You might also like

- Accounts Receivable QuizzerDocument4 pagesAccounts Receivable Quizzerknorrpampapakang67% (3)

- Cpa Review School of The Philippines Manila Financial Accounting and Reforting Theory Valix Siy Valix Escala Revised Conceptual FrameworkDocument43 pagesCpa Review School of The Philippines Manila Financial Accounting and Reforting Theory Valix Siy Valix Escala Revised Conceptual FrameworkRichard BorjaNo ratings yet

- Examination About Investment 7Document3 pagesExamination About Investment 7BLACKPINKLisaRoseJisooJennieNo ratings yet

- Problem 1Document3 pagesProblem 1Zyrah Manalo50% (2)

- Bad Debts Accounting ARDocument5 pagesBad Debts Accounting ARhoneyjoy salapantanNo ratings yet

- 13 Acctg Ed 1 - Loan ReceivableDocument17 pages13 Acctg Ed 1 - Loan ReceivableNath BongalonNo ratings yet

- PAS 36 Concept MapDocument1 pagePAS 36 Concept MapMicah RamaykaNo ratings yet

- Cash AssignmentDocument2 pagesCash AssignmentRocelyn OrdoñezNo ratings yet

- Fin 1 Valix Chap 6Document24 pagesFin 1 Valix Chap 6Christian SampagaNo ratings yet

- Loans and Receivables - Long TermDocument3 pagesLoans and Receivables - Long TermAleezaAngelaSanchezNarvadezNo ratings yet

- Chapter 16Document12 pagesChapter 16WesNo ratings yet

- Loans and Receivables Sample Problems 2Document2 pagesLoans and Receivables Sample Problems 2Bryce Bihag60% (5)

- Lecture Notes On Receivable FinancingDocument5 pagesLecture Notes On Receivable Financingjudel ArielNo ratings yet

- Assessment Task 1-1Document10 pagesAssessment Task 1-1hahahahaNo ratings yet

- Investment in Equity Securities 2Document2 pagesInvestment in Equity Securities 2miss independentNo ratings yet

- Actg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizDocument4 pagesActg 431 Quiz Week 7 Practical Accounting I (Part II) Inventories QuizMarilou Arcillas PanisalesNo ratings yet

- P1 Day4 RMDocument15 pagesP1 Day4 RMSharmaine Sur100% (1)

- The Following Data Pertain To Lincoln Corporation On December 31Document8 pagesThe Following Data Pertain To Lincoln Corporation On December 31Eiuol Nhoj Arraeugse100% (3)

- Financial Asset at Amortized CostDocument14 pagesFinancial Asset at Amortized CostLorenzo Diaz DipadNo ratings yet

- P 1Document8 pagesP 1Ken Mosende TakizawaNo ratings yet

- P1 CompreDocument3 pagesP1 CompreCris Tarrazona CasipleNo ratings yet

- Encantadia Practice SetDocument17 pagesEncantadia Practice SetIrahq Yarte Torrejos100% (2)

- Intermacc Receivables Postlec WaDocument3 pagesIntermacc Receivables Postlec WaClarice Awa-aoNo ratings yet

- Module 1 Notes and Loans Receivable PDFDocument43 pagesModule 1 Notes and Loans Receivable PDFALEXA GENMARY GULFAN0% (1)

- FA REV PRB - Prelim Exam Wit Ans Key LatestDocument13 pagesFA REV PRB - Prelim Exam Wit Ans Key LatestLuiNo ratings yet

- Proof of Cash ProblemDocument4 pagesProof of Cash ProblemHtiduj Oretubag50% (4)

- Chapter 19 - Financial Asset at Amortized Cost PDFDocument21 pagesChapter 19 - Financial Asset at Amortized Cost PDFTurksNo ratings yet

