You might also like

- PP12201710731 HDFC Life ClassicAssure Plus Retail BrochureDocument6 pagesPP12201710731 HDFC Life ClassicAssure Plus Retail BrochureNatuskar pranitNo ratings yet

- HDFC Life Sampoorn Samridhi Plus - Brochure PDFDocument12 pagesHDFC Life Sampoorn Samridhi Plus - Brochure PDFmonicaNo ratings yet

- Guaranteed Savings Insurance PlanDocument5 pagesGuaranteed Savings Insurance PlanAnoop MannadathilNo ratings yet

- PP12201710730 HDFC Life Sampoorn Samridhi Plus Retail BrochureDocument16 pagesPP12201710730 HDFC Life Sampoorn Samridhi Plus Retail BrochureFuse BulbNo ratings yet

- PP06201811428 HDFC Life Sanchay (Standard) Retail - Brochure PDFDocument8 pagesPP06201811428 HDFC Life Sanchay (Standard) Retail - Brochure PDFDjddhNo ratings yet

- 5032-Sanchay Broucher PDFDocument8 pages5032-Sanchay Broucher PDFChandanNo ratings yet

- ICICI Pru Savings SurakshaDocument8 pagesICICI Pru Savings SurakshaRojan G JosephNo ratings yet

- ICICI Pru Savings SurakshaDocument8 pagesICICI Pru Savings SurakshabindalmohitNo ratings yet

- ICICI Savings SurakshaDocument8 pagesICICI Savings SurakshaNipun JainNo ratings yet

- MoneyBackPlus BrochureDocument7 pagesMoneyBackPlus BrochuremanjugnpNo ratings yet

- HDFC Life Click 2 InvestDocument7 pagesHDFC Life Click 2 InvestShaik BademiyaNo ratings yet

- SBI Life - Smart Platina Assure - BrochureDocument12 pagesSBI Life - Smart Platina Assure - Brochuresourav agarwalNo ratings yet

- Bajaj Allianz Guarantee Assure: A Non-Linked Endowment PlanDocument9 pagesBajaj Allianz Guarantee Assure: A Non-Linked Endowment PlanBhaskarNo ratings yet

- Life Insurance BrouchureDocument2 pagesLife Insurance BrouchureGuru9756No ratings yet

- HDFC Life Smart Protect Plan BrochureDocument24 pagesHDFC Life Smart Protect Plan BrochureBharat KalraNo ratings yet

- Tata AIA Life Insurance MoneyBackPlus BrochureDocument6 pagesTata AIA Life Insurance MoneyBackPlus BrochureasfakpaliwalaNo ratings yet

- Dhan Varsha BrochureDocument16 pagesDhan Varsha BrochureJanagiramanNo ratings yet

- Wealth Gain Insurance Plan Brochure V03Document30 pagesWealth Gain Insurance Plan Brochure V03rajlal88No ratings yet

- Edelweiss Tokio Life Wealth Accumulation AcceleratedCover V01 BrochureDocument10 pagesEdelweiss Tokio Life Wealth Accumulation AcceleratedCover V01 BrochureavisekgNo ratings yet

- HDFC Life Smart Protect Plan BrochureDocument24 pagesHDFC Life Smart Protect Plan BrochureanishNo ratings yet

- FAMILY INCOME SECURITY - by ENTERPRISE LIFEDocument10 pagesFAMILY INCOME SECURITY - by ENTERPRISE LIFEemmanuelNo ratings yet

- Smart - Platina - Assure - Brochure - Brand ReimagineDocument12 pagesSmart - Platina - Assure - Brochure - Brand ReimaginepankajNo ratings yet

- ICICI Pru Signature Online Brochure 230331 150752Document30 pagesICICI Pru Signature Online Brochure 230331 150752Tamil PokkishamNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- ICICI Pru Signature Online BrochureDocument30 pagesICICI Pru Signature Online Brochuremyhomemitv2uNo ratings yet

- Max Life Monthly Income Advantage Plan ProspectusDocument11 pagesMax Life Monthly Income Advantage Plan Prospectushemantchawla89No ratings yet

- Contract MahalifegoldDocument6 pagesContract MahalifegoldLohitRamakrishnaKotapatiNo ratings yet

- HDFC ProGrowth Flexi Retail Brochure-PP10201710535Document9 pagesHDFC ProGrowth Flexi Retail Brochure-PP10201710535Girish HemnaniNo ratings yet

