You might also like

- Auditing McqsDocument9 pagesAuditing McqsAbid Tareen0% (1)

- Advanced Auditing & AssuranceDocument9 pagesAdvanced Auditing & AssuranceHaider BhaiNo ratings yet

- Auditing of Banking SectorDocument4 pagesAuditing of Banking SectorhareshNo ratings yet

- T.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Document13 pagesT.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Kadam KartikeshNo ratings yet

- Auditing MCQ'S AnswersDocument6 pagesAuditing MCQ'S AnswersDevraj JaiswalNo ratings yet

- Auditing MCQ 100Document34 pagesAuditing MCQ 100Muhammad Hamid50% (2)

- Exit Model (Fundamental of Accounting)Document6 pagesExit Model (Fundamental of Accounting)aronNo ratings yet

- In The Calculation of Return On Shareholders Investments The Referred Investment Deals WithDocument20 pagesIn The Calculation of Return On Shareholders Investments The Referred Investment Deals WithAnilKumarNo ratings yet

- Auditing Sem VI MCQsDocument10 pagesAuditing Sem VI MCQsMayur PadaveNo ratings yet

- Tax Planning and Management TaxDocument5 pagesTax Planning and Management TaxHarsha HarshaNo ratings yet

- Multiple Choice QuestionsDocument9 pagesMultiple Choice QuestionsReymark MutiaNo ratings yet

- Chapter 5 Computer Fraud: Accounting Information Systems, 13e (Romney/Steinbart)Document15 pagesChapter 5 Computer Fraud: Accounting Information Systems, 13e (Romney/Steinbart)RyzeNo ratings yet

- Auditing Exam 1 MultipleDocument65 pagesAuditing Exam 1 MultipleChristian Dalos100% (1)

- DocDocument13 pagesDocMequen Chille QuemadoNo ratings yet

- Auditing and AssuranceDocument52 pagesAuditing and AssuranceNagarjuna ReddyNo ratings yet

- International AccountingDocument13 pagesInternational Accountingashish300950% (2)

- MCQ On TDS, TCS & Advance TaxDocument15 pagesMCQ On TDS, TCS & Advance TaxPrakhar GuptaNo ratings yet

- Ais MCQSDocument7 pagesAis MCQSAbdul wahabNo ratings yet

- Public Finance NotesDocument12 pagesPublic Finance NotesshivaniNo ratings yet

- Acc 101 QuestionsDocument6 pagesAcc 101 QuestionsSamuel100% (1)

- AuditingDocument626 pagesAuditingAbdulrehman567No ratings yet

- Principles of AuditingDocument148 pagesPrinciples of AuditingAsteway MesfinNo ratings yet

- Auditing Lesson Plan Part Two 2 12 2020 CorrigéDocument6 pagesAuditing Lesson Plan Part Two 2 12 2020 CorrigéBen Abdallah RihabNo ratings yet

- Financial Management Mcqs With AnswersDocument53 pagesFinancial Management Mcqs With Answersviveksharma51No ratings yet

- Audit UNIT 6Document7 pagesAudit UNIT 6Nigussie BerhanuNo ratings yet

- CH 1Document34 pagesCH 1Ram KumarNo ratings yet

- MCQ Test AbdDocument3 pagesMCQ Test AbdRahul Ghosale100% (1)

- Audit II Mid ExamDocument4 pagesAudit II Mid ExamTesfaye SimeNo ratings yet

- Auditing I (Acct 411) : Unit 1: Overview of AuditingDocument30 pagesAuditing I (Acct 411) : Unit 1: Overview of Auditingsamuel debebeNo ratings yet

- Infolink Uiversity College Dilla Campus Department of Accountig & FinanceDocument4 pagesInfolink Uiversity College Dilla Campus Department of Accountig & FinanceKanbiro OrkaidoNo ratings yet

- Taxatio MCQDocument10 pagesTaxatio MCQAtif KhanNo ratings yet

- Basic Terms True FalseDocument12 pagesBasic Terms True FalseSarvar PathanNo ratings yet

