You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Fourth Biden Bank Records MemoDocument12 pagesFourth Biden Bank Records MemoJames Lynch100% (1)

- Managing Your Minister's Housing AllowanceDocument4 pagesManaging Your Minister's Housing AllowanceBelinda Whitfield100% (7)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MERS Procedures Rel 23 FinalDocument220 pagesMERS Procedures Rel 23 FinalrapiddocsNo ratings yet

- Murray Math Line DescriptionDocument48 pagesMurray Math Line DescriptionTUTORIAL BAYNo ratings yet

- For Construction: Document TitleDocument46 pagesFor Construction: Document TitleYousefi76100% (1)

- PR 1718 999 QM 0017 2 Non Conformity ProcedureDocument13 pagesPR 1718 999 QM 0017 2 Non Conformity ProcedureYousefi760% (1)

- Auditing and AssuranceDocument509 pagesAuditing and AssuranceSrinivasa Rao Bandlamudi80% (10)

- Presentation To The Danish Society For Construction and Consulting LawDocument48 pagesPresentation To The Danish Society For Construction and Consulting LawManish Gupta100% (4)

- Merscorp, Inc.: Rules of MembershipDocument48 pagesMerscorp, Inc.: Rules of MembershipDinSFLANo ratings yet

- Asiatic Petroleum VDocument1 pageAsiatic Petroleum VChrisel Joy Casuga SorianoNo ratings yet

- Gas Industry Standard: GIS/F12:2007Document21 pagesGas Industry Standard: GIS/F12:2007Yousefi76No ratings yet

- Corrosion and Galvanic Corrosion of Die Casted Magnesium AlloysDocument6 pagesCorrosion and Galvanic Corrosion of Die Casted Magnesium AlloysYousefi76No ratings yet

- Stray CurrentDocument21 pagesStray CurrentYousefi76No ratings yet

- April 2021 PAYSLIPDocument1 pageApril 2021 PAYSLIPPuja ParekhNo ratings yet

- India and The BASEL-III Reforms Efinitions Basel III:: HQLA (High Quality Liquid Assets)Document5 pagesIndia and The BASEL-III Reforms Efinitions Basel III:: HQLA (High Quality Liquid Assets)Mayank LabhNo ratings yet

- Tuntay'sDocument3 pagesTuntay'sLA AlmznNo ratings yet

- Main Body LicDocument57 pagesMain Body LicRohit RoyNo ratings yet

- InvoiceDocument1 pageInvoiceKunaSudharshanNo ratings yet

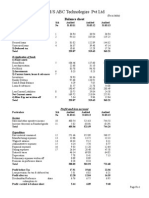

- Balance Sheet of M/S ABC Technologies PVT LTDDocument3 pagesBalance Sheet of M/S ABC Technologies PVT LTDSmitha RajNo ratings yet

- Financial MarketDocument10 pagesFinancial MarketLinganagouda PatilNo ratings yet

- Assets & Liabilites Statement - BorrowerDocument2 pagesAssets & Liabilites Statement - BorrowerAzril JinumboNo ratings yet

- Taxes: Corporate: Sec. S OcDocument2 pagesTaxes: Corporate: Sec. S OcAnonymous JqimV1ENo ratings yet

- Professional MARCH... JULY 2020 #IfrsiseasyDocument172 pagesProfessional MARCH... JULY 2020 #IfrsiseasyJason Baba KwagheNo ratings yet

- Glorvina Constant Plea AgreementDocument12 pagesGlorvina Constant Plea AgreementmtuccittoNo ratings yet

- Bank Ayudhya - Best Practice Panggilan RUPSDocument53 pagesBank Ayudhya - Best Practice Panggilan RUPSAni Nalitayui LifityaNo ratings yet

- Adhar Address Update - Document-List - SSUPDocument1 pageAdhar Address Update - Document-List - SSUPDhanraj PatilNo ratings yet

- History of The Oxford Club - The Oxford ClubDocument9 pagesHistory of The Oxford Club - The Oxford ClubGabriel MouraNo ratings yet

- DP 28434Document235 pagesDP 28434Ankitha KavyaNo ratings yet

- Standard Oil CoDocument2 pagesStandard Oil CoLady MAy SabanalNo ratings yet

- Presentation 1Document15 pagesPresentation 1vanita kunnoNo ratings yet

- More Chapter 5 Exercises TVMDocument11 pagesMore Chapter 5 Exercises TVMaprilNo ratings yet

- 0452 s02 ErDocument9 pages0452 s02 ErAhmed SherifNo ratings yet

- RENT AGREEMENT FormatDocument2 pagesRENT AGREEMENT Formatkaushal sharmaNo ratings yet

- TrushDocument101 pagesTrushtrushna19No ratings yet

- VP Development CEO CFO in San Diego CA Resume Stephen YatskoDocument2 pagesVP Development CEO CFO in San Diego CA Resume Stephen YatskoStephenYatskoNo ratings yet