You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Solutions To End of Chapter ProblemsDocument176 pagesSolutions To End of Chapter Problemsmitaleo23100% (1)

- CH 09 RevisedDocument36 pagesCH 09 RevisedNiharikaChouhanNo ratings yet

- NATWESTDocument25 pagesNATWESTfaguobaozhuangfa2No ratings yet

- PD PDFDocument482 pagesPD PDFCopycatNo ratings yet

- Final Exam Afar 3 2022Document10 pagesFinal Exam Afar 3 2022Cassie HowardNo ratings yet

- Rodel M. Sescon, MM: InstructorDocument23 pagesRodel M. Sescon, MM: InstructorR.v.EscoroNo ratings yet

- ACCA BPP - FR - Final Mock - Qs MAC 24Document18 pagesACCA BPP - FR - Final Mock - Qs MAC 24Iqmal khushairiNo ratings yet

- Chapter 1 Introduction To Cost AccountingDocument42 pagesChapter 1 Introduction To Cost AccountingPotato FriesNo ratings yet

- Pgsus 31122020 enDocument96 pagesPgsus 31122020 enÇağhan EraymanNo ratings yet

- Bibliography AppendixDocument5 pagesBibliography AppendixSocialist GopalNo ratings yet

- Millat Tractors... (Inventories)Document11 pagesMillat Tractors... (Inventories)juni650% (2)

- A Study On Investors Preference Towards Mutual Funds. Shows What Type of Investment People Prefer 1 1Document82 pagesA Study On Investors Preference Towards Mutual Funds. Shows What Type of Investment People Prefer 1 1shariffNo ratings yet

- Chapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document26 pagesChapter 22 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din Sheryar100% (1)

- This Study Resource Was: Financial Management Part 2 Handouts Analysis and Interpretation of Financial StatementsDocument6 pagesThis Study Resource Was: Financial Management Part 2 Handouts Analysis and Interpretation of Financial StatementsRengeline LucasNo ratings yet

- Chapter 23Document22 pagesChapter 23hippop kNo ratings yet

- Maria HernandezDocument8 pagesMaria HernandezAimane BeggarNo ratings yet

- Written WorkDocument3 pagesWritten WorkKenjie SobrevegaNo ratings yet

- San Lam Stratus FundsDocument2 pagesSan Lam Stratus FundsTiso Blackstar GroupNo ratings yet

- ACC Group Assignment 1Document13 pagesACC Group Assignment 1aregahegn bisetNo ratings yet

- ENTREPRENEURSHIP 7Ps MELC3Document18 pagesENTREPRENEURSHIP 7Ps MELC3Hazel De VeraNo ratings yet

- Overview of Heads of income-MTS-2022Document197 pagesOverview of Heads of income-MTS-2022GauravNo ratings yet

- Dividend Policy DecisionDocument37 pagesDividend Policy DecisionGaurav KumarNo ratings yet

- Comparison Between Ulips and Traditional PlanDocument4 pagesComparison Between Ulips and Traditional Planpayal_31No ratings yet

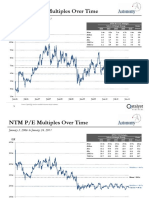

- NTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011Document3 pagesNTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011mittleNo ratings yet

- Fiscal Year Is January-December. All Values USD Millions.: AssetsDocument29 pagesFiscal Year Is January-December. All Values USD Millions.: AssetsHubert Luis Madariaga ManyaNo ratings yet

- Offering Circular 25 January 2008 - Liberty ACQDocument157 pagesOffering Circular 25 January 2008 - Liberty ACQGag PafNo ratings yet

- ET Wealth Apr 6 - 12 2020Document23 pagesET Wealth Apr 6 - 12 2020Rony GeorgeNo ratings yet

- Retirement of Partner, Treatment of GoodwillDocument6 pagesRetirement of Partner, Treatment of GoodwillBoobalan RNo ratings yet

- Agreement For Software MembershipDocument2 pagesAgreement For Software MembershipAnujit NandyNo ratings yet

- Accounting Exercise Chap 13Document10 pagesAccounting Exercise Chap 13Zi Yan HoonNo ratings yet