You might also like

- Accounting Standard 1Document27 pagesAccounting Standard 1Sid2875% (4)

- Business Dealings in Emerging Economies, Non-Contractual Relations, and Recourse To Law - An AnalysisDocument12 pagesBusiness Dealings in Emerging Economies, Non-Contractual Relations, and Recourse To Law - An AnalysisAnish GuptaNo ratings yet

- Covid Vaccine: June 2021Document7 pagesCovid Vaccine: June 2021Sharon GabrielNo ratings yet

- Terms of TradeDocument14 pagesTerms of TradeNaman Mishra100% (2)

- Cooperative Credit Institutions PDFDocument96 pagesCooperative Credit Institutions PDFSumit BirlaNo ratings yet

- Job Analysis of BFSI SectorDocument11 pagesJob Analysis of BFSI SectorHarshada ChavanNo ratings yet

- A Study On Working Capital Management of Anantha PVC Private LTDDocument4 pagesA Study On Working Capital Management of Anantha PVC Private LTDEditor IJTSRDNo ratings yet

- Financial Planning and Tax Savings StrategiesDocument16 pagesFinancial Planning and Tax Savings StrategiesShyam KumarNo ratings yet

- GST Project Report AnalysisDocument61 pagesGST Project Report AnalysisFahim FaisalNo ratings yet

- Study of GST Its Applications BHELDocument43 pagesStudy of GST Its Applications BHELBalram ModiNo ratings yet

- Presentaton On Review of LiteratureDocument27 pagesPresentaton On Review of LiteraturearchitNo ratings yet

- Inter-Firm ComparisonDocument5 pagesInter-Firm Comparisonanon_672065362100% (1)

- Risk ManagementDocument35 pagesRisk Managementfafese7300No ratings yet

- Corporate Finance ProjectDocument14 pagesCorporate Finance ProjectAspiring StudentNo ratings yet

- Full Paper PDFDocument10 pagesFull Paper PDFSuhasini DurveNo ratings yet

- Interim Report On CCLDocument9 pagesInterim Report On CCLanitasingh_kumari5No ratings yet

- Project Report - Merger, Amalgamation, TakeoverDocument18 pagesProject Report - Merger, Amalgamation, TakeoverRohan kedia0% (1)

- LPGDocument11 pagesLPGRobinvarshneyNo ratings yet

- Tax Structure in IndiaDocument37 pagesTax Structure in IndiaShiva Kumar BandaruNo ratings yet

- Project of Financial MarketsDocument31 pagesProject of Financial MarketsrahulbbiNo ratings yet

- CAclubindia News - Managerial Remuneration (In A Simple Way) PDFDocument3 pagesCAclubindia News - Managerial Remuneration (In A Simple Way) PDFVivek ReddyNo ratings yet

- IFM M.Com NotesDocument36 pagesIFM M.Com NotesViraja GuruNo ratings yet

- A Summer Internship Project Report ONDocument64 pagesA Summer Internship Project Report ONSachin PacharneNo ratings yet

- RM Units 1 2 NOTES PDFDocument9 pagesRM Units 1 2 NOTES PDFKishore RamNo ratings yet

- Literature ReviewDocument50 pagesLiterature ReviewMohmmedKhayyumNo ratings yet

- 3.2 Components of Working CapitalDocument24 pages3.2 Components of Working CapitalShahid Shaikh100% (1)

- Comparative Ratio Analysis of Britannia Industries and Nestle IndiaDocument46 pagesComparative Ratio Analysis of Britannia Industries and Nestle Indiasafwan100% (4)

- Foreign Institutional InvestmentsDocument61 pagesForeign Institutional Investmentsnitesh01cool100% (7)

- SynopsisDocument3 pagesSynopsisBinuja ShresthaNo ratings yet

- Dissertation On Analytical Study of Foreign Direct Investment in IndiaDocument80 pagesDissertation On Analytical Study of Foreign Direct Investment in Indiaaurorashiva1No ratings yet

- E0071 Financial Analysis of Reliance Industries LimitedDocument87 pagesE0071 Financial Analysis of Reliance Industries LimitedwebstdsnrNo ratings yet

- Procedures To Obtain Export FinanceDocument3 pagesProcedures To Obtain Export FinanceVajju ThoutiNo ratings yet

- PHD Thesis 13Document292 pagesPHD Thesis 13Prince PatelNo ratings yet

- Construction of Optimal Portfolio Using Sharpe ModelDocument79 pagesConstruction of Optimal Portfolio Using Sharpe ModelMohammad hafeezNo ratings yet

- FM - Financial Planning & Forecasting (Cir 29.3Document83 pagesFM - Financial Planning & Forecasting (Cir 29.3pranoyNo ratings yet

