You might also like

- Financial Services in IndiaDocument78 pagesFinancial Services in IndiaKrunal Vyas0% (1)

- Hedging With STIR FuturesDocument15 pagesHedging With STIR FuturesBach Nguyen Hoai AnhNo ratings yet

- Documentos Comerciales en InglesDocument46 pagesDocumentos Comerciales en InglesMiguel100% (3)

- Financial Instruments Noor 2Document14 pagesFinancial Instruments Noor 2NoorULAinNo ratings yet

- Fin Instrument and Derivative Group 5Document12 pagesFin Instrument and Derivative Group 5Clarisa MaharaniNo ratings yet

- FMI Unit 1Document34 pagesFMI Unit 1Raman KumarNo ratings yet

- Machining ToolsDocument11 pagesMachining ToolsRohan lallNo ratings yet

- IintroductionDocument9 pagesIintroductionSarjil alamNo ratings yet

- Unit 2 Financial System and Its ComponenetsDocument54 pagesUnit 2 Financial System and Its Componenetsaishwarya raikar100% (1)

- Chapter 4 - Review QuestionsDocument17 pagesChapter 4 - Review QuestionsNicole AgostoNo ratings yet

- AE18.1 Financial Markets and Financial SystemDocument23 pagesAE18.1 Financial Markets and Financial SystemTrishia Mae OliverosNo ratings yet

- CH 2Document13 pagesCH 2LIKENAWNo ratings yet

- Definitions TerminologiesDocument30 pagesDefinitions TerminologiesTajalli FatimaNo ratings yet

- International Banking & Foreign Exchange ManagementDocument4 pagesInternational Banking & Foreign Exchange ManagementAnupriya HiranwalNo ratings yet

- Debt Instrument Project PDFDocument50 pagesDebt Instrument Project PDFRohit VishwakarmaNo ratings yet

- Unit One.Document41 pagesUnit One.Manas JainNo ratings yet

- FE - Financial Assets and SecuritiesDocument7 pagesFE - Financial Assets and SecuritiesJUAN BERMUDEZNo ratings yet

- Money and Banking 22-23Document17 pagesMoney and Banking 22-23larissa nazarethNo ratings yet

- Index Executive Summary of Capital Markets Chapter 1 Investment BasicsDocument23 pagesIndex Executive Summary of Capital Markets Chapter 1 Investment Basicsswapnil_bNo ratings yet

- IntroductionDocument5 pagesIntroductionSagar100% (1)

- IFS - Chapter 1Document15 pagesIFS - Chapter 1riashahNo ratings yet

- Indian Financial SystemDocument16 pagesIndian Financial SystemSarada NagNo ratings yet

- Indian Financial SystemDocument5 pagesIndian Financial SystemKamal ShuklaNo ratings yet

- Unit Iii (International Business Environment)Document22 pagesUnit Iii (International Business Environment)RAMESH KUMARNo ratings yet

- Financial Instruments ProjectDocument7 pagesFinancial Instruments ProjectTom SalunkheNo ratings yet

- Glossary: Chapter 2-Money and CreditDocument15 pagesGlossary: Chapter 2-Money and CreditMubbasher HassanNo ratings yet

- Iv. Definitions/ Terminologies: I. AssetsDocument16 pagesIv. Definitions/ Terminologies: I. AssetsAhmad NazeerNo ratings yet

- Financial MarketDocument27 pagesFinancial Marketramesh.kNo ratings yet

- Tybbi Final ProjectDocument76 pagesTybbi Final ProjectKarim MerchantNo ratings yet

- Ifss Mod-1Document24 pagesIfss Mod-1ŚŰBHÁM řájNo ratings yet

- Ias 32 0 34Document22 pagesIas 32 0 34taspiatarannumNo ratings yet

- What Are The Various Types of Financial Markets?Document15 pagesWhat Are The Various Types of Financial Markets?Ronit SinghNo ratings yet

- An Overview of Indian Financial SystemDocument11 pagesAn Overview of Indian Financial SystemParul NigamNo ratings yet

