You might also like

- Theory of the Firm Production Functions and Cost MinimizationDocument4 pagesTheory of the Firm Production Functions and Cost MinimizationFernanda BeltranNo ratings yet

- Hurun India Rich ListDocument21 pagesHurun India Rich ListAnirban Dasgupta100% (2)

- Company Database AnnexureDocument3 pagesCompany Database AnnexureNikhil BadodekarNo ratings yet

- Report-Malls in IndiaDocument55 pagesReport-Malls in Indiahavingosar28No ratings yet

- Disruptions in Real Estate in IndiaDocument56 pagesDisruptions in Real Estate in IndiaDevasish Parmar100% (1)

- Ecommerce Handbook: Growth Outlook and Competitive LandscapeDocument43 pagesEcommerce Handbook: Growth Outlook and Competitive LandscapeTiago SoaresNo ratings yet

- TATA Group SlidesDocument64 pagesTATA Group Slideszahid arif0% (1)

- p2 - Guerrero Ch10Document28 pagesp2 - Guerrero Ch10JerichoPedragosa67% (3)

- Case EasyjetDocument12 pagesCase EasyjetpratyushaNo ratings yet

- Shivam Real EstateDocument46 pagesShivam Real EstateTasmay EnterprisesNo ratings yet

- CBRE - India Office Market View Q12012Document12 pagesCBRE - India Office Market View Q12012inkpot3gNo ratings yet

- Bangalore Office 1Q 2012 Cushman & WakefieldDocument2 pagesBangalore Office 1Q 2012 Cushman & WakefieldReuben JacobNo ratings yet

- Knight Frank Buying Commercial Property in India 2663Document6 pagesKnight Frank Buying Commercial Property in India 2663Aravind SankaranNo ratings yet

- India Office Market Report Q3 - 2020Document6 pagesIndia Office Market Report Q3 - 2020jatin girotraNo ratings yet

- India Office MarketView Q1 2019 PuneDocument7 pagesIndia Office MarketView Q1 2019 PuneAbhilash BhatNo ratings yet

- Commercial Office Development Trends in MumbaiDocument14 pagesCommercial Office Development Trends in MumbaiShubham BhuteNo ratings yet

- Bangaluru Commercial: Real Estate Analysis ofDocument16 pagesBangaluru Commercial: Real Estate Analysis ofmanojkumarmishratNo ratings yet

- Gurgaon Draft Dev Plan 2031Document21 pagesGurgaon Draft Dev Plan 2031askinganandNo ratings yet

- Mantri Developers Chairman and Award-Winning ProjectsDocument20 pagesMantri Developers Chairman and Award-Winning ProjectsAnkit GoelNo ratings yet

- List of Licenses along with the Land Schedule Hyperlink for 2011Document60 pagesList of Licenses along with the Land Schedule Hyperlink for 2011Sumit SavaraNo ratings yet

- 102 Under Construction Projects Data Gurgaon 2007-2010Document30 pages102 Under Construction Projects Data Gurgaon 2007-2010Sarvadaman Oberoi100% (1)

- Grohe Hurun IndiaDocument26 pagesGrohe Hurun IndiaAvinash TiwariNo ratings yet

- Retail Companies in IndiaDocument3 pagesRetail Companies in IndiaNitansha BhutaniNo ratings yet

- Dip JaipurDocument20 pagesDip JaipurPramesh KhatanaNo ratings yet

- Crisil SmeDocument60 pagesCrisil SmeUtkarsh PandeyNo ratings yet

- Hyderabad Achieving New MilestonesDocument16 pagesHyderabad Achieving New MilestonesRushabh ShahNo ratings yet

- Client ListDocument1 pageClient ListshivshankaricwaiNo ratings yet

- Burgundy Private Hurun India 500Document37 pagesBurgundy Private Hurun India 500Bhurishrwa AbhishekNo ratings yet