- Cost of Capital (AnkushaDocument50 pagesCost of Capital (AnkushaPreet PreetNo ratings yet

- Legal and Procedural Aspects of MergerDocument8 pagesLegal and Procedural Aspects of MergerAnkit Kumar (B.A. LLB 16)No ratings yet

- Forms of Amalgamation AccountingDocument35 pagesForms of Amalgamation AccountingKaran VyasNo ratings yet

- Index Number (MBA)Document6 pagesIndex Number (MBA)Veerendranath NaniNo ratings yet

- Describe The Benefits of Having A Clear Mission and Vision StatementDocument2 pagesDescribe The Benefits of Having A Clear Mission and Vision StatementAlemayehu DemekeNo ratings yet

- Cardinal Utility AnalysisDocument19 pagesCardinal Utility AnalysisShah MominNo ratings yet

- Summer Project Report on Working Capital Management at HALDocument62 pagesSummer Project Report on Working Capital Management at HALManaswini Hotta100% (1)

- Sample Sip Report ADocument46 pagesSample Sip Report AJagrati KanojiyaNo ratings yet

- Trend Analysis of FDI in IndiaDocument66 pagesTrend Analysis of FDI in IndiaRajat Goyal100% (4)

- Project Report: Pune UniversityDocument58 pagesProject Report: Pune UniversityMayur N Malviya100% (1)

- Budgetary Control - IciciDocument8 pagesBudgetary Control - Icicimohammed khayyumNo ratings yet

- Working Capital Management ProjectDocument8 pagesWorking Capital Management ProjectAbhilash GopalNo ratings yet

- Limitations of Accounting PrinciplesDocument2 pagesLimitations of Accounting Principlesnsrmurthy60% (5)

- Working Capital MGTDocument61 pagesWorking Capital MGTDinesh Kumar100% (1)

- Capital Budgeting Analysis at Indian Oil CorporationDocument16 pagesCapital Budgeting Analysis at Indian Oil CorporationBhargavi Dodda100% (1)

- Nitin517 Final Project (NBFC)Document78 pagesNitin517 Final Project (NBFC)Abhishek RanaNo ratings yet

- Summer Internship ProjectDocument37 pagesSummer Internship ProjectSagarNo ratings yet

- Fundamentals and Technical Analysis of Private Bank SectorDocument51 pagesFundamentals and Technical Analysis of Private Bank SectorShirish TawdeNo ratings yet

- Study of Budgeting Process and Budgetary ControlDocument47 pagesStudy of Budgeting Process and Budgetary ControlSahil AggarwalNo ratings yet

- O Lakshmi Prasanna: With Reference ToDocument76 pagesO Lakshmi Prasanna: With Reference ToInthiyaz KothapalleNo ratings yet

- Research Paper On Working CapitalDocument7 pagesResearch Paper On Working CapitalRujuta ShahNo ratings yet

- Financial Performence of KesoramDocument97 pagesFinancial Performence of KesoramBasinepalli Sathish ReddyNo ratings yet

- Gautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaDocument23 pagesGautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaShyam TomerNo ratings yet

- Gautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaDocument36 pagesGautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaShyam TomerNo ratings yet

- Himanshu ProjectDocument55 pagesHimanshu ProjectrajNo ratings yet

- 01 Introduction (Compatibility Mode)Document38 pages01 Introduction (Compatibility Mode)Shyam TomerNo ratings yet

- Tabel Z NegatifDocument1 pageTabel Z NegatifDavid Tobing100% (2)

- 8 Pe, VC, AfDocument15 pages8 Pe, VC, AfShyam TomerNo ratings yet

- Vacation Leave 15march14 PDFDocument2 pagesVacation Leave 15march14 PDFShyam TomerNo ratings yet

- ABC Analysis Guide for Inventory ManagementDocument123 pagesABC Analysis Guide for Inventory ManagementManish SinghNo ratings yet

- Operations PapersDocument11 pagesOperations PapersShyam TomerNo ratings yet

- Supply Chain ManagementDocument13 pagesSupply Chain ManagementShyam TomerNo ratings yet

- 1 Financial - Services - IntroductionDocument38 pages1 Financial - Services - IntroductionShyam TomerNo ratings yet

- ShyamDocument38 pagesShyamShyam TomerNo ratings yet

- Supply Chain Management: By: Sweta (16/IMB/034) Shyamveer (16/IMB/) Rohit Gupta (16/IMB/) Aman Singh (15/IMB/010)Document18 pagesSupply Chain Management: By: Sweta (16/IMB/034) Shyamveer (16/IMB/) Rohit Gupta (16/IMB/) Aman Singh (15/IMB/010)Shyam TomerNo ratings yet

- IFMDocument46 pagesIFMIvaturiAnithaNo ratings yet

- Gautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaDocument36 pagesGautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaShyam TomerNo ratings yet

