You might also like

- Advanced Level: Saving vs. Inves NGDocument7 pagesAdvanced Level: Saving vs. Inves NGJames Wellington [STUDENT]No ratings yet

- Investing Tips: Lesson 18: Student Activity Sheet 1Document3 pagesInvesting Tips: Lesson 18: Student Activity Sheet 1GONZALO JIMENEZ MORALESNo ratings yet

- Investing Tips StudentDocument4 pagesInvesting Tips Studentapi-538376298No ratings yet

- Investing and Finance PresentationDocument22 pagesInvesting and Finance Presentationanmol goelNo ratings yet

- Financial Planning Guide 2021Document2 pagesFinancial Planning Guide 2021Finn KevinNo ratings yet

- PDF 1640 PDFDocument3 pagesPDF 1640 PDFKen PioNo ratings yet

- CohenSteers Senior Variable 2019-3 FCDocument2 pagesCohenSteers Senior Variable 2019-3 FCA RNo ratings yet

- If Warren Buffett Started Today, Could He Still Reach His Current Level of Wealth? (ANALYSIS)Document10 pagesIf Warren Buffett Started Today, Could He Still Reach His Current Level of Wealth? (ANALYSIS)Matt EbrahimiNo ratings yet

- Time Value of MoneyDocument19 pagesTime Value of MoneyQueens CarinoNo ratings yet

- MOCKTEST Personal and Family Financial ManagementDocument2 pagesMOCKTEST Personal and Family Financial ManagementyoshinokurukoNo ratings yet

- Chapter 13 Investments FundamentalsDocument11 pagesChapter 13 Investments Fundamentalssaleem razaNo ratings yet

- VUL Insurance Concepts Accreditation MaterialDocument83 pagesVUL Insurance Concepts Accreditation MaterialLady Glorien cayonNo ratings yet

- WEEK SIX Bond Valuation Part-2Document12 pagesWEEK SIX Bond Valuation Part-2kazi A.R RafiNo ratings yet

- Stocks 101Document20 pagesStocks 101kennedyjuliaNo ratings yet

- Calculating Rate Return - GuideDocument6 pagesCalculating Rate Return - GuideAbdullah ShaikhNo ratings yet

- Investement AvenuesDocument82 pagesInvestement AvenuesSunil RawatNo ratings yet

- INVEST Joel Greenblatt ClassguideDocument20 pagesINVEST Joel Greenblatt ClassguideClick LivrosNo ratings yet

- 11a. Chapter 11 - App - Ist Sem 23-24Document28 pages11a. Chapter 11 - App - Ist Sem 23-24Divyam JainNo ratings yet

- CohenSteers Covered Call 2019 3 FCDocument2 pagesCohenSteers Covered Call 2019 3 FCA RNo ratings yet

- Smarter Way To Invest For CollegeDocument26 pagesSmarter Way To Invest For CollegeChristian ChristianNo ratings yet

- 4.1 (PPT) Time Value of MoneyDocument40 pages4.1 (PPT) Time Value of MoneyblueredashbirdsNo ratings yet

- RWJ Chapter 4 DCF ValuationDocument47 pagesRWJ Chapter 4 DCF ValuationAshekin MahadiNo ratings yet

- Investment Vs SavingsDocument2 pagesInvestment Vs Savingsgaurav dedhiaNo ratings yet

- II. Investment EnvironmentDocument45 pagesII. Investment EnvironmentRay MundNo ratings yet

- 04 Handout 2Document7 pages04 Handout 2jerome cortonNo ratings yet

- Inyan TleDocument6 pagesInyan TleLeslie JimenoNo ratings yet

- Investments AssignmentDocument5 pagesInvestments Assignmentapi-276011473No ratings yet

- The Objectives of Financial Planning - 0505Document1 pageThe Objectives of Financial Planning - 0505neenashenoy0125450No ratings yet

- Awadarat Class 3Document254 pagesAwadarat Class 3Octavio GamezNo ratings yet

- FIN 244 Investor Base and Policy StatementsDocument8 pagesFIN 244 Investor Base and Policy StatementsAlex DonahueNo ratings yet

- The Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-2Document2 pagesThe Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-2A RNo ratings yet

- Course Module EngineeringEconomics2Document9 pagesCourse Module EngineeringEconomics2Maoi ReyesNo ratings yet

- Investments AssignmentDocument5 pagesInvestments Assignmentapi-276011592No ratings yet

- The Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-3Document2 pagesThe Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-3A RNo ratings yet

- 02 Time Value of Money - GRCDocument11 pages02 Time Value of Money - GRCGabrielle VizcarraNo ratings yet

- FM (Core) Long-Term FinancingDocument27 pagesFM (Core) Long-Term FinancingMeghna SharmaNo ratings yet

- Basic InvestingDocument3 pagesBasic InvestingDonald rayNo ratings yet

- BIFFPP-Step 4 CPA BermudaDocument6 pagesBIFFPP-Step 4 CPA BermudaRG-eviewerNo ratings yet

