You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

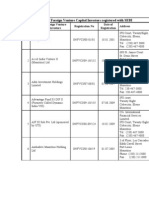

- A-List of Foreign Venture Capital Investors Registered With SEBIDocument24 pagesA-List of Foreign Venture Capital Investors Registered With SEBIVipul ParekhNo ratings yet

- ERP Practice Exam4 7115Document40 pagesERP Practice Exam4 7115Sakthivel Balakrishnan100% (1)

- Lehman Risk Model Sep 2009Document10 pagesLehman Risk Model Sep 2009domokane100% (1)

- College Internship ReportDocument43 pagesCollege Internship ReportGopi Krishnan.n50% (2)

- Sbi Mutual FundsDocument48 pagesSbi Mutual FundsJai Bindal 1 8 3 6 4No ratings yet

- Option Delta With Skew AdjustmentDocument33 pagesOption Delta With Skew AdjustmentTze Shao100% (1)

- Mercantile 1Document313 pagesMercantile 1Ziaul HuqNo ratings yet

- 200922516580254 (1)Document14 pages200922516580254 (1)Jalisa MassiahNo ratings yet

- TH0960CDDocument115 pagesTH0960CDsaroj maharjanNo ratings yet

- Mcqs Help FahadDocument7 pagesMcqs Help FahadAREEBA ABDUL MAJEEDNo ratings yet

- ArbitragePricing Set1Document41 pagesArbitragePricing Set1Pablo DiegoNo ratings yet

- Question No.1 Is Compulsory. Answer Any Questions From The Remaining Six Questions Working Notes Should Form Part of The Answers (MARKS 100)Document6 pagesQuestion No.1 Is Compulsory. Answer Any Questions From The Remaining Six Questions Working Notes Should Form Part of The Answers (MARKS 100)rahul26665323No ratings yet

- Chapter 3 MBF Financial SysDocument24 pagesChapter 3 MBF Financial SysDuy Anh NguyễnNo ratings yet

- Financial Performance Analysis of First Security Islami Bank LimitedDocument21 pagesFinancial Performance Analysis of First Security Islami Bank LimitedSabrinaIra50% (2)

- RL Reco Fund Tracker 181214Document5 pagesRL Reco Fund Tracker 181214techkasambaNo ratings yet

- E-Commerce (Business Communication)Document10 pagesE-Commerce (Business Communication)deeepshahhNo ratings yet

- Target Markets and Channel Design (Chapter 8)Document19 pagesTarget Markets and Channel Design (Chapter 8)Jessa Mae IgotNo ratings yet

- Financial AnalysisDocument40 pagesFinancial AnalysisJephthah BansahNo ratings yet

- The European Bond BasisDocument2 pagesThe European Bond BasisianseowNo ratings yet

- Ccme Nhs Feb1stDocument7 pagesCcme Nhs Feb1stgknyakoNo ratings yet

- Basel 123Document6 pagesBasel 123Iwak TeriNo ratings yet

- PER Guide To A Career in SecondariesDocument11 pagesPER Guide To A Career in SecondariesMarco ErmantazziNo ratings yet

- Systematic Portfolios Guidebook - 2023Document43 pagesSystematic Portfolios Guidebook - 2023JIONGXINNo ratings yet

- Notes - Class 4Document3 pagesNotes - Class 4Majed Abou AlkhirNo ratings yet

- AF Tugas 8 - RifqahDocument8 pagesAF Tugas 8 - RifqahFadhi LullahNo ratings yet

- Trading Binary Options For Fun and Profit - Google BooksDocument1 pageTrading Binary Options For Fun and Profit - Google Bookskhizeewolff90No ratings yet

- Ratio Analysis For Nissan (2008) : Liquidity Ratios RatiosDocument2 pagesRatio Analysis For Nissan (2008) : Liquidity Ratios Ratiosatifrazzaq007No ratings yet

- Arvind Fashions Limited Annual Report For FY-2020 2021 CompressedDocument257 pagesArvind Fashions Limited Annual Report For FY-2020 2021 CompressedUDIT GUPTANo ratings yet

- Regulatory Framework and Role of Domestic Credit Rating Agencies in BangladeshDocument46 pagesRegulatory Framework and Role of Domestic Credit Rating Agencies in BangladeshAsian Development BankNo ratings yet

- ACC 122 Financial Accounting Case Online CORRECTEDDocument4 pagesACC 122 Financial Accounting Case Online CORRECTEDDeepak DohareNo ratings yet