- Supply Chain ManagementDocument13 pagesSupply Chain ManagementShyam TomerNo ratings yet

- Gautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaDocument36 pagesGautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaShyam TomerNo ratings yet

- Summer Internship Guidelines 2019-20Document10 pagesSummer Internship Guidelines 2019-20Shyam TomerNo ratings yet

- Supply Chain ManagementDocument13 pagesSupply Chain ManagementShyam TomerNo ratings yet

- Gautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaDocument23 pagesGautam Buddha University: Submitted in The Partial Fulfillment of Integrated MbaShyam TomerNo ratings yet

- General Guide On Service Tax 20211011Document47 pagesGeneral Guide On Service Tax 20211011bearteddy17193No ratings yet

- Adobe Scan FebDocument1 pageAdobe Scan FebpranayjadhavNo ratings yet

- Ticket Ddu To Delhi 10 JanDocument2 pagesTicket Ddu To Delhi 10 Janvishal yadavNo ratings yet

- Fixedline and broadband bill detailsDocument2 pagesFixedline and broadband bill detailsJawedNo ratings yet

- Invoice2022 2023 07307 001Document2 pagesInvoice2022 2023 07307 001bapi sahuNo ratings yet

- NR7413407451445605Document2 pagesNR7413407451445605gajetushanayaNo ratings yet

- Proforma Invoice THARDocument1 pageProforma Invoice THARSimran DhamoonNo ratings yet

- InvoiceDocument1 pageInvoiceतुमचा हितचिंतकNo ratings yet

- CARO TenderDocument100 pagesCARO Tenderpwdcd1No ratings yet

- DR Vikas PpkiyDocument1 pageDR Vikas PpkiylxshNo ratings yet

- CB5E45903BDocument1 pageCB5E45903Bkrish tcrNo ratings yet

- Print Invoice DetailsDocument1 pagePrint Invoice Detailskrishna kanthNo ratings yet

- Challan 32Document1 pageChallan 32Aditya Kumar KaushikNo ratings yet

- Airtel Bill March'23Document14 pagesAirtel Bill March'23kartik kathuriaNo ratings yet

- Autozone InvoiceDocument2 pagesAutozone InvoicePrasanth C Nandhakumar100% (1)

- Cr. Note No. RJSSC 14322Document1 pageCr. Note No. RJSSC 14322amarjot chhabraNo ratings yet

- Chapter 27 Sales Interstate Exempted EntryDocument3 pagesChapter 27 Sales Interstate Exempted EntryTEJA SINGHNo ratings yet

- OFI GST O2C Tax Defaultation Functional DocumentDocument59 pagesOFI GST O2C Tax Defaultation Functional DocumentdurairajNo ratings yet

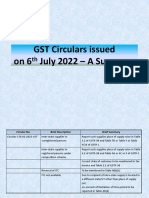

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- Economic Reforms Lpg-Question BankDocument6 pagesEconomic Reforms Lpg-Question BankHari prakarsh NimiNo ratings yet

- Law BCR MTP Questions NovemberDocument6 pagesLaw BCR MTP Questions NovemberTechnical GuruNo ratings yet

- 8080923891/Notes/SYJC COM Practical Solution - 03 - 09 - 2023 - 09 - 18 - 03Document22 pages8080923891/Notes/SYJC COM Practical Solution - 03 - 09 - 2023 - 09 - 18 - 03Rhea JainNo ratings yet

- 24 - 38221544103291 SCR GuntupalliDocument3 pages24 - 38221544103291 SCR GuntupalliAbhishek DahiyaNo ratings yet

- Tax Invoice for realme Buds Q purchaseDocument1 pageTax Invoice for realme Buds Q purchaserupeshNo ratings yet

- 5th March 2022 Current Affairs by Kapil Kathpal (Bilingual)Document55 pages5th March 2022 Current Affairs by Kapil Kathpal (Bilingual)Sailesh AgrawalNo ratings yet

- GST Invoice for MuleSoft TrainingDocument6 pagesGST Invoice for MuleSoft TrainingSrinivasa HelavarNo ratings yet

- GST Bill Format in ExcelDocument184 pagesGST Bill Format in Excelkrishna chaitanyaNo ratings yet

- Report On IMPACT OF GST ON REAL ESTATE INDUSTRYDocument31 pagesReport On IMPACT OF GST ON REAL ESTATE INDUSTRYsamNo ratings yet

- PDF CropDocument4 pagesPDF Crop04vijilNo ratings yet

- Approach Note For Adhering To GST in SAP Environment: © 2016 IBM CorporationDocument7 pagesApproach Note For Adhering To GST in SAP Environment: © 2016 IBM CorporationKashishNo ratings yet