- Which Is Incorrect Concerning Self-Constructed Asset?: Correct Mark 1.00 Out of 1.00Document30 pagesWhich Is Incorrect Concerning Self-Constructed Asset?: Correct Mark 1.00 Out of 1.00Gwendolyn PansoyNo ratings yet

- RECEIVABLESDocument28 pagesRECEIVABLESClarice Ilustre Guintibano100% (1)

- Ppe 2Document7 pagesPpe 2Lara Lewis Achilles50% (2)

- Acctg 121 - Trade and Other ReceivablesDocument6 pagesAcctg 121 - Trade and Other ReceivablesYricaNo ratings yet

- MILJANE PERDIZO - Assignment 2Document5 pagesMILJANE PERDIZO - Assignment 2Miljane PerdizoNo ratings yet

- AnswerQuiz - Module 8Document4 pagesAnswerQuiz - Module 8Alyanna AlcantaraNo ratings yet

- Intermacc Inventories and Bio Assets Postlec WaDocument2 pagesIntermacc Inventories and Bio Assets Postlec WaClarice Awa-aoNo ratings yet

- 1907 Notes Receivable and Loan ImpairmentDocument4 pages1907 Notes Receivable and Loan ImpairmentCykee Hanna Quizo Lumongsod100% (2)

- Ama AccountingDocument3 pagesAma AccountingGabriel JacaNo ratings yet

- Chapter 11 Answers RepportDocument12 pagesChapter 11 Answers RepportJudy56% (16)

- Investment in Bonds / Financial Assets at Amortized CostDocument1 pageInvestment in Bonds / Financial Assets at Amortized CostSteffanie Olivar0% (1)

- Additional Problems For Ppe - Acct202: Problem #1Document1 pageAdditional Problems For Ppe - Acct202: Problem #1Excelsia Grace A. ParreñoNo ratings yet

- Quiz Notes and Loans Receivable SY 2022 2023 SolutionDocument4 pagesQuiz Notes and Loans Receivable SY 2022 2023 Solutionreagan blaireNo ratings yet

- Module 13 Present ValueDocument10 pagesModule 13 Present ValueChristine Elaine LamanNo ratings yet

- Chapter 7 - Loans ReceivableDocument15 pagesChapter 7 - Loans ReceivableTurksNo ratings yet

- Polytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsDocument15 pagesPolytechnic University of The Philippines College of Accountancy Junior Philippine Institute of AccountantsYassi CurtisNo ratings yet

- Mod 04 - Trade A - RDocument2 pagesMod 04 - Trade A - RMARY GRACE VARGAS0% (1)

- Retake: Financial Accounting and ReportingDocument21 pagesRetake: Financial Accounting and ReportingJan ryanNo ratings yet

- Petty Cash - Imprest and Fluctuating SystemDocument4 pagesPetty Cash - Imprest and Fluctuating SystemNika Bautista100% (1)

- Dysas - Fin Acc - 3rdDocument5 pagesDysas - Fin Acc - 3rdJao FloresNo ratings yet

- Bank Reconciliation ProblemsDocument2 pagesBank Reconciliation ProblemsCris Jung80% (5)

- Chapter22 BuenaventuraDocument4 pagesChapter22 BuenaventuraAnonnNo ratings yet

- Inventory LatojaDocument2 pagesInventory Latojalisa juganNo ratings yet

- Cash and Cash EquivalentsDocument8 pagesCash and Cash EquivalentsRonel CaagbayNo ratings yet

- DepletionDocument6 pagesDepletionjemjem14No ratings yet

- Retail Method and Biological AssetDocument3 pagesRetail Method and Biological AssetLuiNo ratings yet

- Quiz - 5B 2Document3 pagesQuiz - 5B 2Jao FloresNo ratings yet

- Audit of ReceivableDocument4 pagesAudit of ReceivableMark Lord Morales Bumagat100% (2)

- D. Discounted - YES Pledged - NODocument9 pagesD. Discounted - YES Pledged - NOJasper LuagueNo ratings yet

