You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Solutions To Capital Budgeting Practice ProblemsDocument0 pagesSolutions To Capital Budgeting Practice Problemssalehin1969No ratings yet

- Section - 49 Markov Chain Steady State PDFDocument19 pagesSection - 49 Markov Chain Steady State PDFArun SircarNo ratings yet

- NLP - Mind To MuscleDocument4 pagesNLP - Mind To MuscleMark K. Francis100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Time Value of MoneyDocument27 pagesTime Value of MoneyRishab KapurNo ratings yet

- Adv Investment Appraisal 2Document44 pagesAdv Investment Appraisal 2kuttan1000100% (1)

- Boosting Cattle Supply Through FatteningDocument25 pagesBoosting Cattle Supply Through FatteningaklilNo ratings yet

- Capital Budgeting AssignmentDocument3 pagesCapital Budgeting AssignmentRobert JohnsonNo ratings yet

- Project Feasibility Study Key to Sustainable ConstructionDocument6 pagesProject Feasibility Study Key to Sustainable ConstructionNhan DoNo ratings yet

- UnlockedDocument45 pagesUnlockedmanojNo ratings yet

- PMP Formulas Pocket GuideDocument2 pagesPMP Formulas Pocket GuideTalha FarooqiNo ratings yet

- Case StudyDocument7 pagesCase StudyPatricia TabalonNo ratings yet

- Assignments-Mba Sem-Ii: Subject Code: MB0029Document28 pagesAssignments-Mba Sem-Ii: Subject Code: MB0029Mithesh KumarNo ratings yet

- BFMDocument28 pagesBFMPratik RambhiaNo ratings yet

- CF Remdial AssignmentDocument5 pagesCF Remdial AssignmentMadhav RajbanshiNo ratings yet

- Disposition and Renovation of Income Properties True/FalseDocument6 pagesDisposition and Renovation of Income Properties True/FalseSiu RebeccaNo ratings yet

- Techno-Economic Analysis of Cloud RAN DeploymentDocument146 pagesTechno-Economic Analysis of Cloud RAN DeploymentMikatechNo ratings yet

- 09 Capital Budgeting TechniquesDocument31 pages09 Capital Budgeting TechniquesMo Mindalano Mandangan100% (3)

- Excel Practise WorkDocument52 pagesExcel Practise WorkanbugobiNo ratings yet

- Costbenefit Analysis 2015Document459 pagesCostbenefit Analysis 2015TRÂM NGUYỄN THỊ BÍCHNo ratings yet

- NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA - Chapter 08Document16 pagesNET PRESENT VALUE AND OTHER INVESTMENT CRITERIA - Chapter 08zordan100% (1)

- Project Management Quiz: Key ConceptsDocument14 pagesProject Management Quiz: Key Conceptssonali bhosaleNo ratings yet

- Bangladesh Open University: BBA Program Semester: 211 (5 Level)Document13 pagesBangladesh Open University: BBA Program Semester: 211 (5 Level)SABBIR AHMEDNo ratings yet

- Chapter 12Document76 pagesChapter 123ooobd1234No ratings yet

- Excel Templates: What Every Real Estate Investor Needs To Know About Cash FlowDocument23 pagesExcel Templates: What Every Real Estate Investor Needs To Know About Cash FlowABHIJEET GAJRENo ratings yet

- Capital Budgeting Report FinalDocument15 pagesCapital Budgeting Report FinalCezar SabladNo ratings yet

- 2 - INTRO TO Financial FSDocument19 pages2 - INTRO TO Financial FSmuhammad akbar bahmiNo ratings yet

- DPP of Construction of Women Prayer Room in Dhaka CityDocument7 pagesDPP of Construction of Women Prayer Room in Dhaka CityShazida Khanam IshitaNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinancejahidkhanNo ratings yet

- University of Pune Oct - 2005, Mba III Sem - Question PaperDocument40 pagesUniversity of Pune Oct - 2005, Mba III Sem - Question PaperSonali BangarNo ratings yet

- New Jersey Task Force On EDA Tax Incentives Third ReportDocument110 pagesNew Jersey Task Force On EDA Tax Incentives Third ReportWHYY NewsNo ratings yet

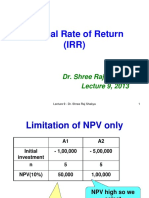

- Lecture9 IRRDocument29 pagesLecture9 IRRsuraj bhandariNo ratings yet

- Basic Methods for Engineering Economy StudiesDocument3 pagesBasic Methods for Engineering Economy Studiesxxkooonxx100% (1)

- Problem Set - AssignmentDocument6 pagesProblem Set - AssignmentKalyan VemparalaNo ratings yet