You might also like

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- 2708183603policy Initiatives - Reserve Bank of IndiaDocument6 pages2708183603policy Initiatives - Reserve Bank of IndiaMonika SainiNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- International Financial SystemDocument22 pagesInternational Financial SystemMonika SainiNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- DMGT549 International Financial Management PDFDocument249 pagesDMGT549 International Financial Management PDFMonika SainiNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- ClearancesDocument3 pagesClearancesmanchiprasadNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Chapter 16: Managing Risk in An Organization:, January 2003, P. 8Document34 pagesChapter 16: Managing Risk in An Organization:, January 2003, P. 8Monika SainiNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Paper: 08, International Business Operations: ManagementDocument15 pagesPaper: 08, International Business Operations: ManagementMonika SainiNo ratings yet

- Basel Norms for Capital Adequacy ExplainedDocument12 pagesBasel Norms for Capital Adequacy ExplainedMonika SainiNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- VII. International Financial Markets: HighlightsDocument22 pagesVII. International Financial Markets: HighlightsMonika SainiNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Paper: 08, International Business Operations: ManagementDocument15 pagesPaper: 08, International Business Operations: ManagementMonika SainiNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- ClearancesDocument3 pagesClearancesmanchiprasadNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Paper: 08, International Business Operations: ManagementDocument14 pagesPaper: 08, International Business Operations: ManagementMonika SainiNo ratings yet

- Paper: 08, International Business Operations: ManagementDocument12 pagesPaper: 08, International Business Operations: ManagementMonika SainiNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- 19 UlabourlawshbDocument197 pages19 UlabourlawshbSaipramod JayanthNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- MIN BRO CHAPTER 2 Final PDFDocument18 pagesMIN BRO CHAPTER 2 Final PDFMonika SainiNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- BuybackDocument7 pagesBuybackRekha SoniNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Financial Derivatives 1Document7 pagesFinancial Derivatives 1Monika SainiNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- IFMDocument46 pagesIFMIvaturiAnithaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Credit PlanningDocument9 pagesCredit PlanningMonika Saini100% (1)

- Theories of MergersDocument8 pagesTheories of MergersRashwanth Tc96% (23)

- IFMDocument46 pagesIFMIvaturiAnithaNo ratings yet

- ClearancesDocument3 pagesClearancesmanchiprasadNo ratings yet

- CREDITDocument26 pagesCREDITMonika SainiNo ratings yet

- FM 406 PDFDocument257 pagesFM 406 PDFWotanngare NawaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- IFMDocument46 pagesIFMIvaturiAnithaNo ratings yet

- IFMDocument46 pagesIFMIvaturiAnithaNo ratings yet

- FM 406 PDFDocument257 pagesFM 406 PDFWotanngare NawaNo ratings yet

- FileHandler PDFDocument46 pagesFileHandler PDFRab RakhaNo ratings yet

- Merchant Banking and Financial Servicest200813Document281 pagesMerchant Banking and Financial Servicest200813Prashant SaxenaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Security Analysis and Portfolio ManagementDocument352 pagesSecurity Analysis and Portfolio ManagementAnonymous V2hyzY1axNo ratings yet

- Form Vat-52Document2 pagesForm Vat-52khajuriaonlineNo ratings yet

- Marico Fund FlowDocument10 pagesMarico Fund FlowAbhishek KothariNo ratings yet

- AMFEIX - Monthly Report (March 2020)Document17 pagesAMFEIX - Monthly Report (March 2020)PoolBTCNo ratings yet

- Chapter 1 Solutions 1Document9 pagesChapter 1 Solutions 1yebegashetNo ratings yet

- Juli 2021Document1 pageJuli 2021Vieny AyuznaNo ratings yet

- Questions On Mariott Case StudyDocument1 pageQuestions On Mariott Case StudyKaran BaruaNo ratings yet

- 2019 Li Mock B-Am-Solutions PDFDocument62 pages2019 Li Mock B-Am-Solutions PDFLucky Sky100% (2)

- Allen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Document317 pagesAllen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Stanford Victims CoalitionNo ratings yet

- Bill statement chargesDocument6 pagesBill statement chargesjjayNo ratings yet

- Reconcile Nostro Februari 2023Document56 pagesReconcile Nostro Februari 2023Riko RudyantoNo ratings yet

