You might also like

- FRM-I Valuation Models NotesDocument146 pagesFRM-I Valuation Models Notesprincelyprince100% (2)

- Lecture 1: Stochastic Volatility and Local Volatility: Jim Gatheral, Merrill LynchDocument18 pagesLecture 1: Stochastic Volatility and Local Volatility: Jim Gatheral, Merrill Lynchabhishek210585No ratings yet

- Expected Returns on Investment PortfolioDocument17 pagesExpected Returns on Investment PortfolioVipulNo ratings yet

- Valuation and Risk ModelsDocument146 pagesValuation and Risk ModelsChaituNo ratings yet

- DECISION THEORY PRESENTATION BREAKDOWNDocument32 pagesDECISION THEORY PRESENTATION BREAKDOWNAmul Shrestha100% (1)

- Sargent T., Et. Al (2010) - Practicing DynareDocument66 pagesSargent T., Et. Al (2010) - Practicing DynareMiguel Ataurima ArellanoNo ratings yet

- 2013 The Implied Volatility SurfacesDocument10 pages2013 The Implied Volatility SurfacesMikhail RadomyselskiyNo ratings yet

- CHAPTER 2 (B) - Risk Analysis and Project EvaluationDocument79 pagesCHAPTER 2 (B) - Risk Analysis and Project EvaluationSarnisha Murugeshwaran (Shazzisha)No ratings yet

- Marriott Training EvaluationsDocument6 pagesMarriott Training EvaluationsMeghapriya1234No ratings yet

- Mid Term Test BFT 64Document3 pagesMid Term Test BFT 64Ngọc LươngNo ratings yet

- Math (Regression Theory)Document31 pagesMath (Regression Theory)Alina BorysenkoNo ratings yet

- Entropy Methods for Financial DerivativesDocument42 pagesEntropy Methods for Financial DerivativesArthur DuxNo ratings yet

- Important Notes About EconometricsDocument24 pagesImportant Notes About EconometricsYoseph BekeleNo ratings yet

- Optimal Hedging of Uncertain Foreign Currency Returns: 12/12/2011 SLJ Macro Partners Fatih YilmazDocument10 pagesOptimal Hedging of Uncertain Foreign Currency Returns: 12/12/2011 SLJ Macro Partners Fatih YilmazAbhishek RamNo ratings yet

- Fitting The Smile, Smart Parameters For SABR and HestonDocument13 pagesFitting The Smile, Smart Parameters For SABR and Hestonhazerider2No ratings yet

- BANK3011 Workshop Week 5 SolutionsDocument3 pagesBANK3011 Workshop Week 5 SolutionsZahraaNo ratings yet

- Regression and Statistical TestsDocument6 pagesRegression and Statistical TestsAguinaldo Geroy JohnNo ratings yet

- Memo Chapter 3 11th Solution Manual Quantitative Analysis For ManagementDocument46 pagesMemo Chapter 3 11th Solution Manual Quantitative Analysis For ManagementKEANU JOOSTE73% (15)

- Bates - Empirical Option Pricing Models - 2021k4Document30 pagesBates - Empirical Option Pricing Models - 2021k4khrysttalexa3146No ratings yet

- Excel MPTDocument23 pagesExcel MPTBokonon22No ratings yet

- Heston Jim GatheralDocument21 pagesHeston Jim GatheralShuo YanNo ratings yet

- FM11 CH 11 Mini CaseDocument13 pagesFM11 CH 11 Mini CasesushmanthqrewrerNo ratings yet

- Risk Management Models - What To Use, and Not To Use: Peter Luk - April 2008Document14 pagesRisk Management Models - What To Use, and Not To Use: Peter Luk - April 2008donttellyouNo ratings yet

- Managerial Eco PaperDocument6 pagesManagerial Eco PaperTech TricksNo ratings yet

- Excel FunctionsDocument13 pagesExcel Functionsfhlim2069No ratings yet

- Stefanica 2017 VolDocument24 pagesStefanica 2017 VolpukkapadNo ratings yet

- AMDA Regression SolutionDocument12 pagesAMDA Regression SolutionParambrahma PandaNo ratings yet

- Abernethy and Chapman Determination of Initial Sample Size Sampling For VariablesDocument8 pagesAbernethy and Chapman Determination of Initial Sample Size Sampling For VariablesJoHn CarLoNo ratings yet

- Soa All Apm Exams for Qfic Fall 2014 副本Document147 pagesSoa All Apm Exams for Qfic Fall 2014 副本cnmouldplasticNo ratings yet

