan Pang50% (2)

- Group 2Document32 pagesGroup 2Ron louise PereyraNo ratings yet

- Charter Act 1813 - 14221776 - 2023 - 12 - 07 - 13 - 19Document3 pagesCharter Act 1813 - 14221776 - 2023 - 12 - 07 - 13 - 19deekshaa685No ratings yet

- Ao Fines Ra9296Document9 pagesAo Fines Ra9296Mark Wong delos ReyesNo ratings yet

- GE 2 Module 4 Lesson 1 4 With ReferencesDocument10 pagesGE 2 Module 4 Lesson 1 4 With ReferencesPark Min YeonNo ratings yet

- Almendralejo Chap8 DiscussionDocument16 pagesAlmendralejo Chap8 DiscussionRhywen Fronda GilleNo ratings yet

- English Book Review Synopsis - A Promised LandDocument3 pagesEnglish Book Review Synopsis - A Promised LandPriyanjali SinghNo ratings yet