You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Quiz 1 - Intermediate AccountingDocument2 pagesQuiz 1 - Intermediate AccountingMary GlaineNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Company Valuation Based On Ev/ebitda and Ev/ebit Multiples: A Case Study of A Brazilian Mining CompanyDocument55 pagesCompany Valuation Based On Ev/ebitda and Ev/ebit Multiples: A Case Study of A Brazilian Mining CompanyRicardo AlvesNo ratings yet

- How To Cashout PaypalDocument2 pagesHow To Cashout PaypalLoubango MikeNo ratings yet

- Sun Maxilink PrimeDocument9 pagesSun Maxilink PrimeGracie Sugatan PlacinoNo ratings yet

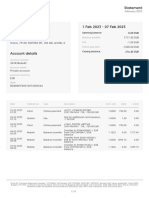

- Icard Statement 01.2023Document1 pageIcard Statement 01.2023anastasiya DubininaNo ratings yet

- DOA GPI 20millionDocument18 pagesDOA GPI 20millionMinh KentNo ratings yet

- (06 Hours) : Concepts of Investment - Financial and Non - Financial Forms of InvestmentDocument15 pages(06 Hours) : Concepts of Investment - Financial and Non - Financial Forms of InvestmentBrahmanand ShetNo ratings yet

- SalaryDocument2 pagesSalaryFLEICH ANNE PASCUANo ratings yet

- Tally Exercise 1 PDFDocument1 pageTally Exercise 1 PDFkumarbcomcaNo ratings yet

- Green Shoe OptionDocument15 pagesGreen Shoe OptionNadeem Ahmad100% (1)

- Challenges For Public Sector Banks in IndiaDocument63 pagesChallenges For Public Sector Banks in IndiaKahkashan Anjum100% (8)

- AccountStatement 1Document3 pagesAccountStatement 1Muhammad WaseemNo ratings yet

- Wealth Plan Worksheet RTQDocument10 pagesWealth Plan Worksheet RTQBùi Duy TùngNo ratings yet

- R NPV IRR 0% 5.000 15.24% 5% 2.988 10% 1.372 15% 0.056 20% - 1.028 25% - 1.932 30% - 2.693Document1 pageR NPV IRR 0% 5.000 15.24% 5% 2.988 10% 1.372 15% 0.056 20% - 1.028 25% - 1.932 30% - 2.693mattNo ratings yet

- Case Study TRXDocument5 pagesCase Study TRXapi-673819921No ratings yet

- Notes On Cash and Cash EquivalentsDocument5 pagesNotes On Cash and Cash EquivalentsLeonoramarie BernosNo ratings yet

- LM01 Rates and ReturnsDocument102 pagesLM01 Rates and ReturnsYuri BNo ratings yet

- Dlsu Exam 2nd Quiz Acccob2Document4 pagesDlsu Exam 2nd Quiz Acccob2Chelcy Mari GugolNo ratings yet

- Chap 017 AccDocument47 pagesChap 017 Acckaren_park1No ratings yet

- Financial Performance Analysis of Jamuna Bank Term Paper Group5 Sec CDocument29 pagesFinancial Performance Analysis of Jamuna Bank Term Paper Group5 Sec CShiraj-Us-Salahin IslamNo ratings yet

- Presentation On Capital MarketDocument20 pagesPresentation On Capital MarketYugesh PrajapatiNo ratings yet

- Assessment Eco211Document15 pagesAssessment Eco211Nur IkaNo ratings yet

- Banna Leisure 111Document2 pagesBanna Leisure 111ravinyseNo ratings yet

- Market IntegrationDocument11 pagesMarket IntegrationDianne Mae LlantoNo ratings yet

- Role and Functions of Nepal Rastra BankDocument15 pagesRole and Functions of Nepal Rastra Banksunil karkiNo ratings yet

- Chapter ThreeDocument20 pagesChapter ThreeWegene Benti UmaNo ratings yet

- Taxation Auditing Problems: (Monday) (Wednesday)Document2 pagesTaxation Auditing Problems: (Monday) (Wednesday)Carmen TabundaNo ratings yet

- AssignmentsWk8 2Document3 pagesAssignmentsWk8 2simamo4203No ratings yet

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadNo ratings yet

- The Cost of Capital Lecture (Revised)Document50 pagesThe Cost of Capital Lecture (Revised)Ranin, Manilac Melissa S50% (4)