- International Financial Management Perpetual Bond: Semester Fourth 2011Document11 pagesInternational Financial Management Perpetual Bond: Semester Fourth 2011Joiya_love100% (1)

- Chapter 2 Time Value of Money Edited (Student)Document20 pagesChapter 2 Time Value of Money Edited (Student)Nguyễn Thái Minh ThưNo ratings yet

- Et WealthDocument14 pagesEt Wealthsunil.claycapitalNo ratings yet

- CH1 220Document46 pagesCH1 220Abdulrahman SaNo ratings yet

- The Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-4Document2 pagesThe Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-4A RNo ratings yet

- CohenSteersGlobalCovCall 2019-1FCDocument2 pagesCohenSteersGlobalCovCall 2019-1FCA RNo ratings yet

- Aviva (Pension) H-Av My Future Focus Growth S2Document4 pagesAviva (Pension) H-Av My Future Focus Growth S2Jason FitchNo ratings yet

- How To Start Your Investment Journey?Document59 pagesHow To Start Your Investment Journey?ElearnmarketsNo ratings yet

- The 1% Difference: Synergy Financial GroupDocument4 pagesThe 1% Difference: Synergy Financial GroupgvandykeNo ratings yet

- Ivo Welch CF IntroDocument14 pagesIvo Welch CF IntroChetan GKNo ratings yet

- 3108 13 05 Investing GN SEDocument9 pages3108 13 05 Investing GN SENEEVE SHETHNo ratings yet

- What Is Investing?: Spotlight OnDocument2 pagesWhat Is Investing?: Spotlight OnSachitNo ratings yet

- The Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-1Document2 pagesThe Cohen & Steers Equity Dividend & Income Closed-End Portfolio 2019-1A RNo ratings yet

- Investments AssignmentDocument5 pagesInvestments Assignmentapi-276122961No ratings yet

- HL A Beginners Guide To Investment Trusts 0322Document14 pagesHL A Beginners Guide To Investment Trusts 0322thomashayward00No ratings yet

- FIMM BookletDocument12 pagesFIMM BookletGoh Koon LoongNo ratings yet

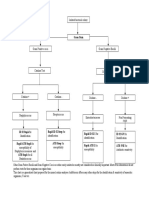

- Financial Independence Flowchart (SG Version)Document1 pageFinancial Independence Flowchart (SG Version)Alvin YeoNo ratings yet

- 2.04 What Is Stock AnywaysDocument3 pages2.04 What Is Stock AnywaysJakeFromStateFarm100% (1)

- VUL Insurance ConceptsDocument79 pagesVUL Insurance ConceptsUNEXPECTED100% (2)

- Banikanta Mishra: Financial Management Ravenshaw UniversityDocument15 pagesBanikanta Mishra: Financial Management Ravenshaw UniversitySoumya Ranjan BalNo ratings yet

- AIG AnnuitiesDocument12 pagesAIG AnnuitiesRaj JarNo ratings yet

- A Fighting Chance: The High School Finance Education Everyone DeservesFrom EverandA Fighting Chance: The High School Finance Education Everyone DeservesNo ratings yet

- Bank Exams MCQ On Computers - 1 and 2Document14 pagesBank Exams MCQ On Computers - 1 and 2Satheesh Kumar TNo ratings yet

- SBI Exam Model QuestionsDocument4 pagesSBI Exam Model QuestionsSatheesh Kumar TNo ratings yet

- GNB Identification ChartDocument1 pageGNB Identification ChartSatheesh Kumar TNo ratings yet

- SBI Exam Questions General AwarenessDocument21 pagesSBI Exam Questions General AwarenessSatheesh Kumar TNo ratings yet

- Lim Klein Team Mental Models 2006 PDFDocument16 pagesLim Klein Team Mental Models 2006 PDFSatheesh Kumar TNo ratings yet

- Micr 0008Document2 pagesMicr 0008Satheesh Kumar TNo ratings yet

- Understanding Investment StrategyDocument1 pageUnderstanding Investment StrategySatheesh Kumar TNo ratings yet

- Panchali SabathamDocument84 pagesPanchali SabathamThiyagarajan SankaranNo ratings yet

- Recovery Rate of NTM From AFB Smear-Positive Sputum Specimens at A Medical Centre in South KoreaDocument6 pagesRecovery Rate of NTM From AFB Smear-Positive Sputum Specimens at A Medical Centre in South KoreaSatheesh Kumar TNo ratings yet

- Mott PDFDocument7 pagesMott PDFSatheesh Kumar TNo ratings yet

- In Vitro Comparison of NALC-NaOH, Tween 80Document9 pagesIn Vitro Comparison of NALC-NaOH, Tween 80Satheesh Kumar TNo ratings yet

- Understanding Investment StrategyDocument1 pageUnderstanding Investment StrategySatheesh Kumar TNo ratings yet