- Planet Starbucks Case AnalysisDocument3 pagesPlanet Starbucks Case AnalysisJugraj Dharni50% (2)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ITO notice for escaped incomeDocument2 pagesITO notice for escaped incomeSukalp WarhekarNo ratings yet

- Submitted From:-Shampa Dhali (06) Priyanka Dhoot (07) Neeraj Gupta (14) Hardik Joshi (18) Jitendra MishraDocument24 pagesSubmitted From:-Shampa Dhali (06) Priyanka Dhoot (07) Neeraj Gupta (14) Hardik Joshi (18) Jitendra MishraShompa Dhali NandiNo ratings yet

- Life Cycle of A LoanDocument12 pagesLife Cycle of A LoanSyed Noman AhmedNo ratings yet

- Interview With J Welles WilderDocument7 pagesInterview With J Welles WilderScribd-downloadNo ratings yet

- Cadbury Schweppes DF 2006Document1 pageCadbury Schweppes DF 2006JORGENo ratings yet

- Ghana Stock Exchange CourseDocument7 pagesGhana Stock Exchange CoursePrinceNo ratings yet

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap020 PDFDocument26 pagesSolution Manual Advanced Financial Accounting 8th Edition Baker Chap020 PDFYopie ChandraNo ratings yet

- Dev't Planning - I Chap OneDocument20 pagesDev't Planning - I Chap Oneferewe tesfayeNo ratings yet

- Chicken Business PlanDocument16 pagesChicken Business PlanmschotoNo ratings yet

- Eobi Loan RegDocument6 pagesEobi Loan RegEOBI FEDERATION100% (1)

- Thomas J. Sargent, Jouko Vilmunen Macroeconomics at The Service of Public PolicyDocument240 pagesThomas J. Sargent, Jouko Vilmunen Macroeconomics at The Service of Public PolicyHamad KalafNo ratings yet

- Accounting Instructions 3Document1 pageAccounting Instructions 3Ely DanelNo ratings yet

- A Project On Camparative Study Between Private Sector and Public Sector BanksDocument75 pagesA Project On Camparative Study Between Private Sector and Public Sector Banksthaheerhauf1234No ratings yet

- Engineering Midterm Review: Gradient Series FormulasDocument7 pagesEngineering Midterm Review: Gradient Series FormulasHikaruNo ratings yet

- Neelkanth Palace Shop ValuationDocument3 pagesNeelkanth Palace Shop ValuationRaj GohilNo ratings yet

- 47-Corporate Salary Package - CSPDocument3 pages47-Corporate Salary Package - CSPmevrick_guyNo ratings yet

- ADM 3351-Final With SolutionsDocument14 pagesADM 3351-Final With SolutionsGraeme RalphNo ratings yet

- Working Capital of Coca ColaDocument3 pagesWorking Capital of Coca ColaSagor Aftermath0% (1)

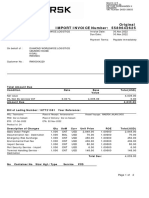

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- My Spiritual Journey: Personal Reflections, Teachings, and TalksFrom EverandMy Spiritual Journey: Personal Reflections, Teachings, and TalksRating: 3.5 out of 5 stars3.5/5 (26)

- Becoming Supernatural: How Common People Are Doing The UncommonFrom EverandBecoming Supernatural: How Common People Are Doing The UncommonRating: 5 out of 5 stars5/5 (1478)

- The Book of Shadows: Discover the Power of the Ancient Wiccan Religion. Learn Forbidden Black Magic Spells and Rituals.From EverandThe Book of Shadows: Discover the Power of the Ancient Wiccan Religion. Learn Forbidden Black Magic Spells and Rituals.Rating: 4 out of 5 stars4/5 (1)

- The Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsFrom EverandThe Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsRating: 3.5 out of 5 stars3.5/5 (3)

- Adventures Beyond the Body: How to Experience Out-of-Body TravelFrom EverandAdventures Beyond the Body: How to Experience Out-of-Body TravelRating: 4.5 out of 5 stars4.5/5 (19)

- Notes from the Universe: New Perspectives from an Old FriendFrom EverandNotes from the Universe: New Perspectives from an Old FriendRating: 4.5 out of 5 stars4.5/5 (53)

- Conversations with God: An Uncommon Dialogue, Book 1From EverandConversations with God: An Uncommon Dialogue, Book 1Rating: 5 out of 5 stars5/5 (66)