- Dhan Varsha BrochureDocument16 pagesDhan Varsha Brochuresunny20009No ratings yet

- PP10201710535 HDFC ProGrowth Flexi Retail BrochureDocument9 pagesPP10201710535 HDFC ProGrowth Flexi Retail Brochuresigmadelhi87No ratings yet

- Savings Advantage Plan LeafletDocument2 pagesSavings Advantage Plan LeafletNishanthNo ratings yet

- Put Your Financial Life On Autopilot With Guaranteed BenefitsDocument12 pagesPut Your Financial Life On Autopilot With Guaranteed BenefitsRengarajan ThiruvengadaswamyNo ratings yet

- ProGrowth Flexi 2Document8 pagesProGrowth Flexi 2madhurima paulNo ratings yet

- ICICI Future Perfect - BrochureDocument11 pagesICICI Future Perfect - BrochureChandan Kumar SatyanarayanaNo ratings yet

- Save, Invest & Protect Your FutureDocument2 pagesSave, Invest & Protect Your Futureemaraty khNo ratings yet

- Future PerfectDocument11 pagesFuture PerfectAditi SinghNo ratings yet

- IDBI Federal Lifesurance Savings Insurance PlanDocument16 pagesIDBI Federal Lifesurance Savings Insurance PlanKumarniksNo ratings yet

- Rakshakaran: A Non Linked, Participating, Whole Life Individual Savings PlanDocument6 pagesRakshakaran: A Non Linked, Participating, Whole Life Individual Savings PlanHemant ShakyaNo ratings yet

- Jeevan Nivesh CanarahsbcDocument14 pagesJeevan Nivesh CanarahsbcVinesh ChandraNo ratings yet

- PNB Metlife Saving PlanDocument6 pagesPNB Metlife Saving PlanPurnima PurohitNo ratings yet

- Terms and Conditions Sampoorna Raksha Plus PDFDocument11 pagesTerms and Conditions Sampoorna Raksha Plus PDFSanthi Swetha PudhotaNo ratings yet

- Bima Gold by Lic of India - 9811896425Document3 pagesBima Gold by Lic of India - 9811896425Harish ChandNo ratings yet

- IPru Signature Online Brochure PDFDocument28 pagesIPru Signature Online Brochure PDFAjeet ThakurNo ratings yet

- Invest Once-BrochureDocument13 pagesInvest Once-BrochureSai KumarNo ratings yet

- HDFC Life Guaranteed Pension Plan20170517 102654Document6 pagesHDFC Life Guaranteed Pension Plan20170517 102654Bhavik PrajapatiNo ratings yet

- HDFC Life Smart Pension Plan BrochureDocument17 pagesHDFC Life Smart Pension Plan BrochureSatyajeet AnandNo ratings yet

- IndiaFirst Smart Save Plan BrochureDocument16 pagesIndiaFirst Smart Save Plan BrochureVishal SharmaNo ratings yet

- Magnum Fortune Plus Plan-Bajaj AllianzeDocument18 pagesMagnum Fortune Plus Plan-Bajaj AllianzeDwarkesh PanchalNo ratings yet

- IPru ASIP EnglishDocument6 pagesIPru ASIP Englishpradeep kumarNo ratings yet

- Secure Income PlanDocument15 pagesSecure Income PlanSuyash PrasadNo ratings yet

- Premier Endowment PlanDocument12 pagesPremier Endowment Planumar zaid khanNo ratings yet

- IPru Sarv Jana Suraksha BrochureDocument6 pagesIPru Sarv Jana Suraksha BrochureyesindiacanngoNo ratings yet

- The M. S.University of Baroda - Faculty of Commerce Personal Finance & Investment Unit III - Insurance and Retirement PlanningDocument16 pagesThe M. S.University of Baroda - Faculty of Commerce Personal Finance & Investment Unit III - Insurance and Retirement PlanningSocio Fact'sNo ratings yet

- Future Wealth GainDocument23 pagesFuture Wealth GainSudhirGajareNo ratings yet

- Brochure Shriram Assured Income Plus OnlineDocument12 pagesBrochure Shriram Assured Income Plus OnlineSivaramakrishna Davuluri100% (1)

- Max Life Fast Trak Super LeafletDocument4 pagesMax Life Fast Trak Super Leafletmantoo kumarNo ratings yet

- DownloadDocument4 pagesDownloadiamshonalidixitNo ratings yet

- Assured Money Back BrochureDocument10 pagesAssured Money Back BrochureTaksh DhamiNo ratings yet

