You might also like

- SAP MM Organization Structure and Master DataDocument3 pagesSAP MM Organization Structure and Master Datanbhaskar bhaskar100% (2)

- Media Planning Media Costs and Buying ProblemsDocument19 pagesMedia Planning Media Costs and Buying ProblemsBilal Munir100% (2)

- Inventory ManagementDocument7 pagesInventory ManagementDavinNo ratings yet

- Translating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationFrom EverandTranslating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationNo ratings yet

- Inventory Management in LiberyDocument101 pagesInventory Management in LiberySamuel DavisNo ratings yet

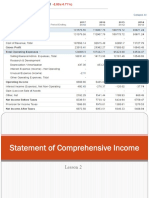

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Hospital ER Diagram Shows Patient, Doctor RelationshipsDocument4 pagesHospital ER Diagram Shows Patient, Doctor RelationshipsKS SubhramaniyamNo ratings yet

- Hospital ER Diagram Shows Patient, Doctor RelationshipsDocument4 pagesHospital ER Diagram Shows Patient, Doctor RelationshipsKS SubhramaniyamNo ratings yet

- MRP exercise lot sizingDocument3 pagesMRP exercise lot sizingJohnyNo ratings yet

- WAR-015 Warehouse Processing Issues Return and Rejects SampleDocument3 pagesWAR-015 Warehouse Processing Issues Return and Rejects Samplesetiawanaji407100% (1)

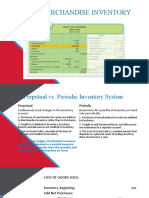

- Accounting For Merchandising OperationsDocument58 pagesAccounting For Merchandising OperationsSalvie Perez UtanaNo ratings yet

- Impact of Inventory Management On The Financial Performance of The FirmDocument12 pagesImpact of Inventory Management On The Financial Performance of The FirmIOSRjournalNo ratings yet

- A Study On Inventory Management and Control: Pratap Chandrakumar. R Gomathi ShankarDocument9 pagesA Study On Inventory Management and Control: Pratap Chandrakumar. R Gomathi Shankarshravasti munwarNo ratings yet

- A Synopsis ON: Inventory ManagementDocument9 pagesA Synopsis ON: Inventory ManagementDEEPAKNo ratings yet

- Rol DeepaDocument5 pagesRol DeepaDeepa DevanNo ratings yet

- Chapter 2Document20 pagesChapter 2PreethaSureshNo ratings yet

- Inventory Turnover Optimization Criteria of Efficiency (With Special Reference To FMCG Sector in India)Document5 pagesInventory Turnover Optimization Criteria of Efficiency (With Special Reference To FMCG Sector in India)Ayesha AtherNo ratings yet

- Review of Working Capital PDFDocument12 pagesReview of Working Capital PDFsandhyaNo ratings yet

- Literarure PDFDocument4 pagesLiterarure PDFLee marie BelarminoNo ratings yet

- An Analytical Study On Inventory Managem PDFDocument6 pagesAn Analytical Study On Inventory Managem PDFPOOJA CHAUDHARINo ratings yet

- Impact of working capital management on firmsDocument8 pagesImpact of working capital management on firmsnational coursesNo ratings yet

- Review of Literature: 2.1 Chapter OverviewDocument37 pagesReview of Literature: 2.1 Chapter OverviewJannpreet KaurNo ratings yet

- Author's Original SubmissionDocument21 pagesAuthor's Original SubmissionDrRashmiranjan PanigrahiNo ratings yet

- G017843443 PDFDocument9 pagesG017843443 PDFRAJA RAMNo ratings yet

- Chapter-2: Review OF LiteratureDocument36 pagesChapter-2: Review OF Literaturekanna_dhasan25581No ratings yet

- The Effectof Inventory Managementon Company Performance Referenceto Listed Manufacturing Companiesin Sri LankaDocument7 pagesThe Effectof Inventory Managementon Company Performance Referenceto Listed Manufacturing Companiesin Sri LankaSyed Shahid SheraziNo ratings yet

- Effective Inventory Management Practice and Firms Performance: Evidence From Nigerian Consumable Goods FirmsDocument12 pagesEffective Inventory Management Practice and Firms Performance: Evidence From Nigerian Consumable Goods FirmsaijbmNo ratings yet

- Inventory Aging Reduction Boosts Automotive Company's CompetitivenessDocument8 pagesInventory Aging Reduction Boosts Automotive Company's CompetitivenessKhaoula RezzoukNo ratings yet

- Impact of Working Capital Management On Profitability: A Case of Pakistan Textile IndustryDocument4 pagesImpact of Working Capital Management On Profitability: A Case of Pakistan Textile IndustryUmar AbbasNo ratings yet

