You might also like

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsFrom EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsNo ratings yet

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Aghara Knitwear Pvt. LTD.: Summary of Rated InstrumentsDocument6 pagesAghara Knitwear Pvt. LTD.: Summary of Rated Instrumentssatvik ahujaNo ratings yet

- Ayushman Merchants Private Limited: Summary of Rated InstrumentsDocument6 pagesAyushman Merchants Private Limited: Summary of Rated InstrumentsJeffNo ratings yet

- Ankit Pulps and Boards - R-25102018Document6 pagesAnkit Pulps and Boards - R-25102018HEMANT GURJARNo ratings yet

- Magnolia Martinique - R - 03082017Document7 pagesMagnolia Martinique - R - 03082017Bhavin SagarNo ratings yet

- Gujarat Guardian Limited-R-30032018Document6 pagesGujarat Guardian Limited-R-30032018SuhasNo ratings yet

- Iscon Balaji Foods - R-24052017Document7 pagesIscon Balaji Foods - R-24052017Kunal DamaniNo ratings yet

- AOV Exports Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument7 pagesAOV Exports Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDevansh ThaparNo ratings yet

- Vikas Spool Private Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesVikas Spool Private Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating Actionvinay durgapalNo ratings yet

- Laser Fibers Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument6 pagesLaser Fibers Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionBhavin SagarNo ratings yet

- Jainam Cables (India) Private Limited: Summary of Rated InstrumentsDocument6 pagesJainam Cables (India) Private Limited: Summary of Rated InstrumentspunamNo ratings yet

- Anand Jewels (Indore) - R-30072019Document6 pagesAnand Jewels (Indore) - R-30072019Rishabh KhandelwalNo ratings yet

- LGB Forge Limited: Summary of Rating ActionDocument7 pagesLGB Forge Limited: Summary of Rating ActionPuneet367No ratings yet

- R.S. Brothers Retail - R-06122017Document7 pagesR.S. Brothers Retail - R-06122017srv 99No ratings yet

- Press Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionDocument4 pagesPress Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionData CentrumNo ratings yet

- BFG International Private Limited: Summary of Rated InstrumentsDocument6 pagesBFG International Private Limited: Summary of Rated InstrumentsB Vignesh BabuNo ratings yet

- ABT Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesABT Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionWilliam Veloz DiazNo ratings yet

- D&H Secheron Electrodes Private Limited: Summary of Rated InstrumentsDocument6 pagesD&H Secheron Electrodes Private Limited: Summary of Rated InstrumentsMahee MahemaaNo ratings yet

- Ganga Rasayanie Private Limited-R-10102019Document7 pagesGanga Rasayanie Private Limited-R-10102019DarshanNo ratings yet

- Press Release MaharajaDocument5 pagesPress Release MaharajaMS SAMIRANNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Solairedirect Energy India Private LimitedDocument6 pagesSolairedirect Energy India Private LimitedAfzal AneesNo ratings yet

- Mechemco - R-30102017 PDFDocument7 pagesMechemco - R-30102017 PDFflytorahulNo ratings yet

- Riyan Paper Mill: Summary of Rated InstrumentsDocument6 pagesRiyan Paper Mill: Summary of Rated InstrumentsKNOW INDIANo ratings yet

- Satya Deeptha Pharmaceuticals LimitedDocument6 pagesSatya Deeptha Pharmaceuticals LimitedsriramraneNo ratings yet

- Sara International Private Limited Rating UpgradedDocument6 pagesSara International Private Limited Rating UpgradedRavi BabuNo ratings yet

- Airvision India Private Limited - R - 25082020Document7 pagesAirvision India Private Limited - R - 25082020DarshanNo ratings yet

- Shree Radhekrushna Ginning - R-11092017Document6 pagesShree Radhekrushna Ginning - R-11092017SuMit PaTilNo ratings yet

- Alkali Metals Limited - R - 26112020Document7 pagesAlkali Metals Limited - R - 26112020Yogi173No ratings yet

- Stove Kraft Limited-3Document5 pagesStove Kraft Limited-3venkyniyerNo ratings yet

- Vaighai Agro Products Limited: Instruments Amount Rated (Rs. Crore) Rating ActionDocument7 pagesVaighai Agro Products Limited: Instruments Amount Rated (Rs. Crore) Rating ActionSuresh NmsNo ratings yet

- Azure Power Thirty Six - R-15102018Document6 pagesAzure Power Thirty Six - R-15102018vinay durgapalNo ratings yet

- Bata India Limited: Summary of Rating ActionDocument6 pagesBata India Limited: Summary of Rating ActionDhrubajyoti DattaNo ratings yet

- The DataDocument7 pagesThe DatashettyNo ratings yet

- Ultramarine & Pigments LTD: Summary of Rated InstrumentsDocument7 pagesUltramarine & Pigments LTD: Summary of Rated Instrumentsjanmejay26No ratings yet

- Della Adventure R 17112017Document7 pagesDella Adventure R 17112017Anil KanojiaNo ratings yet

