You might also like

- Optimisation and DecisionDocument17 pagesOptimisation and DecisionMnawer Hadid100% (1)

- Start A Disposable Syringes Manufacturing Business PDFDocument7 pagesStart A Disposable Syringes Manufacturing Business PDFIndia Heals-2020100% (2)

- Qualitrol STB000 Smart Transformer BreatherDocument42 pagesQualitrol STB000 Smart Transformer BreatherLuis SánchezNo ratings yet

- Surviving the Spare Parts Crisis: Maintenance Storeroom and Inventory ControlFrom EverandSurviving the Spare Parts Crisis: Maintenance Storeroom and Inventory ControlNo ratings yet

- Acid SlurryDocument8 pagesAcid SlurryVinod GoelNo ratings yet

- Surgical Bandage PDFDocument5 pagesSurgical Bandage PDFJoe SparrowNo ratings yet

- Western Home Elevator Design Guide 2011 PDFDocument21 pagesWestern Home Elevator Design Guide 2011 PDFTuấn NamNo ratings yet

- Requirement of Bitumen (VG & PMB)Document5 pagesRequirement of Bitumen (VG & PMB)Veeresh SharmaNo ratings yet

- Medical Titanium Bellows - Tailored To Your NeedsDocument8 pagesMedical Titanium Bellows - Tailored To Your NeedssourabhNo ratings yet

- P P O I : Roject Rofile N NvertersDocument11 pagesP P O I : Roject Rofile N NvertersAshwani RanaNo ratings yet

- Chaff CutterDocument23 pagesChaff CutterFekadie TesfaNo ratings yet

- Plastic CratesDocument9 pagesPlastic CratesfawwazNo ratings yet

- Roll CrusherDocument7 pagesRoll CrusherSudarshan Devarapalli100% (1)

- Metals and Engineering Corporation: Feasibility Study ONDocument15 pagesMetals and Engineering Corporation: Feasibility Study ONkinfegetaNo ratings yet

- Self Tapping ScrewDocument12 pagesSelf Tapping Screwsanjay_lingotNo ratings yet

- Crockmeter (Rubbing Tester) : To Determine The Colour Fastness of Textiles To Dry or Wet Crocking or RubbingDocument2 pagesCrockmeter (Rubbing Tester) : To Determine The Colour Fastness of Textiles To Dry or Wet Crocking or RubbingDebashishDolonNo ratings yet

- Ajustable Hospital Beds PsDocument11 pagesAjustable Hospital Beds PsManish PoddarNo ratings yet

- Pilfer Proof Caps - Project ReportDocument10 pagesPilfer Proof Caps - Project Reportbaddy2inNo ratings yet

- Tutorial QuestionsDocument7 pagesTutorial Questionsrobinkaby06No ratings yet

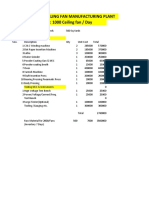

- Plant CostingDocument1 pagePlant CostingNeeraj KatariaNo ratings yet

- Surgical Absorbent CottonDocument11 pagesSurgical Absorbent CottonharyroyNo ratings yet

- 2019 Bhilai Tender - TND - 074802 - 152879Document32 pages2019 Bhilai Tender - TND - 074802 - 152879Bhavya Makhania100% (1)

- current transformer, potential transformer, metering cubicle, combined ctpt unit, metering unit, LT CT, indoor resin cast CT, indoor resin cast PT, resin cast current transformer, resin cast potential transformerDocument3 pagescurrent transformer, potential transformer, metering cubicle, combined ctpt unit, metering unit, LT CT, indoor resin cast CT, indoor resin cast PT, resin cast current transformer, resin cast potential transformerSharafatNo ratings yet

- Solapur MOCB Statistics - 18-02-2014Document16 pagesSolapur MOCB Statistics - 18-02-2014Pushpak AkhadeNo ratings yet

- Lecture 1Document6 pagesLecture 1محمد احمدNo ratings yet

- Premiere Industries - AbstractDocument23 pagesPremiere Industries - AbstractBOUDOUNIT YounesNo ratings yet

- Business Opportunity - Thru Tubing ToolsDocument24 pagesBusiness Opportunity - Thru Tubing ToolsSohaib RashidNo ratings yet

- Tinplate CompanyDocument32 pagesTinplate CompanysnbtccaNo ratings yet

- Schedule-J - List of Maintenance Tools and TacklesDocument6 pagesSchedule-J - List of Maintenance Tools and TacklesPrasanna kumar subudhiNo ratings yet

- Andrew ChaseDocument4 pagesAndrew Chasevipereejay100% (2)