- AFM472 2011 MidtermSolutions HuangDocument16 pagesAFM472 2011 MidtermSolutions Huangsamspeed7No ratings yet

- Interest Rate Risk: Maturity Model The Price-Market Yield Relationship: A Single InstrumentDocument24 pagesInterest Rate Risk: Maturity Model The Price-Market Yield Relationship: A Single InstrumentMad_of_booksNo ratings yet

- AlbatrossDocument1 pageAlbatrossindranil biswasNo ratings yet

- Manufacturing Decisions Ranikka Moore Capella University Operations Management For Competitive Advantage November 26, 2021Document5 pagesManufacturing Decisions Ranikka Moore Capella University Operations Management For Competitive Advantage November 26, 2021ranikka mooreNo ratings yet

- EmvDocument2 pagesEmvAndika17No ratings yet

- Black Scholes ModellingDocument18 pagesBlack Scholes Modellings.archana100% (1)

- Single Index ModelDocument3 pagesSingle Index ModelPinkyChoudhary100% (1)

- Statistics For Management - A2Document11 pagesStatistics For Management - A2Ayushi PrabhuNo ratings yet

- Regression Analysis Demand EstimationDocument9 pagesRegression Analysis Demand EstimationdelisyaaamilyNo ratings yet

- Sensitivity Sample Model: Tornado, Spider and Sensitivity Charts (Nonlinear)Document6 pagesSensitivity Sample Model: Tornado, Spider and Sensitivity Charts (Nonlinear)cajimenezb8872No ratings yet

- MAS 2 Midterms Module No. 1 StudentsDocument6 pagesMAS 2 Midterms Module No. 1 StudentsJoan Marie AgnesNo ratings yet

- Decision Analysis Techniques and ModelsDocument46 pagesDecision Analysis Techniques and ModelsSunkanmi FadojuNo ratings yet

- Auto Call Able SDocument37 pagesAuto Call Able SAnkit VermaNo ratings yet

- Exercises For Chapter 6 of Vinod's " Hands-On Intermediate Econometrics Using R"Document25 pagesExercises For Chapter 6 of Vinod's " Hands-On Intermediate Econometrics Using R"damian camargoNo ratings yet

- Mean of Discrete Random VariableDocument25 pagesMean of Discrete Random VariableAngelica BuquelNo ratings yet

- Example 2Document7 pagesExample 2Thái TranNo ratings yet

- Data Management With Voice OverDocument38 pagesData Management With Voice OverMarjorie NepomucenoNo ratings yet

- Cla 22222222 FinanceDocument21 pagesCla 22222222 FinanceSneha MaharjanNo ratings yet

- Decision Science AssignmentDocument9 pagesDecision Science AssignmentBhagyashree NagarkarNo ratings yet

- Pmlect 2 BDocument24 pagesPmlect 2 BThe Learning Solutions Home TutorsNo ratings yet

- Gatheral ArbFreeImplVolParameterizationDocument41 pagesGatheral ArbFreeImplVolParameterizationginovainmonaNo ratings yet

- Decision Recognizing Risks: Topic 5Document24 pagesDecision Recognizing Risks: Topic 5Jayson Dela Cruz OmictinNo ratings yet

- The Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsDocument27 pagesThe Dynamics of Financial Markets: Fibonacci Numbers, Elliott Waves, and SolitonsHakimi BobNo ratings yet

- Dynamic Hedging in A Volatile MarketDocument9 pagesDynamic Hedging in A Volatile Marketmirando93No ratings yet

- ChallengeDocument30 pagesChallengesanucwa6932No ratings yet

- FINANCIAL DERIVATIVESDocument30 pagesFINANCIAL DERIVATIVESBevNo ratings yet

- Using Calculator Casio AU PLUSDocument8 pagesUsing Calculator Casio AU PLUSzapelNo ratings yet

- Chapter 4 Demand EstimationDocument8 pagesChapter 4 Demand Estimationmyra0% (1)

- Quant Method Unit 1 Notes Hu-Jean RussellDocument2 pagesQuant Method Unit 1 Notes Hu-Jean RussellHu-Jean RussellNo ratings yet

- KentDocument5 pagesKentharsh guptaNo ratings yet

- Industry Analysis of AirBnbDocument1 pageIndustry Analysis of AirBnbharsh guptaNo ratings yet

- SDGsDocument21 pagesSDGsharsh guptaNo ratings yet

- Business Law ProjectDocument35 pagesBusiness Law Projectharsh guptaNo ratings yet