- Working Capital Management Literature ReviewDocument8 pagesWorking Capital Management Literature ReviewGoutam SoniNo ratings yet

- Effects of Inventory Control On Profitability of Industrial and Allied Firms in KenyaDocument8 pagesEffects of Inventory Control On Profitability of Industrial and Allied Firms in KenyaOgunmola femiNo ratings yet

- Article 5Document11 pagesArticle 5Areef BashaNo ratings yet

- Evaluation of Working Capital Management of Indian Oil Corporation Limited - March - 2016 - 6091513501 - 2909783Document3 pagesEvaluation of Working Capital Management of Indian Oil Corporation Limited - March - 2016 - 6091513501 - 2909783Ayesha AmreenNo ratings yet

- Literature ReviewDocument26 pagesLiterature ReviewShahid ShaikhNo ratings yet

- WCM and Profitability in Textiles IndustryDocument18 pagesWCM and Profitability in Textiles IndustryMahesh BendigeriNo ratings yet

- The Impact of Inventory Management Practice On Firms' Competitiveness and Organizational PerformanceDocument19 pagesThe Impact of Inventory Management Practice On Firms' Competitiveness and Organizational PerformanceCynthia WalterNo ratings yet

- Evaluating The Impact of Working Capital Management Components On Corporate Profitability: Evidence From Indian Manufacturing FirmsDocument10 pagesEvaluating The Impact of Working Capital Management Components On Corporate Profitability: Evidence From Indian Manufacturing FirmsderihoodNo ratings yet

- Research Paper On "Efficient Management of Working Capital: A Study of Automobile Industry in India"Document8 pagesResearch Paper On "Efficient Management of Working Capital: A Study of Automobile Industry in India"yash sultaniaNo ratings yet

- 2012 - IsSN - Influence of Working Capital Management On Profitability A Study On Indian FMCG CompaniesDocument10 pages2012 - IsSN - Influence of Working Capital Management On Profitability A Study On Indian FMCG CompaniesThi NguyenNo ratings yet

- Relationship Between Working Capital Management and ProfitabilityDocument5 pagesRelationship Between Working Capital Management and ProfitabilityEditor IJIRMFNo ratings yet

- iJARS 520Document16 pagesiJARS 520Sasi KumarNo ratings yet

- CHAPTER I and IIDocument13 pagesCHAPTER I and IIPritz Marc Bautista MorataNo ratings yet

- Effects of Working Capital Management On SME Profitability: Pedro Juan García TeruelDocument8 pagesEffects of Working Capital Management On SME Profitability: Pedro Juan García TeruelGaurav Kumar BhagatNo ratings yet

- Introduction of Inventory ManagementDocument4 pagesIntroduction of Inventory ManagementPrathyusha ReddyNo ratings yet

- Impact of Inventory Valuation Methods on Financial Reporting of Manufacturing CompaniesDocument33 pagesImpact of Inventory Valuation Methods on Financial Reporting of Manufacturing CompaniesBalogun Felix AyindeNo ratings yet

- A Study On Financial Reengineering in Ashok Leyland Ltd.,hosurDocument8 pagesA Study On Financial Reengineering in Ashok Leyland Ltd.,hosurIJERDNo ratings yet

- Chapter 3Document48 pagesChapter 3SundaraMathavanNo ratings yet

- Working Capital Management in the Plastic Pipe IndustryDocument14 pagesWorking Capital Management in the Plastic Pipe IndustryananthakumarNo ratings yet

- Review of LiteratureDocument9 pagesReview of LiteratureShankar ChinnusamyNo ratings yet

- Project For Fin-IIDocument15 pagesProject For Fin-IIpgcilindore1924No ratings yet

- Chapter 2Document13 pagesChapter 2eswariNo ratings yet

- FMCGDocument15 pagesFMCGRicha ChandraNo ratings yet

- An Empirical Study On Working Capital Management and ProfitabilityDocument5 pagesAn Empirical Study On Working Capital Management and Profitabilityanjali shilpa kajalNo ratings yet

- Integrated Versus Non-Integrated Inventory Management: Full Length Research PaperDocument12 pagesIntegrated Versus Non-Integrated Inventory Management: Full Length Research PaperSamar AsadNo ratings yet

- 1.1 Title of The StudyDocument8 pages1.1 Title of The StudydivyanikeshNo ratings yet

- Monginise Inventory ManagementDocument36 pagesMonginise Inventory ManagementTejNaikNo ratings yet

- Files AllDocument23 pagesFiles AllRosanth Selva RajNo ratings yet

- Of Working Capital MeaningDocument6 pagesOf Working Capital MeaningAkarshit SharmaNo ratings yet

- Working capital impact on FMCG profitabilityDocument10 pagesWorking capital impact on FMCG profitabilitynishaNo ratings yet