- Press Release 3B Fibreglass Norway AS: Policy On Withdrawal of Ratings Policy On Default RecognitionDocument3 pagesPress Release 3B Fibreglass Norway AS: Policy On Withdrawal of Ratings Policy On Default RecognitionData CentrumNo ratings yet

- Super Screws Private Limited: Summary of Rated InstrumentsDocument7 pagesSuper Screws Private Limited: Summary of Rated InstrumentsAnonymous bdUhUNm7JNo ratings yet

- Indotech Transformers LimitedDocument6 pagesIndotech Transformers LimitedMonika GNo ratings yet

- Acknit Industries Limited: Summary of Rating ActionDocument7 pagesAcknit Industries Limited: Summary of Rating ActionprasanthNo ratings yet

- Prime Urban ICRA April 17Document7 pagesPrime Urban ICRA April 17BALMERNo ratings yet

- ALM Industries Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating ActionDocument6 pagesALM Industries Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating Actionsgr_kansagraNo ratings yet

- Avantor Performance Materials - R - 25052018Document5 pagesAvantor Performance Materials - R - 25052018Ankit JainNo ratings yet

- Triveni TurbineDocument6 pagesTriveni TurbinevikasNo ratings yet

- RL Steel Jan 2017 ICRADocument6 pagesRL Steel Jan 2017 ICRAPuneet367No ratings yet

- Press Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Document5 pagesPress Release Amkette Analytics Limited: Details of Instruments/facilities in Annexure-1Data CentrumNo ratings yet

- Sree Akkamamba Textiles - R - 13032020Document7 pagesSree Akkamamba Textiles - R - 13032020saikiran reddyNo ratings yet

- 3B Binani GlassfibreDocument2 pages3B Binani GlassfibreData CentrumNo ratings yet

- Pan Healthcare Private Limited (PHCPL) October 12, 2020Document5 pagesPan Healthcare Private Limited (PHCPL) October 12, 2020Sachin DhorajiyaNo ratings yet

- Eurotex Industries and Exports Limited: Summary of Rated InstrumentsDocument7 pagesEurotex Industries and Exports Limited: Summary of Rated InstrumentsHari KrishnanNo ratings yet

- Investigation On The Flow Behaviour of ADocument6 pagesInvestigation On The Flow Behaviour of ANikhil GuptaNo ratings yet

- Ace Designers-R-05042018 PDFDocument7 pagesAce Designers-R-05042018 PDFkachadaNo ratings yet

- Wipro Limited - Update On Material Event: Summary of Rating(s) OutstandingDocument7 pagesWipro Limited - Update On Material Event: Summary of Rating(s) OutstandingMegha PrakashNo ratings yet

- Saya Homes ProjectDocument5 pagesSaya Homes ProjectSatish RAjNo ratings yet

- Singer India Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesSinger India Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionSaravanan BalakrishnanNo ratings yet

- Ganesh Benzoplast LTD (GBL)Document7 pagesGanesh Benzoplast LTD (GBL)Positive ThinkerNo ratings yet

- Titan Company Limited: Migration of The Rating Outstanding On The Medium-Term Rating Scale To The Long-Term Rating ScaleDocument5 pagesTitan Company Limited: Migration of The Rating Outstanding On The Medium-Term Rating Scale To The Long-Term Rating ScaleMalavShahNo ratings yet

- Sitaram Maharaj Sakhar - R - 22042019 PDFDocument6 pagesSitaram Maharaj Sakhar - R - 22042019 PDFJagadamba RealtorNo ratings yet

- The Government Tele Communication R 03102017Document7 pagesThe Government Tele Communication R 03102017SandeeploguNo ratings yet

- Enigma IndiabuilsDocument36 pagesEnigma IndiabuilsKaran Mehta50% (2)

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- Companiees DataDocument51 pagesCompaniees Datasales100% (1)

- CPhI China'09Document1 pageCPhI China'09Bhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- Underwriters AgreementDocument15 pagesUnderwriters AgreementBhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

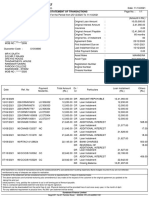

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Toaz - Info Data 1xlsx PRDocument1,033 pagesToaz - Info Data 1xlsx PRBhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Amalgamation - Share India Securities - Turnaround Corporate AdvisorsDocument5 pagesAmalgamation - Share India Securities - Turnaround Corporate AdvisorsBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- piVentures-Term Sheet - TemplateDocument6 pagespiVentures-Term Sheet - TemplateBhavin SagarNo ratings yet

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDocument10 pagesAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- Removed HEM SECURITIES - MAGAZINE - DEC (8) - 5Document1 pageRemoved HEM SECURITIES - MAGAZINE - DEC (8) - 5Bhavin SagarNo ratings yet

- Demerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiDocument4 pagesDemerger May 2021 - Tips Industries LTD by Inga Advisors MumbaiBhavin SagarNo ratings yet

- Overall Strategies For All VerticalsDocument2 pagesOverall Strategies For All VerticalsBhavin SagarNo ratings yet

- Revised SME IPO Data Performers 2021Document13 pagesRevised SME IPO Data Performers 2021Bhavin SagarNo ratings yet