- Cluster Profile Howrah Foundry Industries: West BengalDocument16 pagesCluster Profile Howrah Foundry Industries: West BengalSonal PatelNo ratings yet

- P P O I : Roject Rofile N NvertersDocument11 pagesP P O I : Roject Rofile N NvertersramaNo ratings yet

- Project Report On CottonDocument8 pagesProject Report On CottonManu ChawlaNo ratings yet

- Absorbent CottonDocument27 pagesAbsorbent CottonTrầnChíTrungNo ratings yet

- Chaff CutterDocument23 pagesChaff Cutterabel_kayel100% (2)

- Or Tutorial 1 - LPP FormulationsDocument8 pagesOr Tutorial 1 - LPP FormulationsKrunal PitrodaNo ratings yet

- BTL-5000 Series: User'S ManualDocument65 pagesBTL-5000 Series: User'S ManualAlexaNo ratings yet

- Bleaching PowderDocument3 pagesBleaching PowderVikram ChoodaiahNo ratings yet

- Internship Report of ISHAN EQUIPMENTS LTDDocument38 pagesInternship Report of ISHAN EQUIPMENTS LTDTapanNo ratings yet

- Biopure Market Potential Exercise Suggested SolutionDocument4 pagesBiopure Market Potential Exercise Suggested Solutionargand_xw9097No ratings yet

- Distribution TransformerDocument16 pagesDistribution TransformerPurit RawalNo ratings yet

- Foodpharma AtritorDocument6 pagesFoodpharma AtritorAntonNo ratings yet

- Aspects of Productivity in Cotton Spinning PDFDocument4 pagesAspects of Productivity in Cotton Spinning PDFlalit kashyapNo ratings yet

- Cerafil App ManualDocument27 pagesCerafil App Manualcbernal73No ratings yet

- Tech Spec of Grinding Ball Based On CC OS SpecDocument17 pagesTech Spec of Grinding Ball Based On CC OS SpecAmitava PalNo ratings yet

- Air Bubble PackingDocument9 pagesAir Bubble PackingSneha Sagar SharmaNo ratings yet

- Medical Mo QuoteDocument5 pagesMedical Mo QuoteSam PattnaikNo ratings yet

- Business Opportunity - Thru Tubing ToolsDocument24 pagesBusiness Opportunity - Thru Tubing ToolsSohaib RashidNo ratings yet

- CATL 34189-20AH Low Temperature Cell SpecificationDocument17 pagesCATL 34189-20AH Low Temperature Cell Specificationxueziying741No ratings yet

- Oxygen PlantDocument9 pagesOxygen PlantVivek PrajapatiNo ratings yet

- IP ProblemsDocument8 pagesIP ProblemsShrinidhi HariharasuthanNo ratings yet

- Supply Chain Strategies - Session IiiDocument23 pagesSupply Chain Strategies - Session IiiSharad SharmaNo ratings yet

- Tutorial Sheet 1Document3 pagesTutorial Sheet 1ANMOL50% (2)

- Steel: The Indian Steel IndustryDocument20 pagesSteel: The Indian Steel IndustrySylvia GraceNo ratings yet

- (SO) 02 (24-25) Science & Surgical (Ligasure Trolley)Document1 page(SO) 02 (24-25) Science & Surgical (Ligasure Trolley)kayamhossain94No ratings yet

- Andrew Carter Case StudyDocument8 pagesAndrew Carter Case StudyLouie Mar SabadoNo ratings yet

- Jwala Techno Engineering Pvt. LTD.: Turnkey Plants & Machinery For Processing Fruits & VegetablesDocument7 pagesJwala Techno Engineering Pvt. LTD.: Turnkey Plants & Machinery For Processing Fruits & VegetablesDnyaneshwar Dattatraya PhadatareNo ratings yet

- PlasticbottleDocument9 pagesPlasticbottleAzhar Abdul RazakNo ratings yet

- CTL 3000 Rev 3 PDFDocument16 pagesCTL 3000 Rev 3 PDFdiego martinezNo ratings yet

- Adiabatic Fixed-Bed Reactors: Practical Guides in Chemical EngineeringFrom EverandAdiabatic Fixed-Bed Reactors: Practical Guides in Chemical EngineeringNo ratings yet

- Mechanical Properties and Performance of Engineering Ceramics and Composites X: A Collection of Papers Presented at the 39th International Conference on Advanced Ceramics and CompositesFrom EverandMechanical Properties and Performance of Engineering Ceramics and Composites X: A Collection of Papers Presented at the 39th International Conference on Advanced Ceramics and CompositesDileep SinghNo ratings yet