- 103 CompilationDocument12 pages103 CompilationLyn AbudaNo ratings yet

- Drills Acc 108 Sem EnderDocument10 pagesDrills Acc 108 Sem Enderbrmo.amatorio.uiNo ratings yet

- Practice Exercise (Loans Receivable) Problem 1Document1 pagePractice Exercise (Loans Receivable) Problem 1zxcvbnmNo ratings yet

- 3 - Accounting For Loans and ImpairmentDocument1 page3 - Accounting For Loans and ImpairmentReese AyessaNo ratings yet

- BP MidtermDocument4 pagesBP MidtermGelyn CruzNo ratings yet

- Ais 1Document48 pagesAis 1Gelyn CruzNo ratings yet

- Chapter 12Document27 pagesChapter 12Gelyn CruzNo ratings yet

- Chapter 8Document6 pagesChapter 8Gelyn CruzNo ratings yet

- A. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsDocument1 pageA. B. C. D. E. F. G. H. I. J.: Speeches For All OccassionsGelyn CruzNo ratings yet

- Chapter 24Document20 pagesChapter 24Gelyn CruzNo ratings yet

- Bsa 1Document110 pagesBsa 1Gelyn CruzNo ratings yet

- Decision MakingDocument28 pagesDecision MakingGelyn CruzNo ratings yet

- CRC-ACE PW-TaxDocument14 pagesCRC-ACE PW-TaxGelyn CruzNo ratings yet

- Phase I-Risk Assessment Planning The AudDocument21 pagesPhase I-Risk Assessment Planning The AudGelyn CruzNo ratings yet

- Accounting Information SystemDocument48 pagesAccounting Information SystemGelyn CruzNo ratings yet

- Thesis It To Be FinalizeDocument29 pagesThesis It To Be FinalizeGelyn CruzNo ratings yet

- Auditing Theory TEST BANKDocument23 pagesAuditing Theory TEST BANKGelyn CruzNo ratings yet

- Reaction PaperDocument3 pagesReaction PaperGelyn CruzNo ratings yet

- Research Questionnaire: TH TH THDocument4 pagesResearch Questionnaire: TH TH THGelyn CruzNo ratings yet

- MS - EconomicsDocument16 pagesMS - EconomicsGelyn CruzNo ratings yet

- Test Bank Chapter 1 Managerial AccountingDocument9 pagesTest Bank Chapter 1 Managerial AccountingGelyn CruzNo ratings yet

- Responsibility Acctg, Transfer Pricing & GP AnalysisDocument21 pagesResponsibility Acctg, Transfer Pricing & GP AnalysisGelyn CruzNo ratings yet

- John Gokongwei1Document4 pagesJohn Gokongwei1Gelyn CruzNo ratings yet

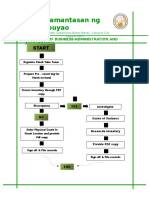

- Pamantasan NG Cabuyao: College of Business Administration and AccountancyDocument1 pagePamantasan NG Cabuyao: College of Business Administration and AccountancyGelyn CruzNo ratings yet

- 1iab SampleDocument52 pages1iab SampleGelyn CruzNo ratings yet

- Chapter 11 Cash Flow Estimation and Risk Analysis PDFDocument80 pagesChapter 11 Cash Flow Estimation and Risk Analysis PDFGelyn Cruz100% (1)

- Thesis Pattern ItDocument1 pageThesis Pattern ItGelyn CruzNo ratings yet

- Citi InsightDocument16 pagesCiti InsightPopeye AlexNo ratings yet

- IFRS 9 Financial Instruments (Hedge Accounting and Amendments To IFRS 9, IFRS 7 and IAS 39) Implementation GuidanceDocument55 pagesIFRS 9 Financial Instruments (Hedge Accounting and Amendments To IFRS 9, IFRS 7 and IAS 39) Implementation GuidancePaul GeorgeNo ratings yet