- Performance of Sectoral Indices - 2021Document80 pagesPerformance of Sectoral Indices - 2021Bhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- NDADocument7 pagesNDABhavin SagarNo ratings yet

- piVentures-Term Sheet - TemplateDocument6 pagespiVentures-Term Sheet - TemplateBhavin SagarNo ratings yet

- 7868 01 Spaceship Roadmap Concept For Powerpoint 16x9Document5 pages7868 01 Spaceship Roadmap Concept For Powerpoint 16x9Bhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- Rimi Khanuja Vs S P Mehra Ors On 24 August 2022Document4 pagesRimi Khanuja Vs S P Mehra Ors On 24 August 2022Prakhar SinghNo ratings yet

- Extreme TourismDocument2 pagesExtreme TourismRodrigo RezendeNo ratings yet

- Communion With The Goddess Priestesses PDFDocument30 pagesCommunion With The Goddess Priestesses PDFAtmageet KaurNo ratings yet

- CS PDFDocument26 pagesCS PDFcwmediaNo ratings yet

- KBC Terms and ConditionsDocument30 pagesKBC Terms and ConditionspkfmsNo ratings yet

- ISO 9001 Quality Objectives - What They Are and How To Write ThemDocument7 pagesISO 9001 Quality Objectives - What They Are and How To Write ThemankitNo ratings yet

- Review Nikolaus Pevsner Pioneers of Modern Design: From William Morris To Walter GropiusDocument8 pagesReview Nikolaus Pevsner Pioneers of Modern Design: From William Morris To Walter GropiusTomas Aassved HjortNo ratings yet

- All Grown Up - BareDocument9 pagesAll Grown Up - BareNiamh HawkesNo ratings yet

- Peoria County Booking Sheet 11/02/13Document8 pagesPeoria County Booking Sheet 11/02/13Journal Star police documentsNo ratings yet

- Getting To Grips With A320 &Document88 pagesGetting To Grips With A320 &duythienddt100% (4)

- Summary Report Family Code of The Pihilippines E.O. 209Document41 pagesSummary Report Family Code of The Pihilippines E.O. 209Cejay Deleon100% (3)

- Family DiversityDocument4 pagesFamily DiversityAlberto Salazar CarballoNo ratings yet

- 4.4.1.2 Packet Tracer - Configure IP ACLs To Mitigate Attacks - InstructorDocument7 pages4.4.1.2 Packet Tracer - Configure IP ACLs To Mitigate Attacks - Instructorrafael8214No ratings yet

- September 2017 Real Estate Appraiser Licensure ExamDocument12 pagesSeptember 2017 Real Estate Appraiser Licensure ExamRapplerNo ratings yet

- Punjab National Bank Punjab National Bank Punjab National BankDocument1 pagePunjab National Bank Punjab National Bank Punjab National BankHarsh ChaudharyNo ratings yet

- HRMT 623 Hamid Kazemi AssignmentDocument14 pagesHRMT 623 Hamid Kazemi AssignmentAvneet Kaur SranNo ratings yet

- Resume-Roberta Strange 2014Document3 pagesResume-Roberta Strange 2014Jamie RobertsNo ratings yet

- Assignment 3: Research Reflection PaperDocument9 pagesAssignment 3: Research Reflection PaperDang HuynhNo ratings yet

- United States v. Arthur Young & Co., 465 U.S. 805 (1984)Document15 pagesUnited States v. Arthur Young & Co., 465 U.S. 805 (1984)Scribd Government DocsNo ratings yet

- Comparison Among Languages: C. Cappa, J. Fernando, S. GiuliviDocument62 pagesComparison Among Languages: C. Cappa, J. Fernando, S. GiuliviSaoodNo ratings yet

- Unjust identification of Pushyamitra as a BrahminDocument6 pagesUnjust identification of Pushyamitra as a BrahminSHIVAM SINGHNo ratings yet

- Letter of Motivation (Financial Services Management)Document1 pageLetter of Motivation (Financial Services Management)Tanzeel Ur Rahman100% (5)

- Aerographer's Mate Second Class, Volume 2Document444 pagesAerographer's Mate Second Class, Volume 2Bob Kowalski100% (2)

- A Study On Equity Analysis of Selected Banking StocksDocument109 pagesA Study On Equity Analysis of Selected Banking Stocksanil0% (1)

- Pipeline Emergencies - 3e - WcoverDocument246 pagesPipeline Emergencies - 3e - WcoverSergio Eligio Sánchez CruzNo ratings yet

- Ffiitrsfrshq (Fthfraf) : LadingDocument1 pageFfiitrsfrshq (Fthfraf) : LadingNeo KnightNo ratings yet

- CHAPTER 2 AnalysisDocument7 pagesCHAPTER 2 AnalysisJv Seberias100% (1)

- Group 8 Zara Fast Fashion in Digital AgeDocument14 pagesGroup 8 Zara Fast Fashion in Digital AgeAshish DrawkcabNo ratings yet

- I Twin Technology11 PDFDocument14 pagesI Twin Technology11 PDFChandhanNo ratings yet

- Materials System SpecificationDocument6 pagesMaterials System SpecificationFAPM1285No ratings yet