- Atrix HD LGDocument28 pagesAtrix HD LGJachal VisionNo ratings yet

- 14.ergonomic Workstation Design For Science Laboratory (Norhafizah Rosman) PP 93-102Document10 pages14.ergonomic Workstation Design For Science Laboratory (Norhafizah Rosman) PP 93-102upenapahangNo ratings yet

- Research Paper Humss 201 Chapter 1 and 2Document39 pagesResearch Paper Humss 201 Chapter 1 and 2Mariel Dulin ArcegaNo ratings yet

- HITACHI RAC Brochure Generic 08Document33 pagesHITACHI RAC Brochure Generic 08Charalampos KovrasNo ratings yet

- Schuller History PowerpointDocument24 pagesSchuller History PowerpointKarel RespatiNo ratings yet

- Catalog BB Type HDocument2 pagesCatalog BB Type HdioalfanandaNo ratings yet

- Essc-Pwg Report Agusan Marsh Development Alliance Agusan Del Sur1Document9 pagesEssc-Pwg Report Agusan Marsh Development Alliance Agusan Del Sur1Princess VistalNo ratings yet

- PRDS Valve: Different Options For UseDocument3 pagesPRDS Valve: Different Options For UseRahul GawaliNo ratings yet

- Semistructured Key Informant Interview (KII) GuideDocument10 pagesSemistructured Key Informant Interview (KII) GuideEdy Syahputra HarahapNo ratings yet

- Assessment Nursing Diagnosis Planning Intervention Rationale EvaluationDocument2 pagesAssessment Nursing Diagnosis Planning Intervention Rationale EvaluationJulliza Joy PandiNo ratings yet

- CSR Policy of Linde India523 - 131268Document5 pagesCSR Policy of Linde India523 - 131268Bhomik J ShahNo ratings yet

- Information Brochure 2023Document5 pagesInformation Brochure 2023sunny KumarNo ratings yet

- Symptom Management Obstruksi BowelDocument5 pagesSymptom Management Obstruksi BowelPutri Mega PetasiNo ratings yet

- Defects in PaintDocument6 pagesDefects in Paintsonu024100% (1)

- Primary Water SystemDocument15 pagesPrimary Water SystemSantoshkumar GuptaNo ratings yet

- Potentiality of Coir Coconut Husk and Sodium Bicarbonate Baking Soda As Compost Catalyst To Reduce Waste Among Filipino HouseholdsDocument38 pagesPotentiality of Coir Coconut Husk and Sodium Bicarbonate Baking Soda As Compost Catalyst To Reduce Waste Among Filipino HouseholdsHANNAH MARIE VINOYANo ratings yet

- Blow Moulding: Assignment 2 (Ms Ii)Document12 pagesBlow Moulding: Assignment 2 (Ms Ii)Nikhil SinghNo ratings yet

- DS0960205-0303860 Adapter Cable Camera BNC - 4pF A01Document2 pagesDS0960205-0303860 Adapter Cable Camera BNC - 4pF A01Игорь ИвановNo ratings yet

- Q2 Cookery 10 WK 1 8Document54 pagesQ2 Cookery 10 WK 1 8Maxine Eunice RocheNo ratings yet

- Timothy Johnson DocumentDocument1 pageTimothy Johnson Document13WMAZNo ratings yet

- EagleBurgmann EA560 enDocument3 pagesEagleBurgmann EA560 enDenim BeširovićNo ratings yet

- TG IflashDocument4 pagesTG IflashNIGHT tubeNo ratings yet

- PV Specificna Velicina Za PA6 Plastiku - QUADRANT-Products - Applications - GuideDocument44 pagesPV Specificna Velicina Za PA6 Plastiku - QUADRANT-Products - Applications - Guide022freeNo ratings yet

- Introduction To Conditional Probability and Bayes Theorem For Data Science ProfessionalsDocument12 pagesIntroduction To Conditional Probability and Bayes Theorem For Data Science ProfessionalsNicholas Pindar DibalNo ratings yet

- Design and Implementation of Acoustic Frequency Deterrent For Lonchura AtricapillaDocument6 pagesDesign and Implementation of Acoustic Frequency Deterrent For Lonchura AtricapillaChris DarayNo ratings yet

- It Report Table of ContentsDocument6 pagesIt Report Table of ContentsMatthewNo ratings yet

- Guía Clínica HTA 2011Document310 pagesGuía Clínica HTA 2011marcelagarciavNo ratings yet

- FSW-Tech Handbook For Specialists and Engineers - enDocument172 pagesFSW-Tech Handbook For Specialists and Engineers - enkamal touilebNo ratings yet