- Amalgamation, Absorption, Reconstruction, and General Insurance Company MCQDocument17 pagesAmalgamation, Absorption, Reconstruction, and General Insurance Company MCQbharat wankhedeNo ratings yet

- Accountancy Vol 1 - EM PDFDocument136 pagesAccountancy Vol 1 - EM PDFvickkyNo ratings yet

- Curriclum Revised 1st DraftDocument73 pagesCurriclum Revised 1st Draftamaruthivaraprasad100% (1)

- Model Question Paper - IGST Act.: (2 Marks Each) Multiple Choice QuestionsDocument25 pagesModel Question Paper - IGST Act.: (2 Marks Each) Multiple Choice QuestionsShyam Prasad100% (1)

- 2.1. What Is Auditing Standard?: General Standards Standards of Fieldwork Standards of ReportingDocument56 pages2.1. What Is Auditing Standard?: General Standards Standards of Fieldwork Standards of ReportingFackallofyouNo ratings yet

- Principles of Auditing MCQDocument24 pagesPrinciples of Auditing MCQaao wacNo ratings yet

- Auditing CH 1Document20 pagesAuditing CH 1Nigussie BerhanuNo ratings yet

- MCQ Public FinanceDocument4 pagesMCQ Public FinanceWild Gaming YT100% (2)

- International Economics II Chapter 2Document29 pagesInternational Economics II Chapter 2Härêm ÔdNo ratings yet

- REDEMPTION OF SHARES & DEBENTURES MCQsDocument7 pagesREDEMPTION OF SHARES & DEBENTURES MCQsChetan StoresNo ratings yet

- Unit 1-4Document104 pagesUnit 1-4ዝምታ ተሻለNo ratings yet

- Auditing Lecture Slides Introduction.Document30 pagesAuditing Lecture Slides Introduction.MoniqueNo ratings yet

- Audit B.com Part 2Document1 pageAudit B.com Part 2Ahmad Nawaz JanjuaNo ratings yet

- Wroksheet Princples of Auditing IIDocument9 pagesWroksheet Princples of Auditing IIEwnetu TadesseNo ratings yet

- Public Finance: D. Interest Rates C. Firms' Investment DecisionsDocument5 pagesPublic Finance: D. Interest Rates C. Firms' Investment DecisionsPhaul QuicktrackNo ratings yet

- Chapter 5 MC QuestionsDocument5 pagesChapter 5 MC QuestionsjessicaNo ratings yet

- BSA202 GR03 CH03 Ethics Fraud and Internal Control QuizDocument4 pagesBSA202 GR03 CH03 Ethics Fraud and Internal Control Quizohmyme sungjaeNo ratings yet

- 80 Auditing Assurance MCQ'S: © Ca WorldDocument14 pages80 Auditing Assurance MCQ'S: © Ca WorldZain Butt50% (2)

- 4 Multiple Choice QuestionsDocument2 pages4 Multiple Choice QuestionsMohib Ullah YousafzaiNo ratings yet

- MCQ On Management Information System AnsDocument34 pagesMCQ On Management Information System AnsEnrique Sonsona Oliveros jrNo ratings yet

- Multiple-Choice QuestionsDocument15 pagesMultiple-Choice QuestionsDiossaNo ratings yet

- Cost Accounting Question BankDocument48 pagesCost Accounting Question BankShedrine WamukekheNo ratings yet

- Auditing and Taxation: Ty Bcom - Auditing and Taxation - MCQ - Question Bank - Compiled by Manoj VoraDocument7 pagesAuditing and Taxation: Ty Bcom - Auditing and Taxation - MCQ - Question Bank - Compiled by Manoj VoraSample Use67% (3)

- Chapter 1: Accounting For Incomplete Records or Single Entry Exercise # 1Document12 pagesChapter 1: Accounting For Incomplete Records or Single Entry Exercise # 1amirNo ratings yet

- Audit MCQDocument20 pagesAudit MCQNitin BadganchiNo ratings yet

- MCQ'S Auditing Sem 4Document31 pagesMCQ'S Auditing Sem 4Siddharth VoraNo ratings yet