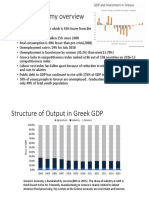

- Greece Economy OverviewDocument2 pagesGreece Economy Overviewharsh guptaNo ratings yet

- FM Final ProjectDocument21 pagesFM Final Projectharsh guptaNo ratings yet

- Calculating Implied Volatility Using Black-Scholes ModelsDocument4 pagesCalculating Implied Volatility Using Black-Scholes Modelsharsh guptaNo ratings yet

- Best Option Trading Strategies For Indian MarketsDocument2 pagesBest Option Trading Strategies For Indian Marketssantanu_1310No ratings yet

- Class 3Document73 pagesClass 3Geoffrey MwangiNo ratings yet

- Option Market MakingDocument45 pagesOption Market Makingchuff6675100% (1)

- Investment Basics I: ObjectivesDocument14 pagesInvestment Basics I: Objectivesno nameNo ratings yet

- UNICON Insurance FormDocument2 pagesUNICON Insurance FormJiezel VillanuevaNo ratings yet

- Ins 22 Chapter 1 2 3 4 With AnswersDocument28 pagesIns 22 Chapter 1 2 3 4 With Answersgcr007No ratings yet

- Bankers Trust Case StudyDocument19 pagesBankers Trust Case StudySedeqha PopalNo ratings yet

- Commercial Reviewer 2022Document8 pagesCommercial Reviewer 2022Ceedee RagayNo ratings yet

- Companies Equity Share Questions Class 12thDocument19 pagesCompanies Equity Share Questions Class 12thambika9290No ratings yet

- The Life Cycle of a TradeDocument98 pagesThe Life Cycle of a Trademox222No ratings yet

- Louise Bedford Trading InsightsDocument80 pagesLouise Bedford Trading Insightsartendu100% (3)

- Wa0003.Document1 pageWa0003.mitricarobert83No ratings yet

- Module 3 Yr. 2017Document89 pagesModule 3 Yr. 2017Xaky ODNo ratings yet

- BBCF3153: Mid Term TestDocument6 pagesBBCF3153: Mid Term TestTebashiniNo ratings yet

- Entry Age Normal Method For Defined Benefit Pension Funding: International Conference On Statistics and Analytics 2019Document12 pagesEntry Age Normal Method For Defined Benefit Pension Funding: International Conference On Statistics and Analytics 2019Kartika ShantiNo ratings yet

- Option Pricing Models - BinomialDocument10 pagesOption Pricing Models - BinomialSahinNo ratings yet

- Hedging Techniques in Indian Stock Market-Indiabulls (1) - FinalDocument108 pagesHedging Techniques in Indian Stock Market-Indiabulls (1) - FinalUpendra SaiNo ratings yet

- CH 06 Hull Fundamentals 9 TH EdDocument30 pagesCH 06 Hull Fundamentals 9 TH EdIbrahim KhatatbehNo ratings yet

- Soeren Skov Hansen PDFDocument101 pagesSoeren Skov Hansen PDFpkdeyiitkgpNo ratings yet

- Long Call Repair Stratergy Me & Go Option Adjustment SchoolDocument6 pagesLong Call Repair Stratergy Me & Go Option Adjustment SchoolpkkothariNo ratings yet

- Quotation - Householders - LAPSONDocument1 pageQuotation - Householders - LAPSONCredsureNo ratings yet

- Fin512 习题1Document21 pagesFin512 习题1Biao Wang100% (1)

- A Quick Guide To Asset Swaps: What Is An Asset Swap? What Are The Advantages of Asset Swaps?Document1 pageA Quick Guide To Asset Swaps: What Is An Asset Swap? What Are The Advantages of Asset Swaps?Damian WalężakNo ratings yet

- Car Policy 2022 - 2023Document2 pagesCar Policy 2022 - 2023Shakshi TomarNo ratings yet

- Insurance ServicesDocument2 pagesInsurance ServicesKameswara Rao PorankiNo ratings yet

- Citi Deal Pricing HistoryDocument1 pageCiti Deal Pricing HistoryykkwonNo ratings yet

- Yields, Swaps, & Corp Fin Teaching with BloombergDocument20 pagesYields, Swaps, & Corp Fin Teaching with BloombergHkn YılmazNo ratings yet

- Quotation For Optima SecureDocument2 pagesQuotation For Optima SecureHritik SharmaNo ratings yet

- Policy DocumentDocument3 pagesPolicy Documentsunil dhangarNo ratings yet

- Derivative Securities Course OutlineDocument5 pagesDerivative Securities Course OutlineMohammad Latef Al-AlsheikhNo ratings yet