- Contest MASDocument29 pagesContest MASTerence Jeff Tamondong100% (1)

- Audit of InvestmentsDocument6 pagesAudit of InvestmentsGille Rosa AbajarNo ratings yet

- Serie de Matematicas Financieras 3Document11 pagesSerie de Matematicas Financieras 3Alexander RebolledoNo ratings yet

- GibsonDocument17 pagesGibsonViclynLoveMesagrandeNo ratings yet

- 2Document5 pages2HuyenKhanhNo ratings yet

- Second Examination - Finance 3320 - Spring 2011 (Moore)Document9 pagesSecond Examination - Finance 3320 - Spring 2011 (Moore)Randall McVayNo ratings yet

- BBA 7th Semester Syllabus 2016 PDFDocument63 pagesBBA 7th Semester Syllabus 2016 PDFSagar AdhikariNo ratings yet

- LIABILITIESDocument12 pagesLIABILITIESAimee NucumNo ratings yet

- Lecture - Interest Rate SwapDocument26 pagesLecture - Interest Rate SwapKamran AbdullahNo ratings yet

- 6904 PPT Materials For UploadDocument5 pages6904 PPT Materials For UploadAljur SalamedaNo ratings yet

- Valuation of Bonds and Stock: Objectives: After Reading His Chapter, You WillDocument23 pagesValuation of Bonds and Stock: Objectives: After Reading His Chapter, You WillAnkit PatnaikNo ratings yet

- Capital Market: Subject: Indian Financial System (Ifs)Document8 pagesCapital Market: Subject: Indian Financial System (Ifs)Nayana hyNo ratings yet

- HW 3Document24 pagesHW 3Matthew RyanNo ratings yet

- Compendium Petitioner AnonymousDocument105 pagesCompendium Petitioner Anonymouspratham mohantyNo ratings yet

- CH 14Document35 pagesCH 14Shaneen AdorableNo ratings yet

- Advanced Financial Accounting 10th Edition Christensen Test Bank 2Document35 pagesAdvanced Financial Accounting 10th Edition Christensen Test Bank 2estelleflowerssgsop100% (17)

- Wiley CFA Society Mock Exam 2020 Level I Afternoon QuestionsDocument33 pagesWiley CFA Society Mock Exam 2020 Level I Afternoon QuestionsThaamier Misbach100% (1)

- Module 8 - Bonds PayableDocument6 pagesModule 8 - Bonds PayableLui100% (2)

- FINMAN ReviewerDocument45 pagesFINMAN ReviewerGadfrey Doy-acNo ratings yet

- QuestionsDocument9 pagesQuestionsShaheer BaigNo ratings yet

- Answers Quiz2Document3 pagesAnswers Quiz2Salim MattarNo ratings yet

- INVESTMENTS-HO-5-SOL-GUIDE-PP-1-2 EditedDocument1 pageINVESTMENTS-HO-5-SOL-GUIDE-PP-1-2 EditedKendrew SujideNo ratings yet

- Question Paper Security Analysis - I (211)Document22 pagesQuestion Paper Security Analysis - I (211)Raghavendra Rajendra Basvan100% (1)

- Section A: Answer All QuestionsDocument4 pagesSection A: Answer All QuestionsK LalwaniNo ratings yet

- G1 (Sanket Awate) Pem PFSDocument5 pagesG1 (Sanket Awate) Pem PFSNirank JadhavNo ratings yet

- International Capital Markets - AnkurDocument24 pagesInternational Capital Markets - AnkurRaj K GahlotNo ratings yet

- Financial Markets: Dr. Ekta Shah Mba Sem-3 Sal Institute of ManagementDocument33 pagesFinancial Markets: Dr. Ekta Shah Mba Sem-3 Sal Institute of Managementekta mehtaNo ratings yet

- Learning Module 4 IpmDocument6 pagesLearning Module 4 IpmAira Abigail100% (1)