- List of IncubatorsDocument10 pagesList of IncubatorsakashNo ratings yet

- List of companies with addresses in Delhi NCR regionDocument10 pagesList of companies with addresses in Delhi NCR regionAyesha NasirNo ratings yet

- ITAT hearing on capital gains and jurisdiction of 153B assessmentDocument64 pagesITAT hearing on capital gains and jurisdiction of 153B assessmentParas GuliaNo ratings yet

- VCE Summer Internship Program 2020: Sandeep Dwivedi SM02 Project FinanceDocument3 pagesVCE Summer Internship Program 2020: Sandeep Dwivedi SM02 Project Financesandeep dwivedi100% (1)

- List of Hedge Funds CompaniesDocument24 pagesList of Hedge Funds CompaniesSrini VasanNo ratings yet

- NCR Off 2q19Document2 pagesNCR Off 2q19Siddharth GulatiNo ratings yet

- New Gurgaon: Real Insights: Locality SnapshotDocument24 pagesNew Gurgaon: Real Insights: Locality Snapshotshiv vaibhavNo ratings yet

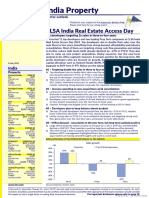

- India Property: CLSA India Real Estate Access DayDocument21 pagesIndia Property: CLSA India Real Estate Access DayManideep KumarNo ratings yet

- Contractor List June15Document32 pagesContractor List June15MINAKSHI SINGHNo ratings yet

- Faridabad Project Development FinalDocument24 pagesFaridabad Project Development Finalrideptsinghal05No ratings yet

- RAJKOTDocument4 pagesRAJKOTAnkita MishraNo ratings yet

- 202204-UBS-Real Estate Outlook US UBS April 2022Document6 pages202204-UBS-Real Estate Outlook US UBS April 2022Tianliang ZhangNo ratings yet

- Commercial Office Space - Cyber CityDocument8 pagesCommercial Office Space - Cyber CityankurNo ratings yet

- Registered Alternative Investment Funds As On Nov 13 2022Document140 pagesRegistered Alternative Investment Funds As On Nov 13 2022VenkatGuruNo ratings yet

- SEZ's in Telangana StateDocument15 pagesSEZ's in Telangana StateLokamNo ratings yet

- ProjectsDocument17 pagesProjectsA BNo ratings yet

- KR Society HyderabadDocument3 pagesKR Society HyderabadAkankshaNo ratings yet

- 2021 Pimpri ChinchwadDocument41 pages2021 Pimpri Chinchwadsanthosh100% (1)

- UKSDM List of Training Providers (MoU Signed) PDFDocument4 pagesUKSDM List of Training Providers (MoU Signed) PDFAshutosh SharmaNo ratings yet

- Builders Owners NamesDocument8 pagesBuilders Owners NamesShaju Leela GopalakrishnanNo ratings yet

- Brokers List As On 31-03-2020Document50 pagesBrokers List As On 31-03-2020pradeep Devaraj100% (1)

- Funnel Bulk SMS-GVNDocument6 pagesFunnel Bulk SMS-GVNJamie JordanNo ratings yet

- 3M India LTD: S. Noname of The Company Corporate Office Location Branch 1 2Document16 pages3M India LTD: S. Noname of The Company Corporate Office Location Branch 1 2gauravntulips8219No ratings yet

- List of Civil Contractors Registered in The CIDCO LTDDocument26 pagesList of Civil Contractors Registered in The CIDCO LTDParth DamaNo ratings yet

- Bangalore Residential Market Report April 2012 PDFDocument44 pagesBangalore Residential Market Report April 2012 PDFPonchuNo ratings yet

- Ficci FinalDocument22 pagesFicci FinalJimit ShahNo ratings yet

- 21st century legend type L1/13 addresses in DelhiDocument98 pages21st century legend type L1/13 addresses in DelhiSB Brijesh0% (1)

