You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Secor Chrystal Jean E. Shareholders EquityDocument53 pagesSecor Chrystal Jean E. Shareholders EquityAbriel BumatayNo ratings yet

- Organization and Formation of A CorporationDocument41 pagesOrganization and Formation of A CorporationDennis Udani100% (1)

- IBIG 04 04 Equity Value Enterprise Value Metrics MultiplesDocument94 pagesIBIG 04 04 Equity Value Enterprise Value Metrics MultiplesCarloNo ratings yet

- Debt InstrumentDocument5 pagesDebt InstrumentDhaval JoshiNo ratings yet

- 1-Deal StructuringDocument13 pages1-Deal StructuringNeelabhNo ratings yet

- Final Production PlanDocument35 pagesFinal Production Planllerry racuyaNo ratings yet

- Cost of CapitalDocument99 pagesCost of CapitalRajesh GovardhanNo ratings yet

- MC11 Matcha CreationsDocument3 pagesMC11 Matcha CreationsJuanita ChristieNo ratings yet

- External Factors MatrixDocument7 pagesExternal Factors Matrixllerry racuyaNo ratings yet

- 2 Management Catlyn 3.1 3.3Document11 pages2 Management Catlyn 3.1 3.3llerry racuyaNo ratings yet

- Internal Factor Evaluation Matrix Key Internal Factors Weight Score Weighted Score StrengthsDocument4 pagesInternal Factor Evaluation Matrix Key Internal Factors Weight Score Weighted Score Strengthsllerry racuyaNo ratings yet

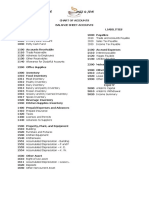

- REAL Chart of AccountsDocument4 pagesREAL Chart of Accountsllerry racuya100% (1)

- Bipedal Is MDocument9 pagesBipedal Is Mllerry racuyaNo ratings yet

- Dividend History of SM Prime Holdings, Inc (2013-2017)Document2 pagesDividend History of SM Prime Holdings, Inc (2013-2017)llerry racuyaNo ratings yet

- 9 - (Cost of Capital) Maulana Rizky FaadillahDocument13 pages9 - (Cost of Capital) Maulana Rizky FaadillahAnanda RiskiNo ratings yet

- 7 Financial MarketsDocument140 pages7 Financial MarketsLe Thuy Dung100% (1)

- Hanoi University Faculty of Management and TourismDocument20 pagesHanoi University Faculty of Management and TourismNguyễn HuyềnNo ratings yet

- Valix 17 20 MCQ and Theory Emp Ben She PDFDocument48 pagesValix 17 20 MCQ and Theory Emp Ben She PDFMitchie FaustinoNo ratings yet

- PRELIM-EXAMS 2223 with-ANSWERDocument5 pagesPRELIM-EXAMS 2223 with-ANSWERbrmo.amatorio.uiNo ratings yet

- Financial Markets and Instruments in GhanaDocument16 pagesFinancial Markets and Instruments in GhanaKwesi Banson Jnr100% (1)

- CIR Vs CADocument21 pagesCIR Vs CAArmie Lyn SimeonNo ratings yet

- Company Law: Corporate and Other Laws: A Capsule For Quick Recap (The Companies Act, 2013)Document14 pagesCompany Law: Corporate and Other Laws: A Capsule For Quick Recap (The Companies Act, 2013)angelNo ratings yet

- United States District Court Central District of California: 8:21-Cv-00403-Jvs-AdsxDocument114 pagesUnited States District Court Central District of California: 8:21-Cv-00403-Jvs-Adsxtriguy_2010No ratings yet

- Chapter 4 PDFDocument24 pagesChapter 4 PDFShoayebNo ratings yet

- 01 Cash & CE CompositionDocument3 pages01 Cash & CE Compositionsharielles /No ratings yet

- Constellation Energy Group 03 Mar 1999Document102 pagesConstellation Energy Group 03 Mar 1999spark4uNo ratings yet

- Financial Investment EXERCISE-1Document16 pagesFinancial Investment EXERCISE-1Quynh NguyenNo ratings yet

- Long Term Sources of FinanceDocument26 pagesLong Term Sources of FinancemustafakarimNo ratings yet

- SEBI - Non-Convertible Debt Securities & Non-Convertible Redeemable Preference SharesDocument18 pagesSEBI - Non-Convertible Debt Securities & Non-Convertible Redeemable Preference SharesDivesh GoyalNo ratings yet

- Chapter 01: The Role and Objective of Financial Management: Answer: ADocument17 pagesChapter 01: The Role and Objective of Financial Management: Answer: AKyla Ramos DiamsayNo ratings yet

- Chap 23 Retained Earnings Dividends Fin Acct 2 - Barter Summary Team PDFDocument3 pagesChap 23 Retained Earnings Dividends Fin Acct 2 - Barter Summary Team PDFSuper JhedNo ratings yet

- Adoption of New Set of Articles of Association (Company Update)Document90 pagesAdoption of New Set of Articles of Association (Company Update)Shyam SunderNo ratings yet

- Financial Statement AnalysisDocument5 pagesFinancial Statement AnalysisErwin Dave M. DahaoNo ratings yet

- Chapter No 06 Final Afs-1Document58 pagesChapter No 06 Final Afs-1salwaburiroNo ratings yet

- Mock Test of Jaiib Principles & Practices of Banking.: AnswerDocument12 pagesMock Test of Jaiib Principles & Practices of Banking.: Answeraao wacNo ratings yet

- R17 - Understanding Income Statements - 2022Document57 pagesR17 - Understanding Income Statements - 2022Ihuomacumeh100% (1)

- Cost of FinanceDocument6 pagesCost of Financeblue benzNo ratings yet