- B Com Semester 6 Auditing and Assurance Multiple Choice QuestionsDocument113 pagesB Com Semester 6 Auditing and Assurance Multiple Choice QuestionsBhavesh DhandeNo ratings yet

- Auditing Assurance MCQ B Com SDocument26 pagesAuditing Assurance MCQ B Com SBhavan YadavNo ratings yet

- Journal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggioDocument6 pagesJournal of Destination Marketing & Management: Giacomo Del Chiappa, Rodolfo BaggiovineethkmenonNo ratings yet

- Project PPT (ASHA V S)Document18 pagesProject PPT (ASHA V S)vineethkmenonNo ratings yet

- How To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: ADocument12 pagesHow To Cite: Marikyan, D. & Papagiannidis, S. (2022) Technology Acceptance Model: AvineethkmenonNo ratings yet

- Emotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsuranceDocument13 pagesEmotional Finance: Financial Anxiety Among Salaried Individuals With Special Reference To Life InsurancevineethkmenonNo ratings yet

- PG Project PPT (Revathykrishna PS)Document24 pagesPG Project PPT (Revathykrishna PS)vineethkmenonNo ratings yet

- Performance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18Document4 pagesPerformance Evaluation of Systematic Investment Plans in Top Rated Conservative Hybrid Mutual Funds During 2016-18vineethkmenonNo ratings yet

- Camel AnalysisDocument12 pagesCamel AnalysisvineethkmenonNo ratings yet

- Teaching Aptitude For UGCDocument13 pagesTeaching Aptitude For UGCvineethkmenonNo ratings yet

- Bcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsDocument14 pagesBcom - Semester V Cm05Baa02 - Special Accounting Multiple Choice QuestionsvineethkmenonNo ratings yet

- Chapter 14 Foundations of Behavior: True/False QuestionsDocument35 pagesChapter 14 Foundations of Behavior: True/False QuestionsvineethkmenonNo ratings yet

- Sruthy Vineeth STC Full PaperDocument5 pagesSruthy Vineeth STC Full PapervineethkmenonNo ratings yet

- KMRL ProjectDocument48 pagesKMRL Projectvineethkmenon80% (10)

- Kwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwDocument2 pagesKwÿm/ Ktωf/W: D∂X Hnzym-'Ymk A≤Ym-) I KwlwvineethkmenonNo ratings yet

- MCQ GST Answer KeyDocument23 pagesMCQ GST Answer KeyvineethkmenonNo ratings yet

- Famous Festivals in Kerala PDFDocument19 pagesFamous Festivals in Kerala PDFvineethkmenonNo ratings yet

- Accounting For Managerial DecisionsDocument22 pagesAccounting For Managerial DecisionsvineethkmenonNo ratings yet

- KFC FORM 7 Report of Transfer of Charge PDFDocument2 pagesKFC FORM 7 Report of Transfer of Charge PDFvineethkmenon100% (1)

- Core 13 Applied Ethics (4) 20 - 02Document3 pagesCore 13 Applied Ethics (4) 20 - 02vineethkmenonNo ratings yet

- Kerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.Document215 pagesKerala Service Rules Full - Uploaded by T James Joseph Adhikarathil, Deputy Collector Alappuzha.James AdhikaramNo ratings yet

- UG Model QP MergedDocument93 pagesUG Model QP MergedvineethkmenonNo ratings yet

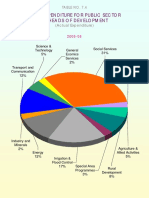

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

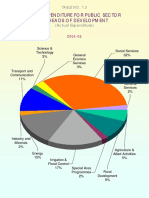

- Five Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentDocument1 pageFive Yaer Plan: Plan Expenditure For Public Sector by Heads of DevelopmentvineethkmenonNo ratings yet

- Nbaa PloDocument212 pagesNbaa PlosmlingwaNo ratings yet

- AP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Document10 pagesAP-200Q (Quizzer - Error Correction, Accounting Changes, Cash-Accrual & Single Entry)Bernadette Panican100% (1)

- SUMMATIVE Assessment II March 2010 Design of The Question PaperDocument10 pagesSUMMATIVE Assessment II March 2010 Design of The Question PaperSanthosh KammamNo ratings yet

