You might also like

- Gale Researcher Guide for: The Role of Institutions and InfrastructureFrom EverandGale Researcher Guide for: The Role of Institutions and InfrastructureNo ratings yet

- Finance and Economic Growth Nexus: Case of ZimbabweDocument23 pagesFinance and Economic Growth Nexus: Case of ZimbabweMoses ChungaNo ratings yet

- CH1, CH2 1Document46 pagesCH1, CH2 1USAMA RAJANo ratings yet

- Banking System, Institutional Quality, and Economic Growth: Panel Data Analysis On A Sample of Countries in The MENA RegionDocument7 pagesBanking System, Institutional Quality, and Economic Growth: Panel Data Analysis On A Sample of Countries in The MENA RegionRabaa DooriiNo ratings yet

- Financial Development, Investment, and Economic Growth: Xu, ZhenhuiDocument17 pagesFinancial Development, Investment, and Economic Growth: Xu, ZhenhuiMihaela NicoaraNo ratings yet

- Financial Sector Development and Economic Growth: Evidence From ZimbabweDocument12 pagesFinancial Sector Development and Economic Growth: Evidence From ZimbabweDhienna AyoeNo ratings yet

- Financial Repression and Economic Growth : Nouriel Roubini and Xavier Sala-i-MartinDocument26 pagesFinancial Repression and Economic Growth : Nouriel Roubini and Xavier Sala-i-Martinrajeshwar panyalaNo ratings yet

- AfricaDocument30 pagesAfricaSaad HameedNo ratings yet

- IISTE November Issue High Impact FactorsDocument9 pagesIISTE November Issue High Impact FactorsPraise IgweonuNo ratings yet

- Finance-Led Growth Hypothesis in The Philippines: A Granger Causality TestDocument17 pagesFinance-Led Growth Hypothesis in The Philippines: A Granger Causality TestHealthyYOUNo ratings yet

- Asian & GlobalDocument8 pagesAsian & GlobalJuhith RathodNo ratings yet

- Tanvir Sir1Document14 pagesTanvir Sir1tania abdullahNo ratings yet

- Effects of Financial Inclusion On The Economic Growth of Nigeria 1982 2012Document18 pagesEffects of Financial Inclusion On The Economic Growth of Nigeria 1982 2012Devika100% (1)

- Financial Development and Economic Growth: Theory and A Survey of EvidenceDocument29 pagesFinancial Development and Economic Growth: Theory and A Survey of EvidenceFeleke TerefeNo ratings yet

- 18 PBR Journal2018Document14 pages18 PBR Journal2018MuhsinNo ratings yet

- Debt, Deficit and Inflation Linkages, An Optimal Combination For Economic StabilityDocument6 pagesDebt, Deficit and Inflation Linkages, An Optimal Combination For Economic StabilityZunoor AdnanNo ratings yet

- Causal Nexus Between Innovation, Financial Development, and Economic Growth: The Case of OECD CountriesDocument32 pagesCausal Nexus Between Innovation, Financial Development, and Economic Growth: The Case of OECD Countriesusmanshaukat311No ratings yet

- The Impact of Integrated Financial Management System On Economic Development: The Case of GhanaDocument20 pagesThe Impact of Integrated Financial Management System On Economic Development: The Case of GhanaLaMine N'tambi-SanogoNo ratings yet

- Sources of GrowthDocument29 pagesSources of GrowthSamsonNo ratings yet

- Cyclical Fiscal PolicyDocument58 pagesCyclical Fiscal PolicyamudaryoNo ratings yet

- Examining The Fiscal Policy-Poverty Reduction Nexus in NigeriaDocument18 pagesExamining The Fiscal Policy-Poverty Reduction Nexus in NigeriaNova TambunanNo ratings yet

- Fiscal Deficits and Economic GrowthDocument19 pagesFiscal Deficits and Economic Growthtonya93No ratings yet

- Thesis Outline (10-6-16)Document14 pagesThesis Outline (10-6-16)Umer IqbalNo ratings yet

- Finance and Development: Grégoire Mollier BAI 3A G4Document4 pagesFinance and Development: Grégoire Mollier BAI 3A G4Gregoire MollierNo ratings yet

- The Impact of Financial Development On Economic Growth of NigeriaDocument13 pagesThe Impact of Financial Development On Economic Growth of NigeriaPORI ENTERPRISESNo ratings yet

- Re-Examining The Finance-Growth Nexus: Structural Break, Threshold Cointegration and Causality Evidence From The EcowasDocument23 pagesRe-Examining The Finance-Growth Nexus: Structural Break, Threshold Cointegration and Causality Evidence From The EcowasHelali KamelNo ratings yet

- Foreign Direct Investment, Financial DevelopmentDocument16 pagesForeign Direct Investment, Financial DevelopmentRabaa DooriiNo ratings yet

