You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Comparison Bet. Ftaa & MpsaDocument10 pagesComparison Bet. Ftaa & Mpsacriselkate100% (1)

- Current Liabilities ManagementDocument18 pagesCurrent Liabilities ManagementAndrew Usatii100% (2)

- Case Study 20202712Document4 pagesCase Study 20202712rabbi sodhiNo ratings yet

- Group 3 - Team Assignment 5Document5 pagesGroup 3 - Team Assignment 5rabbi sodhiNo ratings yet

- Technology at Airbnb: Group 3-Team DeloitteDocument6 pagesTechnology at Airbnb: Group 3-Team Deloitterabbi sodhiNo ratings yet

- Income Statement Analysis: Group - FDocument7 pagesIncome Statement Analysis: Group - Frabbi sodhiNo ratings yet

- Gaps Model of Service Quality Example: Movie PlexDocument19 pagesGaps Model of Service Quality Example: Movie Plexrabbi sodhiNo ratings yet

- BzComm - Givegoa Review ReportDocument10 pagesBzComm - Givegoa Review Reportrabbi sodhiNo ratings yet

- Advisory Board Toolbox 2016Document47 pagesAdvisory Board Toolbox 2016John TurnerNo ratings yet

- Shoe Affair (Factory) - Po-000008724Document2 pagesShoe Affair (Factory) - Po-000008724talentacquistionretailcoordinaNo ratings yet

- October Exam All Year Questions ExamDocument210 pagesOctober Exam All Year Questions ExamSOURAV MONDALNo ratings yet

- Planning in Public Administration-Prankur SharmaDocument35 pagesPlanning in Public Administration-Prankur SharmaPrankur Sharma100% (1)

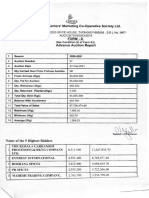

- Auctlon: CP - Mss The Cardamom Planters' Itlarketing Society LTDDocument24 pagesAuctlon: CP - Mss The Cardamom Planters' Itlarketing Society LTDRoshniNo ratings yet

- 12 - Chapter 4 PDFDocument29 pages12 - Chapter 4 PDFNANDANA CHANDRANNo ratings yet

- SG285HX - SG333HX - SG350HX EU Declaration of ConformityDocument2 pagesSG285HX - SG333HX - SG350HX EU Declaration of ConformityeriganiNo ratings yet

- MV Sir - Old TrackerDocument6 pagesMV Sir - Old Trackersnehajainsneha52No ratings yet

- Irfan AlamDocument5 pagesIrfan AlamSatish SauravNo ratings yet

- Changes Under The Customs Modernization and Tariff ActDocument6 pagesChanges Under The Customs Modernization and Tariff Actmami mingNo ratings yet

- India BahrainDocument4 pagesIndia BahrainVikram GuptaNo ratings yet

- Shriram Liberty Square - 99acresDocument24 pagesShriram Liberty Square - 99acresKayjay2050No ratings yet

- Lecture 08Document11 pagesLecture 08Mohamed HanyNo ratings yet

- CR 17319Document82 pagesCR 17319nicodelrioNo ratings yet

- Elasticity of DemandDocument21 pagesElasticity of DemandNitika AggarwalNo ratings yet

- 2017.11.21 Letter To Sessions On No-Poach AgreementsDocument3 pages2017.11.21 Letter To Sessions On No-Poach AgreementsSenator Cory BookerNo ratings yet

- Tuirum Adhaar Update Tur ListDocument4 pagesTuirum Adhaar Update Tur ListLalthlamuana MuanaNo ratings yet

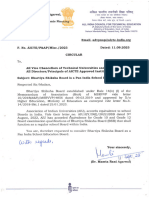

- Bhartiya Shiksha Board CircularDocument1 pageBhartiya Shiksha Board CircularNDTVNo ratings yet

- Metrorail MapDocument2 pagesMetrorail Mapayse432No ratings yet

- Foreign Finance, Investment, and Aid: Controversies and OpportunitiesDocument34 pagesForeign Finance, Investment, and Aid: Controversies and OpportunitiesFahad khan100% (1)

- Essay Writing in Bank ExamsDocument3 pagesEssay Writing in Bank Examsanuraaag123No ratings yet

- Meeting With BCDA - Presentation MaterialDocument10 pagesMeeting With BCDA - Presentation MaterialJohn Jay BenavidezNo ratings yet

- Trade and Investment Policies: True/False QuestionsDocument24 pagesTrade and Investment Policies: True/False QuestionsAshok SubramaniamNo ratings yet

- Management of Non Performing Assets - A Current Scenario: Chandan Chatterjee Jeet Mukherjee DR - Ratan DasDocument11 pagesManagement of Non Performing Assets - A Current Scenario: Chandan Chatterjee Jeet Mukherjee DR - Ratan DasprabindraNo ratings yet

- PR - Interim Order Cum Show Cause Notice Against Shri Priyansh Patodi, Proprietor - MMF SolutionsDocument1 pagePR - Interim Order Cum Show Cause Notice Against Shri Priyansh Patodi, Proprietor - MMF SolutionsShyam SunderNo ratings yet

- Forward Rate AgreementsDocument2 pagesForward Rate Agreementsajain22No ratings yet

- Ail Setup AdxDocument5 pagesAil Setup Adxharish20050% (1)

- Responsibilties of A Professional ManagerDocument11 pagesResponsibilties of A Professional ManagerElma V MuthuNo ratings yet