- Tally QuestionDocument9 pagesTally QuestionmekavinashNo ratings yet

- Advertising Budget - Objectives, Approaches, Methods - BBA - Mantra PDFDocument14 pagesAdvertising Budget - Objectives, Approaches, Methods - BBA - Mantra PDFAbhimanyuNo ratings yet

- DTR TransmittalDocument12 pagesDTR TransmittalANGIE BERNALNo ratings yet

- Recent Fabm ShortDocument20 pagesRecent Fabm Shortgk concepcionNo ratings yet

- D Business Combinations - IFRS 3 (Revised)Document10 pagesD Business Combinations - IFRS 3 (Revised)Brook KongNo ratings yet

- Financial Reporting and AnalysisDocument5 pagesFinancial Reporting and AnalysisPiyush AgarwalNo ratings yet

- Admas University Bishoftu Campus: Course Title - Maintain Inventory RecordsDocument6 pagesAdmas University Bishoftu Campus: Course Title - Maintain Inventory RecordsTilahun GirmaNo ratings yet

- Solution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesDocument10 pagesSolution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesGeorge BulikiNo ratings yet

- Book 6Document4 pagesBook 6Actg SolmanNo ratings yet

- Financial Accounting Assignment 2Document6 pagesFinancial Accounting Assignment 2kirubelNo ratings yet

- Introduction To Financial Accounting NotesDocument3 pagesIntroduction To Financial Accounting NotesRaksa HemNo ratings yet

- Ebook College Accounting Chapters 1 30 13Th Edition Price Solutions Manual Full Chapter PDFDocument67 pagesEbook College Accounting Chapters 1 30 13Th Edition Price Solutions Manual Full Chapter PDFconvive.unsadden.hgp2100% (12)

- VP Religious AffairDocument4 pagesVP Religious Affairjaiscey valenciaNo ratings yet

- Sarangapani & Co: Chartered AccountantsDocument14 pagesSarangapani & Co: Chartered AccountantsSarangapani KaliyamoorthyNo ratings yet

- Aud339 Audit ReportDocument22 pagesAud339 Audit ReportNur IzzahNo ratings yet

- Fixed Assets PDFDocument21 pagesFixed Assets PDFSrihari GullaNo ratings yet

- PG 2022 Batch Onwards November 2023Document35 pagesPG 2022 Batch Onwards November 2023Abarna TNo ratings yet

- CH 03Document71 pagesCH 03martinus linggo100% (1)

- User Manual Asset AccountingDocument47 pagesUser Manual Asset AccountinginasapNo ratings yet

- FA RSL CaseDocument10 pagesFA RSL Caseharendra choudharyNo ratings yet

- 2108AFE Topic 4 - Accounting Information Systems - StudentDocument38 pages2108AFE Topic 4 - Accounting Information Systems - StudentAnh TrầnNo ratings yet

- EA and ReportingDocument17 pagesEA and ReportingsengottuvelNo ratings yet

- 1) Journal Entries: 496199857.xls How To Use This FileDocument6 pages1) Journal Entries: 496199857.xls How To Use This FileAdo BerikelashviliNo ratings yet

- SoM UIA Forensic Review 11.25.2020 708891 7Document34 pagesSoM UIA Forensic Review 11.25.2020 708891 7Tiffany RobertsonNo ratings yet

- Financial Accounting Fundamentals 6Th Edition Wild Test Bank Full Chapter PDFDocument67 pagesFinancial Accounting Fundamentals 6Th Edition Wild Test Bank Full Chapter PDFBriannaWashingtonpoyb100% (11)

- Chapter 1-Introduction To Financial Reporting: Multiple ChoiceDocument17 pagesChapter 1-Introduction To Financial Reporting: Multiple Choicekurinkato83100% (1)

- Internal Control Questionnaire YES NO NA Comments Component: Control Environment Integrity and Ethical ValuesDocument44 pagesInternal Control Questionnaire YES NO NA Comments Component: Control Environment Integrity and Ethical ValuesMyra BarandaNo ratings yet