- Does Financial Development Cause Economic Growth Time-Series Evidence From 16 Countries PDFDocument25 pagesDoes Financial Development Cause Economic Growth Time-Series Evidence From 16 Countries PDFMarita Jocelin BauerNo ratings yet

- Literature Review. Financial IntegrationDocument8 pagesLiterature Review. Financial IntegrationjainsfranNo ratings yet

- System GMM Model-Financial Deepening and Economic GrowthDocument12 pagesSystem GMM Model-Financial Deepening and Economic GrowthNur AlamNo ratings yet

- Financial Structure of Nigerian EconomyDocument27 pagesFinancial Structure of Nigerian EconomyDamilare O OlawaleNo ratings yet

- Economic Determinants of Corporate Capital Structure: The Case of Tunisian FirmsDocument7 pagesEconomic Determinants of Corporate Capital Structure: The Case of Tunisian FirmsMissaoui IbtissemNo ratings yet

- Financial Development and Economic GrowthDocument22 pagesFinancial Development and Economic GrowthVANSHIKA BHAIYA 2033479No ratings yet

- Jurnal Internasional 1Document11 pagesJurnal Internasional 1Enggus SetiawanNo ratings yet

- #######Document16 pages#######Bereket RegassaNo ratings yet

- A 65 669-676 Amended Research Article of Co - ANJUMDocument8 pagesA 65 669-676 Amended Research Article of Co - ANJUMshazia bilalNo ratings yet

- Global InflationDocument7 pagesGlobal InflationJeremiah AnjorinNo ratings yet

- 6 TranThiPhuongDocument26 pages6 TranThiPhuongK60 Trương Khả DiNo ratings yet

- Jurnal BPPK: Volume 1, Nomor 4, Oktober 2010Document43 pagesJurnal BPPK: Volume 1, Nomor 4, Oktober 2010danielNo ratings yet

- 1 PDFDocument21 pages1 PDFNA NANo ratings yet

- SSRN Id2765755Document52 pagesSSRN Id2765755Adnan AhmadNo ratings yet

- Pide ArticleDocument24 pagesPide ArticleAtiq ur Rehman QamarNo ratings yet

- Impact of Public Debt On Economic Growth: Evidence From Indian StatesDocument34 pagesImpact of Public Debt On Economic Growth: Evidence From Indian Stateshashim AbdulahiNo ratings yet

- A Simultaneous Equation Model of Economic Growth, FDI and Government Policy in ChinaDocument47 pagesA Simultaneous Equation Model of Economic Growth, FDI and Government Policy in ChinaIvoy VanhostenNo ratings yet

- Financial Inclusion and Inequality: A Cross-Country AnalysisDocument32 pagesFinancial Inclusion and Inequality: A Cross-Country AnalysisRjendra LamsalNo ratings yet

- Government Budget Deficit and Economic GrowthDocument16 pagesGovernment Budget Deficit and Economic GrowthTham NguyenNo ratings yet

- BudgetethiopiayemaneDocument19 pagesBudgetethiopiayemaneHenok EnkuselassieNo ratings yet

- Financial Liberalization: (Insert Figure 1 About Here)Document13 pagesFinancial Liberalization: (Insert Figure 1 About Here)Maria LilyNo ratings yet

- Asian Economic and Financial ReviewDocument13 pagesAsian Economic and Financial ReviewRana Zeshan ArshadNo ratings yet

- Financial Instability and Inequality Dynamics in The WAEMUDocument20 pagesFinancial Instability and Inequality Dynamics in The WAEMUNizar HezziNo ratings yet

- A Guide For Deficit Reduction in The United States Based On Historical Consolidations That WorkedDocument65 pagesA Guide For Deficit Reduction in The United States Based On Historical Consolidations That Workedrichardck61No ratings yet

- Jurnal Financial Developing PDFDocument12 pagesJurnal Financial Developing PDFMichael ComunityNo ratings yet

- Working Paper: Financial Stability and Economic PerformanceDocument34 pagesWorking Paper: Financial Stability and Economic Performancekhemakhem mhamed aliNo ratings yet

- Applied Term PaperDocument8 pagesApplied Term PapershaguftaNo ratings yet

- The Effect of Financial Structure and Economic Growth: An Empirical ApproachDocument9 pagesThe Effect of Financial Structure and Economic Growth: An Empirical ApproachIAEME PublicationNo ratings yet

- Comparative Economic ResearchDocument26 pagesComparative Economic ResearchdanoshkenNo ratings yet

- Journal of Development Economics: Andrei A. Levchenko, Romain Rancière, Mathias ThoenigDocument13 pagesJournal of Development Economics: Andrei A. Levchenko, Romain Rancière, Mathias Thoenigvikas1tehariaNo ratings yet

- Hathroubi, S 2019Document36 pagesHathroubi, S 2019Filipa CoelhoNo ratings yet

- Academia EdiDocument14 pagesAcademia EdiRia LestariNo ratings yet

- A Simultaneous Equation Model of Economic Growth, Fdi and Government Policy in ChinaDocument48 pagesA Simultaneous Equation Model of Economic Growth, Fdi and Government Policy in ChinaR HadimanNo ratings yet