- Difco BBL Manual SampleDocument10 pagesDifco BBL Manual SampleSatheesh Kumar TNo ratings yet

- CPF Investment Scheme (CPFIS) - Everything You Need To Know About Investing With CPFDocument11 pagesCPF Investment Scheme (CPFIS) - Everything You Need To Know About Investing With CPFSatheesh Kumar TNo ratings yet

- Article Lean SigmaDocument5 pagesArticle Lean SigmaSatheesh Kumar TNo ratings yet

- ISI Document On Gasolone Standard 2008Document37 pagesISI Document On Gasolone Standard 2008Satheesh Kumar TNo ratings yet

- Day 1Document18 pagesDay 1Satheesh Kumar TNo ratings yet

- JEM Diseases of South East AsiaDocument4 pagesJEM Diseases of South East AsiaSatheesh Kumar TNo ratings yet

- Homework For Next ClassDocument3 pagesHomework For Next ClassSimo El Kettani20% (5)

- Syl 51 1132361508Document1 pageSyl 51 1132361508arif rahmanNo ratings yet

- Question Paper of MBA Second YearDocument5 pagesQuestion Paper of MBA Second YearKaran Veer SinghNo ratings yet

- TABB Exchange TrioDocument3 pagesTABB Exchange TriotfeditorNo ratings yet

- Compounding and DiscountingDocument43 pagesCompounding and DiscountingRosalie RosalesNo ratings yet

- APC313 Assessment Brief January19Document3 pagesAPC313 Assessment Brief January19Hoài Sơn VũNo ratings yet

- Prest On Basics (F&O) - YashodhanDocument13 pagesPrest On Basics (F&O) - YashodhanAkshay SahooNo ratings yet

- Working Capital Management of Rajasthan Cooperative Dairy Federation LTD in India PDFDocument6 pagesWorking Capital Management of Rajasthan Cooperative Dairy Federation LTD in India PDFSk NagoorNo ratings yet

- The Yale Endowment Model of Investing Is Not DeadDocument8 pagesThe Yale Endowment Model of Investing Is Not DeadkeatingcapitalNo ratings yet

- Sip PDFDocument81 pagesSip PDFMayuri TetwarNo ratings yet

- ISJ047 and European CustodyDocument76 pagesISJ047 and European Custody2imediaNo ratings yet

- Convertible Bond - Credit SuisseDocument52 pagesConvertible Bond - Credit Suissenyj martin100% (1)

- Micro-Cap Review Magazine Fall 2010Document80 pagesMicro-Cap Review Magazine Fall 2010Planet MicroCap Review MagazineNo ratings yet

- Hedge Fund ActivismDocument17 pagesHedge Fund ActivismjamesNo ratings yet

- Binary Option Strategy That WorksDocument25 pagesBinary Option Strategy That Worksfrankolett100% (2)

- Consolidated Financial Statements: - Prepared From Separate FinancialDocument53 pagesConsolidated Financial Statements: - Prepared From Separate FinancialSowmeia Vasudevan100% (2)

- Ch05-How Securities Are Traded-SalaarDocument39 pagesCh05-How Securities Are Traded-SalaarAhmed Rasool BaigNo ratings yet

- Part I-Introduction (Financial Market)Document56 pagesPart I-Introduction (Financial Market)Steve Jhon James TantingNo ratings yet

- Meaning of Euro Currency Market:: The Following Factors Led To Its Growth: 1. Flow of US AidDocument3 pagesMeaning of Euro Currency Market:: The Following Factors Led To Its Growth: 1. Flow of US AidAijaz KhajaNo ratings yet

- Investment BooksDocument2 pagesInvestment BooksRohan GhoshNo ratings yet

- Forex NRE NRO NRIDocument5 pagesForex NRE NRO NRIadifaahNo ratings yet

- ICO MARKET RESEARChDocument64 pagesICO MARKET RESEARChGungaa JaltsanNo ratings yet

- WSO Resume 8Document1 pageWSO Resume 8Devin MaaNo ratings yet

- VCM - Chapter 1Document11 pagesVCM - Chapter 1belle crisNo ratings yet

- Maf 630 Chapter 1Document3 pagesMaf 630 Chapter 1Pablo EkskobaNo ratings yet

- 4603 Pirelli FY 2018 Results PresentationDocument40 pages4603 Pirelli FY 2018 Results PresentationDavide AbdelalNo ratings yet

- Summary of IAS 38Document5 pagesSummary of IAS 38Jaanu SanthiranNo ratings yet

- Risk TableDocument1 pageRisk TableJael PistioNo ratings yet

- CH 18-Revenue Recognition - KiesoDocument41 pagesCH 18-Revenue Recognition - Kiesofransiskawidya100% (1)

- Understanding Asian Kill Zone, London Manipulation, Optimum TradingDocument35 pagesUnderstanding Asian Kill Zone, London Manipulation, Optimum TradingKevin Mwaura100% (1)