You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

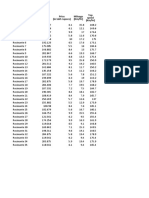

- Regression Analysis Random MotorsDocument11 pagesRegression Analysis Random MotorsNivedita Nautiyal100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2017 Hays Asia Salary Guide - enDocument116 pages2017 Hays Asia Salary Guide - ennurulhaiNo ratings yet

- Article 16 Magnetic Flux Leakage (MFL) ExaminationDocument5 pagesArticle 16 Magnetic Flux Leakage (MFL) ExaminationleonciomavarezNo ratings yet

- Pads Layout Mentor GraphicsDocument59 pagesPads Layout Mentor GraphicsgiorgioviNo ratings yet

- Stuffed The Sandwich Cookie Book Heather Mubarak Full Chapter PDF ScribdDocument67 pagesStuffed The Sandwich Cookie Book Heather Mubarak Full Chapter PDF Scribdleslie.dedeke821100% (5)

- Importance of Taxation KnowledgeDocument3 pagesImportance of Taxation KnowledgeElizabeth Wee Ern Cher33% (3)

- 4-3 Electrical Komponen SpecDocument9 pages4-3 Electrical Komponen Specibnu malkanNo ratings yet

- Digested Cases in Criminal ProcedureDocument7 pagesDigested Cases in Criminal ProcedureBartolome MercadoNo ratings yet

- Telit Run AT Remotely Application Note r4Document37 pagesTelit Run AT Remotely Application Note r4skhalopzNo ratings yet

- ParDocument19 pagesParpaco37No ratings yet

- Info Link University College Department of Accounting and FinanceDocument6 pagesInfo Link University College Department of Accounting and FinanceZeemanNo ratings yet

- Lands D PN 2 - 2020 App IDocument30 pagesLands D PN 2 - 2020 App IAlvisNo ratings yet

- HandiLaz Mini User Manual ReveDocument76 pagesHandiLaz Mini User Manual Revethao nguyenNo ratings yet

- SampoornSuraksha SchemeDetails14102022190Document1 pageSampoornSuraksha SchemeDetails14102022190Murthy NandulaNo ratings yet

- The Blue Lotus 11Document180 pagesThe Blue Lotus 11Yusuf MartinNo ratings yet

- Probability Interview QuestionsDocument31 pagesProbability Interview QuestionsBoul chandra GaraiNo ratings yet

- Arab Open University Tutor Marked Assignment (TMA)Document4 pagesArab Open University Tutor Marked Assignment (TMA)Elena AbdoNo ratings yet

- ITSM Configuration Quick StartDocument2 pagesITSM Configuration Quick StartliemdarenNo ratings yet

- (Rev-31May) BCAMP Closing Tentative ProgramDocument10 pages(Rev-31May) BCAMP Closing Tentative Programikakristiana widyaningrumNo ratings yet

- The Greatest Trading Book Ever PDFDocument12 pagesThe Greatest Trading Book Ever PDFTrần Quốc HùngNo ratings yet

- Technology For Teaching and Learning-2-UNIT-1Document30 pagesTechnology For Teaching and Learning-2-UNIT-1Jude Vincent MacalosNo ratings yet

- Enterprise Resource Planning & Material Requirement PlanningDocument5 pagesEnterprise Resource Planning & Material Requirement PlanningEnnavy YongkolNo ratings yet

- Microsoft Word 2007Document6 pagesMicrosoft Word 2007JoshLowensohn100% (32)

- Canon P900 ManualDocument242 pagesCanon P900 ManualAllen WilburNo ratings yet

- Study Successful CalculationDocument58 pagesStudy Successful CalculationRatnakar PatilNo ratings yet

- 10.4324 9780429466823-18 ChapterpdfDocument14 pages10.4324 9780429466823-18 Chapterpdffrankvalle5No ratings yet

- DP Sound Realtek wnt5 x86 32 906Document2 pagesDP Sound Realtek wnt5 x86 32 906Samwel KaranjaNo ratings yet

- Unit 1. BBE Assignment 2 of 2Document3 pagesUnit 1. BBE Assignment 2 of 2ldan240505No ratings yet

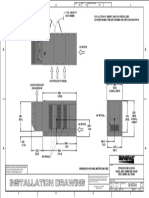

- Drawing Created From Pro/Engineer 3D File. Eco Modification To Be Applied To Solid Model OnlyDocument1 pageDrawing Created From Pro/Engineer 3D File. Eco Modification To Be Applied To Solid Model OnlyJuly E. Maldonado M.No ratings yet

- ANNEXURE 1-Eligibility Criteria - Empanelement of Collection AgenciesDocument5 pagesANNEXURE 1-Eligibility Criteria - Empanelement of Collection AgenciesKartik SikarwarNo ratings yet