- Crypto Safe Haven in Covid-2Document13 pagesCrypto Safe Haven in Covid-2RazaNo ratings yet

- Credit Risk-COVIDDocument6 pagesCredit Risk-COVIDRazaNo ratings yet

- Robert DavidsonDocument32 pagesRobert DavidsonRazaNo ratings yet

- Challenge To Resource Based View Theory (A Case of Chenone Store)Document9 pagesChallenge To Resource Based View Theory (A Case of Chenone Store)RazaNo ratings yet

- Module 2 L2 Pest AnalysisDocument2 pagesModule 2 L2 Pest AnalysisBLOCK 8 / TAMAYO / K.No ratings yet

- Duke ProjectDocument39 pagesDuke ProjectDuggal ShikhaNo ratings yet

- Applying Hegemony and Power Theory To TransboundarDocument11 pagesApplying Hegemony and Power Theory To TransboundarEsthher RománNo ratings yet

- Microeconomics 9th Edition Colander Solutions ManualDocument10 pagesMicroeconomics 9th Edition Colander Solutions Manualrydervyzk31bj100% (27)

- 01 Technical Analysis - Level 1 - Kunal JoshiDocument267 pages01 Technical Analysis - Level 1 - Kunal Joshisandeep chaurasiaNo ratings yet

- Examination: Subject CT1 Financial Mathematics Core TechnicalDocument211 pagesExamination: Subject CT1 Financial Mathematics Core TechnicalMfundo MshenguNo ratings yet

- Economics Problem SetDocument3 pagesEconomics Problem SetSankar AdhikariNo ratings yet

- Channel of DistributionDocument25 pagesChannel of DistributionSrishti ShekhawatNo ratings yet

- Inclusive Green GrowthDocument192 pagesInclusive Green GrowthLiz Yoha AnguloNo ratings yet

- Midterm Examination BeeDocument18 pagesMidterm Examination BeeMariette Alex AgbanlogNo ratings yet

- BA 540 (Homework-1)Document6 pagesBA 540 (Homework-1)MariaNo ratings yet

- All Math pdf2Document6 pagesAll Math pdf2MD Hafizul Islam HafizNo ratings yet

- Jibo Stock ReturnDocument165 pagesJibo Stock ReturnsaminukaitaNo ratings yet

- Hitting The Sweet Spot PDFDocument12 pagesHitting The Sweet Spot PDFCharlene OmzNo ratings yet

- IV Sem MBA - TM - Supply Chain Management Model Paper 2013Document2 pagesIV Sem MBA - TM - Supply Chain Management Model Paper 2013vikramvsu0% (1)

- Mie L1 AbDocument38 pagesMie L1 AbSakshi MNo ratings yet

- Microeconomics Exam Study GuideDocument29 pagesMicroeconomics Exam Study GuideAndrew HoNo ratings yet

- QEP 2022 Theme General State TheIAShub Sample FIDocument26 pagesQEP 2022 Theme General State TheIAShub Sample FIakash bhattNo ratings yet

- FS WP Amadeus-Airport-A4 11dec17 FINALDocument44 pagesFS WP Amadeus-Airport-A4 11dec17 FINALaidaNo ratings yet

- Production Possibility: Curve (PPC)Document33 pagesProduction Possibility: Curve (PPC)quratulainNo ratings yet

- Cengage Eco Dev Chapter 1 - Introduction To EconomicsDocument38 pagesCengage Eco Dev Chapter 1 - Introduction To EconomicsAngelo TipaneroNo ratings yet

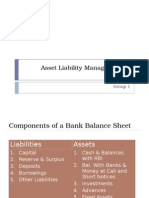

- Asset Liability Management in Banks: Group 1Document29 pagesAsset Liability Management in Banks: Group 1AjDonNo ratings yet

- Period End ChecklistDocument4 pagesPeriod End Checklistsneel.bw3636No ratings yet

- 0450 s13 QP 13Document12 pages0450 s13 QP 13Pramudith LiyanageNo ratings yet

- Pangea Property Outlook 2021 - SwedenDocument48 pagesPangea Property Outlook 2021 - SwedenPuneet PandianNo ratings yet

- Marketing Plan Liquid EggDocument30 pagesMarketing Plan Liquid EggK. J. M. Rezaur Rahman100% (1)

- Management AccountingDocument14 pagesManagement AccountingAbhishek ShahNo ratings yet

- Visu 4Document5 pagesVisu 4HIyer CARNo ratings yet

- CRE Chartbook 4Q 2012Document11 pagesCRE Chartbook 4Q 2012subwayguyNo ratings yet

- The Fall and Rise of Development EconomicsDocument17 pagesThe Fall and Rise of Development EconomicsJavier SolanoNo ratings yet