- Hyderabad Real EstateDocument30 pagesHyderabad Real EstateSriyaja SriNo ratings yet

- Top Real Estate Companies in BangaloreDocument10 pagesTop Real Estate Companies in BangaloreSijo JosephNo ratings yet

- 29th CREDAI-MCHI Property and Housing Finance Expo 2019Document67 pages29th CREDAI-MCHI Property and Housing Finance Expo 2019Mithun LokareNo ratings yet

- Stellar One: GH-09, Sector-1, Greater Noida WestDocument7 pagesStellar One: GH-09, Sector-1, Greater Noida WestRavi BhattacharyaNo ratings yet

- Yamuna ExpresswayDocument23 pagesYamuna ExpresswayvarshaNo ratings yet

- Updated Indian Resi Real Estate Overview - V2Document14 pagesUpdated Indian Resi Real Estate Overview - V2yashNo ratings yet

- Bangalore Startups Companies List Part 2 Aman Barnwal 1669265122Document77 pagesBangalore Startups Companies List Part 2 Aman Barnwal 16692651221DS19CS050 GM LohithNo ratings yet

- DefaulterDocument269 pagesDefaulterKrish Arjun100% (1)

- NBCC Common Application FormDocument7 pagesNBCC Common Application FormAditya GoenkaNo ratings yet

- Dawn of Future Cities of IndiaDocument21 pagesDawn of Future Cities of IndiaGOUTHAM G.KNo ratings yet

- We Have Ample Intellectual Capacity To Solve Our Challenges. IITs Are The Pride of Our Country. They Are Breeding Ground For AcademicDocument2 pagesWe Have Ample Intellectual Capacity To Solve Our Challenges. IITs Are The Pride of Our Country. They Are Breeding Ground For Academicsaururja saururjaNo ratings yet

- LkjihygyfDocument2 pagesLkjihygyfsaururja saururjaNo ratings yet

- Sustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem ServicesDocument3 pagesSustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem Servicessaururja saururjaNo ratings yet

- Sustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem ServicesDocument3 pagesSustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem Servicessaururja saururjaNo ratings yet

- Sustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem ServicesDocument3 pagesSustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem Servicessaururja saururjaNo ratings yet

- Year End Review - 2019 of Ministry of Corporate AffairsDocument4 pagesYear End Review - 2019 of Ministry of Corporate Affairssaururja saururjaNo ratings yet

- Should Not Become A Casualty of Development Addresses 62nd Convocation of Sardar Patel University The One Who Follows Sardar Patel'sDocument2 pagesShould Not Become A Casualty of Development Addresses 62nd Convocation of Sardar Patel University The One Who Follows Sardar Patel'ssaururja saururjaNo ratings yet

- List of HR Persons (Companies) (Ascending Order)Document9 pagesList of HR Persons (Companies) (Ascending Order)varma5110% (1)

- Sustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem ServicesDocument3 pagesSustainable Way, Minimising The Adverse Impact of Mining and Mitigating It For Further Ecosystem Servicessaururja saururjaNo ratings yet

- OSFC Godown Space Rent EOIDocument2 pagesOSFC Godown Space Rent EOIsaururja saururjaNo ratings yet

- Vice President Lauds Gujarat Police For 33 Percent Reservation For Women, Asks All States To Follow The SameDocument3 pagesVice President Lauds Gujarat Police For 33 Percent Reservation For Women, Asks All States To Follow The Samesaururja saururjaNo ratings yet

- National Institute of Ani Health.Document2 pagesNational Institute of Ani Health.saururja saururjaNo ratings yet

- Trade and Investments Here Today. Discussions Centred Around Enhancing Composite Engagement in Both Energy and Steel Sector To Further Help Elevate The Multidimensional Bilateral TiesDocument3 pagesTrade and Investments Here Today. Discussions Centred Around Enhancing Composite Engagement in Both Energy and Steel Sector To Further Help Elevate The Multidimensional Bilateral Tiessaururja saururjaNo ratings yet