- Indian Financial SystemDocument37 pagesIndian Financial SystemgeorgeNo ratings yet

- 8526 1uniDocument18 pages8526 1uniMs AimaNo ratings yet

- Financial System: by Debraj (308) Avtar (304) Ajay (301) Pavani (306) TejaDocument20 pagesFinancial System: by Debraj (308) Avtar (304) Ajay (301) Pavani (306) Tejasinghbenipal93No ratings yet

- Indian Financial SystemDocument5 pagesIndian Financial Systemshibashish PandaNo ratings yet

- Master of Business Administration 42Document7 pagesMaster of Business Administration 42ali_rahim1988No ratings yet

- Mission RBI 2018 - Financial SystemDocument6 pagesMission RBI 2018 - Financial SystemsaidheerendrapalkNo ratings yet

- Week 1 2Document10 pagesWeek 1 2Shanley Vanna EscalonaNo ratings yet

- Unit 3Document122 pagesUnit 3Prateek JainNo ratings yet

- Overview of Indian Financial MarketDocument22 pagesOverview of Indian Financial MarketPrinky SweetiepieNo ratings yet

- 1 Financial SystemDocument72 pages1 Financial Systemsaha apurvaNo ratings yet

- 3 The Indian Financial SystemDocument3 pages3 The Indian Financial SystemAbhishek AnandNo ratings yet

- Financial ServicesDocument32 pagesFinancial ServicesphilipkptrNo ratings yet

- Financial Markets and Institutions 1Document32 pagesFinancial Markets and Institutions 1Hamza Iqbal100% (1)

- FN302 01-FinAssets&Mkts RevisionDocument17 pagesFN302 01-FinAssets&Mkts RevisionAmani UrassaNo ratings yet

- Megha Malani Roll No.07 FybbiDocument18 pagesMegha Malani Roll No.07 Fybbiakotian91No ratings yet

- Money MarketDocument20 pagesMoney MarketThiên TrangNo ratings yet

- Financial Markets and InstitutionsDocument40 pagesFinancial Markets and InstitutionsAnZeerNo ratings yet

- Financial Markets & Services - Unit 1 NotesDocument60 pagesFinancial Markets & Services - Unit 1 Notesroshanrossi333No ratings yet

- Security (Finance) - WikipediaDocument10 pagesSecurity (Finance) - WikipediaŞtefan PtrtuNo ratings yet

- Attachment Indian Financial System IDocument43 pagesAttachment Indian Financial System IPratheesh BoseNo ratings yet

- Chapter2. Financial Inst&capital ArketsDocument12 pagesChapter2. Financial Inst&capital Arketsnewaybeyene5No ratings yet

- Unit 2 Financial Markets and Institutions: ObjectivesDocument13 pagesUnit 2 Financial Markets and Institutions: ObjectivesSHYAM GOELNo ratings yet

- Structure of Indian Financial SystemDocument6 pagesStructure of Indian Financial Systemanjaligupta23102003No ratings yet

- Final Hard Copy of Money and BankingDocument17 pagesFinal Hard Copy of Money and BankingMohammad Zahirul IslamNo ratings yet

- Why Study Financial Markets and InstitutionsDocument7 pagesWhy Study Financial Markets and InstitutionsMuhammad BilalNo ratings yet

- IF NotesDocument10 pagesIF NotesMd YusufNo ratings yet

- Given Below Are The Features of The Indian Financial SystemDocument3 pagesGiven Below Are The Features of The Indian Financial SystemALLIED AGENCIES0% (1)

- International Trade Finance: A NOVICE'S GUIDE TO GLOBAL COMMERCEFrom EverandInternational Trade Finance: A NOVICE'S GUIDE TO GLOBAL COMMERCENo ratings yet

- Bank Management Financial Service 21Document16 pagesBank Management Financial Service 21begardNo ratings yet

- 5a.capital Gains - Important NoteDocument3 pages5a.capital Gains - Important NoteKansal AbhishekNo ratings yet