- Brochure Shriram Assured Income Plan OfflineDocument7 pagesBrochure Shriram Assured Income Plan OfflineSivaramakrishna DavuluriNo ratings yet

- Dont Pay With Itunes Gift Cards FinalDocument1 pageDont Pay With Itunes Gift Cards FinalJack WilliamsNo ratings yet

- Digital Marketing Resume PDFDocument2 pagesDigital Marketing Resume PDFKavya Mirji100% (1)

- Power User Training Sign-Off Sheet Financial Accounting: 15 June 2010 - 23 JUNE 2010Document5 pagesPower User Training Sign-Off Sheet Financial Accounting: 15 June 2010 - 23 JUNE 2010Omer Farooq KhanNo ratings yet

- Retail Vs Etail - Supply ChainDocument1 pageRetail Vs Etail - Supply ChainTarunendra Pratap SinghNo ratings yet

- DATASHEET - ZPA Private-Service-EdgeDocument4 pagesDATASHEET - ZPA Private-Service-EdgeCansel ÖzcanNo ratings yet

- TicketsDocument1 pageTicketsGladys MalekarNo ratings yet

- Roadmap Statement of Cash FlowsDocument134 pagesRoadmap Statement of Cash FlowsNabil BouraïmaNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument6 pagesMobile Services: Your Account Summary This Month'S ChargesManjul SinghNo ratings yet

- Đề cương KTQTDocument6 pagesĐề cương KTQTNguyễn Thị Hồng HạnhNo ratings yet

- Cover LetterDocument2 pagesCover LetterAmos OnhanNo ratings yet

- SIGTRAN Telecom ProtocolDocument2 pagesSIGTRAN Telecom ProtocolJitender YadavNo ratings yet

- Accounting Policies & Procedures ManualDocument335 pagesAccounting Policies & Procedures ManualPlatonic100% (23)

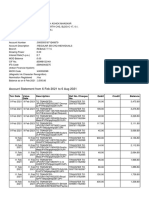

- Account Statement From 6 Feb 2021 To 6 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 6 Feb 2021 To 6 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSantosh MhaskarNo ratings yet

- Accounts Receivable and Receivable FinancingDocument4 pagesAccounts Receivable and Receivable FinancingLui50% (2)

- Tiket Baru PDFDocument1 pageTiket Baru PDFMohamad Shafiq Saleh UddinNo ratings yet

- SCD Isupplier Final VDocument24 pagesSCD Isupplier Final VFeqede hambisaNo ratings yet

- Vdocuments - MX Odoo TrainingDocument25 pagesVdocuments - MX Odoo TrainingDesahan AsmaraNo ratings yet

- IFRS 5 Non-Current Assets Held For Sale and Discontinued OperationsDocument12 pagesIFRS 5 Non-Current Assets Held For Sale and Discontinued Operationsanon_419651076No ratings yet

- Sbi 4 PDFDocument1 pageSbi 4 PDFarjunv_14No ratings yet

- Warehousing & Inventory Control TrainingDocument3 pagesWarehousing & Inventory Control TrainingsukmadewiNo ratings yet

- Form Refund-Transfer Request-V180903Document1 pageForm Refund-Transfer Request-V180903Catarina GitaNo ratings yet

- L03 - Accounting Classification and EquationsDocument29 pagesL03 - Accounting Classification and EquationsmardhiahNo ratings yet

- NBFC Project Report by MS. Sonia JariaDocument34 pagesNBFC Project Report by MS. Sonia JariaSonia SoniNo ratings yet

- Prince Corporation Acquired 100 Percent of Sword CompanyDocument2 pagesPrince Corporation Acquired 100 Percent of Sword CompanyKailash Kumar50% (2)

- ASPIS Cyber Technologies Enters Into Partnership With ICARO™ Media GroupDocument5 pagesASPIS Cyber Technologies Enters Into Partnership With ICARO™ Media GroupPR.comNo ratings yet

- Journal of Transport Geography: SciencedirectDocument11 pagesJournal of Transport Geography: SciencedirectJuan BuitragoNo ratings yet

- 103 Interview Que.Document14 pages103 Interview Que.Shailendra GuptaNo ratings yet

- Ca ResumeDocument2 pagesCa Resumeapi-379518333No ratings yet

- Credit Card I PdsDocument11 pagesCredit Card I PdsIskandar ZulqarnainNo ratings yet

- Shaw AgreementDocument7 pagesShaw AgreementDennis EnnsNo ratings yet