- The Vice President Advocates For Gender Studies in Educational InstitutionsDocument6 pagesThe Vice President Advocates For Gender Studies in Educational Institutionssaururja saururjaNo ratings yet

- Shri Dharmendra Pradhan Meets Japanese Minister For Economy, Trade and Industry - Calls For Enhancing Japanese Investments, Technology and Capital in Energy and Steel Sectors PDFDocument3 pagesShri Dharmendra Pradhan Meets Japanese Minister For Economy, Trade and Industry - Calls For Enhancing Japanese Investments, Technology and Capital in Energy and Steel Sectors PDFsaururja saururjaNo ratings yet

- Rashtriya Gokul MissionDocument2 pagesRashtriya Gokul Missionsaururja saururjaNo ratings yet

- Shri Dharmendra Pradhan Meets Japanese Minister For Economy, Trade and Industry - Calls For Enhancing Japanese Investments, Technology and Capital in Energy and Steel Sectors PDFDocument3 pagesShri Dharmendra Pradhan Meets Japanese Minister For Economy, Trade and Industry - Calls For Enhancing Japanese Investments, Technology and Capital in Energy and Steel Sectors PDFsaururja saururjaNo ratings yet

- Press Information Bureau Government of India Ministry of Rural DevelopmentDocument2 pagesPress Information Bureau Government of India Ministry of Rural Developmentsaururja saururjaNo ratings yet

- GoI clears misgivings over proposed amendments to Indian Forest Act, tribal rights to be protectedDocument3 pagesGoI clears misgivings over proposed amendments to Indian Forest Act, tribal rights to be protectedsaururja saururjaNo ratings yet

- CodeForHonorFinals PDFDocument1 pageCodeForHonorFinals PDFsaururja saururjaNo ratings yet

- NDSAP (National Data Sharing & Accessibility Policy) & Open Data INDIADocument2 pagesNDSAP (National Data Sharing & Accessibility Policy) & Open Data INDIAsaururja saururjaNo ratings yet

- Rajya Sabha - Annexures to Parliamentary QuestionsDocument7 pagesRajya Sabha - Annexures to Parliamentary Questionssaururja saururjaNo ratings yet

- Hunter HaatDocument3 pagesHunter Haatsaururja saururjaNo ratings yet

- Web Ratna Awards 2014: Nominations Open for E-Governance RecognitionDocument1 pageWeb Ratna Awards 2014: Nominations Open for E-Governance Recognitionsaururja saururjaNo ratings yet

- Press Information Bureau Government of India Ministry of Science & TechnologyDocument2 pagesPress Information Bureau Government of India Ministry of Science & Technologysaururja saururjaNo ratings yet

- BRICS Countries Bring Stability & Balance in An Uncertain World Focus On Trade As Catalyst of Development - Piyush GoyalDocument2 pagesBRICS Countries Bring Stability & Balance in An Uncertain World Focus On Trade As Catalyst of Development - Piyush Goyalsaururja saururjaNo ratings yet

- DPIIT Establishes Development Council For BicycleDocument2 pagesDPIIT Establishes Development Council For Bicyclesaururja saururjaNo ratings yet

- India Will Emerge As The Torchbearer of Banking Reforms, Says Dr. Jitendra SinghDocument2 pagesIndia Will Emerge As The Torchbearer of Banking Reforms, Says Dr. Jitendra Singhsaururja saururjaNo ratings yet

- "Creation of UT of J&K and Ladakh Historic, Opened The Flood Gates of Development and Progress in The Region" - Dr. Jitendra SinghDocument1 page"Creation of UT of J&K and Ladakh Historic, Opened The Flood Gates of Development and Progress in The Region" - Dr. Jitendra Singhsaururja saururjaNo ratings yet