- Ratio Formula RemarksDocument7 pagesRatio Formula RemarksmgajenNo ratings yet

- Acc Ch-7 Average Due Date SaDocument15 pagesAcc Ch-7 Average Due Date SaShivaSrinivas100% (3)

- Bài Kiểm Tra Giữa Kỳ 2Document2 pagesBài Kiểm Tra Giữa Kỳ 2Thu Trang NguyễnNo ratings yet

- G11 General-Mathematics Q2 L2Document7 pagesG11 General-Mathematics Q2 L2Maxine ReyesNo ratings yet

- IFMP Pakistan's Market Regulations Certification Mock Examination (100 QS) PDFDocument32 pagesIFMP Pakistan's Market Regulations Certification Mock Examination (100 QS) PDFJackey911100% (1)

- Importance of Merchant BankingDocument16 pagesImportance of Merchant BankingOmkar VedpathakNo ratings yet

- Loans and LeasesDocument19 pagesLoans and LeasesyanaNo ratings yet

- Ias 21 Summary Notes by Fahad IrfanDocument8 pagesIas 21 Summary Notes by Fahad Irfanmultiverseofkpop25No ratings yet

- PE IN IndiaDocument117 pagesPE IN IndiaRohit VijayvergiaNo ratings yet

- Boynton SM CH 17Document34 pagesBoynton SM CH 17jeankopler100% (1)

- Siyaram Health Care 2Document5 pagesSiyaram Health Care 2bm.india58No ratings yet

- FABM2 Q2 PPT 2 - Bank Accounts and Basic TransactionsDocument40 pagesFABM2 Q2 PPT 2 - Bank Accounts and Basic TransactionsSpencer Marvin P. EsguerraNo ratings yet

- Audit of Investments-ColorDocument6 pagesAudit of Investments-ColorChezka HerreraNo ratings yet

- Partnership LiquidationDocument2 pagesPartnership LiquidationJapsNo ratings yet

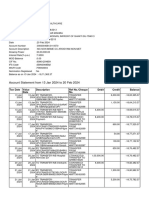

- Statement of Account: BranchDocument2 pagesStatement of Account: BranchKelum KonaraNo ratings yet

- Cash Flow Statement Analysis Between Commercial BaDocument9 pagesCash Flow Statement Analysis Between Commercial Baशिवम कर्णNo ratings yet

- Financial Accounting and Reporting - Cash and Cash Equivalents, Bank Reconciliation and Proof of CashDocument4 pagesFinancial Accounting and Reporting - Cash and Cash Equivalents, Bank Reconciliation and Proof of CashLuisitoNo ratings yet

- Ch06 JeterDocument26 pagesCh06 JeterLydia WulandariNo ratings yet

- A Study On Customer Insight Towards UPI (Unified Payment Interface) - An Advancement of Mobile Payment SystemDocument8 pagesA Study On Customer Insight Towards UPI (Unified Payment Interface) - An Advancement of Mobile Payment SystemAnkita RanaNo ratings yet

- AP 01 - Cash To Accrual BasisDocument11 pagesAP 01 - Cash To Accrual BasisGabriel OrolfoNo ratings yet

- Introduction To Bimetallic Standard of MoneyDocument6 pagesIntroduction To Bimetallic Standard of MoneyPrithy GrNo ratings yet

- Img 20230625 0002Document1 pageImg 20230625 0002van souNo ratings yet

- Online ChallanDocument1 pageOnline ChallanKalpesh DeoraNo ratings yet

- Audit Problems CashDocument18 pagesAudit Problems CashYenelyn Apistar Cambarijan0% (1)

- Auditing and Assurance Services 7th Edition Louwers Solutions Manual DownloadDocument29 pagesAuditing and Assurance Services 7th Edition Louwers Solutions Manual DownloadEthel Tanenbaum100% (25)

- Midterm ReviewDocument4 pagesMidterm ReviewMuhammad AalimNo ratings yet