You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

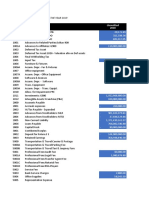

- Unaudited Trial Balance For The Year 2019: Sultan 900 Capital, IncDocument18 pagesUnaudited Trial Balance For The Year 2019: Sultan 900 Capital, IncGlennizze GalvezNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Accountancy Student: Froilan Arlando BandulaDocument5 pagesAccountancy Student: Froilan Arlando BandulaGlennizze GalvezNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- HsyshDocument1 pageHsyshGlennizze GalvezNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Entrep 4 Week: What I KnowDocument9 pagesEntrep 4 Week: What I KnowGlennizze GalvezNo ratings yet

- Assets: Balance Sheet As of September 31, 2020Document91 pagesAssets: Balance Sheet As of September 31, 2020Glennizze GalvezNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Chapter 14 - Bus Com Part 1 - Afar Part 2-1Document4 pagesChapter 14 - Bus Com Part 1 - Afar Part 2-1Glennizze GalvezNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Mathematics in Modern World Lecture InsightsDocument2 pagesMathematics in Modern World Lecture InsightsGlennizze GalvezNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- January 2018 - December 2018Document12 pagesJanuary 2018 - December 2018Jussa Leilady AlberbaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Senior High School Department Proposed Tax Amnesty ProgramDocument1 pageSenior High School Department Proposed Tax Amnesty ProgramGlenn GalvezNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- PurposiveDocument1 pagePurposiveGlennizze GalvezNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Financialaccounting 3 Theories Summary ValixDocument10 pagesFinancialaccounting 3 Theories Summary ValixDarwin Competente LagranNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Maxims of CommunicationDocument1 pageMaxims of CommunicationGlennizze GalvezNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Maxims of CommunicationDocument1 pageMaxims of CommunicationGlennizze GalvezNo ratings yet

- Body Composition: BenefitsDocument8 pagesBody Composition: BenefitsGlennizze GalvezNo ratings yet

- Cpa Review Questions - Batch 7Document44 pagesCpa Review Questions - Batch 7MJ YaconNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- January 2019: Sun Mon Tue Wed Thu Fri SatDocument12 pagesJanuary 2019: Sun Mon Tue Wed Thu Fri SatGlennizze GalvezNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- TestbankDocument93 pagesTestbankMack Ray O. Paredes100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Chapter 16 - Bus Com Part 3 - Afar Part 2-1Document5 pagesChapter 16 - Bus Com Part 3 - Afar Part 2-1Glennizze GalvezNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Accountants National Capital Region (NFJPIA-NCR) Is A Duly: Ngarap Tungo SA Kilang LaDocument4 pagesAccountants National Capital Region (NFJPIA-NCR) Is A Duly: Ngarap Tungo SA Kilang LaGlennizze GalvezNo ratings yet

- 3.2.9 Process FlowchartDocument4 pages3.2.9 Process FlowchartGlennizze GalvezNo ratings yet

- Accountancy Student: Froilan Arlando BandulaDocument5 pagesAccountancy Student: Froilan Arlando BandulaGlennizze GalvezNo ratings yet

- Systems Analysis and Design 2014 Course OverviewDocument3 pagesSystems Analysis and Design 2014 Course OverviewGlennizze GalvezNo ratings yet

- Determining the Feasibility of Manufacturing and Marketing LaingDocument65 pagesDetermining the Feasibility of Manufacturing and Marketing LaingGlennizze Galvez100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Analytic-Geometry:: You Should Be Using A RulerDocument8 pagesAnalytic-Geometry:: You Should Be Using A RulerGlennizze GalvezNo ratings yet

- 3.1.4-3.1.5 Marketing PlanDocument4 pages3.1.4-3.1.5 Marketing PlanGlennizze GalvezNo ratings yet

- Umar SulemanDocument7 pagesUmar SulemanUmar SulemanNo ratings yet

- Perpetual Dalta Fun Booth U-Week 2018Document2 pagesPerpetual Dalta Fun Booth U-Week 2018Glennizze GalvezNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Senior High School Department Proposed Tax Amnesty ProgramDocument1 pageSenior High School Department Proposed Tax Amnesty ProgramGlenn GalvezNo ratings yet

- Whole UniverseDocument2 pagesWhole UniverseGlenn GalvezNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)