- The Vice President Calls Upon Youth To Overcome Apprehensions and Pledge To Donate OrgansDocument5 pagesThe Vice President Calls Upon Youth To Overcome Apprehensions and Pledge To Donate Organssaururja saururjaNo ratings yet

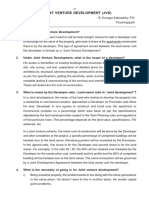

- K.Sabapathy-Joint Venture Development.1 PDFDocument9 pagesK.Sabapathy-Joint Venture Development.1 PDFEla SimyunnNo ratings yet

- Template Road Carbon Style XL A4 TubeMiterDocument26 pagesTemplate Road Carbon Style XL A4 TubeMiterRahul ManavalanNo ratings yet

- Property, Plant and Equipment (With Answers)Document16 pagesProperty, Plant and Equipment (With Answers)gazer beamNo ratings yet

- Paper 8 - DisneyDocument4 pagesPaper 8 - DisneyMaulida KusumaningsariNo ratings yet

- Part 7 The Price System and The Micro Economy A2 Level 2017 (New)Document129 pagesPart 7 The Price System and The Micro Economy A2 Level 2017 (New)Jennifer YoshuaraNo ratings yet

- Prints India V Springer India Private Limited OthersDocument23 pagesPrints India V Springer India Private Limited OthersChirag AgrawalNo ratings yet

- KomatsuDocument2 pagesKomatsuAkansha SaxenaNo ratings yet

- Solid Mettle CRISILDocument40 pagesSolid Mettle CRISILRamanan ChandrasekaranNo ratings yet

- Group 1 LenovoDocument17 pagesGroup 1 LenovoGULAM GOUSHNo ratings yet

- 9 Rules of Research - NDRDocument28 pages9 Rules of Research - NDRnbfbr536100% (1)

- Mock Exam MG T Acct 2019Document3 pagesMock Exam MG T Acct 2019Lê Việt HoàngNo ratings yet

- Practical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingDocument23 pagesPractical Relative-Value Volatility Trading: Stephen Blyth, Managing Director, Head of European Arbitrage TradingArtur SilvaNo ratings yet

- Camargo v. AbbVieDocument103 pagesCamargo v. AbbVieCrainsChicagoBusinessNo ratings yet

- Fall 2023 - FIN630 - 1Document3 pagesFall 2023 - FIN630 - 1nabila qayyumNo ratings yet

- Bijay Kumar MohantyDocument4 pagesBijay Kumar Mohantybmohanty97No ratings yet

- Pricing in FashionDocument21 pagesPricing in FashionarushiparasharNo ratings yet

- Principles OF AccountsDocument9 pagesPrinciples OF AccountsdonNo ratings yet

- Test Bank For Microeconomics Canada in The Global Environment 8th Canadian Edition ParkinDocument36 pagesTest Bank For Microeconomics Canada in The Global Environment 8th Canadian Edition Parkinsiltcheaply3iyz100% (32)

- Marketing Process DefinitionDocument6 pagesMarketing Process Definitionizzah_nadiahNo ratings yet

- Price Skimming - Wikipedia, The Free EncyclopediaDocument3 pagesPrice Skimming - Wikipedia, The Free Encyclopedia92SgopeNo ratings yet

- Promissory NotesDocument7 pagesPromissory NotesShenina ManaloNo ratings yet

- De-Listing of A Listed CompanyDocument14 pagesDe-Listing of A Listed CompanyVrinda GargNo ratings yet

- Chap 5Document8 pagesChap 5Aman Kumar SaranNo ratings yet

- JSW New Final ProjetDocument48 pagesJSW New Final ProjetRajender SinghNo ratings yet

- More Power Southeast Asia and India Lifetime Services Plus: GE Energy Jenbacher Gas Engines Issue 3/2009Document50 pagesMore Power Southeast Asia and India Lifetime Services Plus: GE Energy Jenbacher Gas Engines Issue 3/2009boeingAH64No ratings yet