- In Uence of Working Capital Management On Profitability: A Study On Indian FMCG CompaniesDocument11 pagesIn Uence of Working Capital Management On Profitability: A Study On Indian FMCG Companieschirag PatwariNo ratings yet

- Forecasting - Docx For Send 1Document2 pagesForecasting - Docx For Send 1James EspaderaNo ratings yet

- CHAPTER I and II - Docx EditedDocument15 pagesCHAPTER I and II - Docx EditedPritz Marc Bautista MorataNo ratings yet

- Capstone 2Document6 pagesCapstone 2Aayush jainNo ratings yet

- REVIEW OF LITERATURE DharaniDocument5 pagesREVIEW OF LITERATURE Dharanigowrimahesh2003No ratings yet

- A Study On Working Capital Management With Special Reference To Tube Products of India Limited, ChennaiDocument41 pagesA Study On Working Capital Management With Special Reference To Tube Products of India Limited, ChennaiBasant NagarNo ratings yet

- SuvithaDocument84 pagesSuvithaVenkatram PrabhuNo ratings yet

- Strengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsFrom EverandStrengthening the Operational Pillar: The Building Blocks of World-Class Production Planning and Inventory Control SystemsNo ratings yet

- Guide to Management Accounting Inventory turnover for managersFrom EverandGuide to Management Accounting Inventory turnover for managersNo ratings yet

- ESDocument1 pageESKS SubhramaniyamNo ratings yet

- NBFCDocument8 pagesNBFCKS SubhramaniyamNo ratings yet

- Pivot Table NitishDocument2 pagesPivot Table NitishKS SubhramaniyamNo ratings yet

- ACCOUNTANCY SAMPLE QUESTION PAPER ANALYSISDocument21 pagesACCOUNTANCY SAMPLE QUESTION PAPER ANALYSISmohit pandeyNo ratings yet

- A Storage and Material Handling Ballou11Document19 pagesA Storage and Material Handling Ballou11Uttkarsh JaiswalNo ratings yet

- I.A 2, Assignment-2Document4 pagesI.A 2, Assignment-2Elea MorataNo ratings yet

- A 85 A 0 Module 2 UpDocument39 pagesA 85 A 0 Module 2 UphimnnnNo ratings yet

- Sol14 4eDocument103 pagesSol14 4eKiều Thảo Anh100% (1)

- Serial Control ItemsDocument2 pagesSerial Control ItemsSurekha RaoNo ratings yet

- Chapter 7 The Conversion Cycle: Batch Processing SystemDocument6 pagesChapter 7 The Conversion Cycle: Batch Processing SystemAnne Rose EncinaNo ratings yet

- Process Costing WorksheetDocument21 pagesProcess Costing WorksheetpchakkrapaniNo ratings yet

- Multi Echelon Inventory EOQDocument4 pagesMulti Echelon Inventory EOQLazyLundNo ratings yet

- Quality Control Inspector or Warehouse or Inventory ControlDocument3 pagesQuality Control Inspector or Warehouse or Inventory Controlapi-77999205No ratings yet

- SCM - Chemtech IncDocument2 pagesSCM - Chemtech IncBalaji Sridharan50% (2)

- Financial Accounting - Chapter 5Document81 pagesFinancial Accounting - Chapter 5Hamza PagaNo ratings yet

- DocxDocument11 pagesDocx?????No ratings yet

- Merchandise Inventory System and CostingDocument13 pagesMerchandise Inventory System and CostingJade PielNo ratings yet

- Azerbaijan State Oil and Industry University: Question #1 (6 Points)Document3 pagesAzerbaijan State Oil and Industry University: Question #1 (6 Points)TaToSh GamerNo ratings yet

- Optimize Inventory Lot Sizes with Dynamic ModelsDocument13 pagesOptimize Inventory Lot Sizes with Dynamic ModelsOtieno MosesNo ratings yet

- AbsorptionDocument28 pagesAbsorptionJenika AtanacioNo ratings yet

- Quiz - Midterm Summative Test 2Document21 pagesQuiz - Midterm Summative Test 2MarkuNo ratings yet

- Myco Paque InventoriesDocument5 pagesMyco Paque InventoriesMYCO PONCE PAQUENo ratings yet

- Is A Construction Company Specializing in Custom PatiosDocument8 pagesIs A Construction Company Specializing in Custom Patioslaale dijaanNo ratings yet

- UNIT 8 SpoilageDocument16 pagesUNIT 8 SpoilageKale MessayNo ratings yet

- INVENTORIES4Document2 pagesINVENTORIES4Katherine MagpantayNo ratings yet

- Valuation of Inventories: A Cost-Basis Approach: Multiple ChoiceDocument34 pagesValuation of Inventories: A Cost-Basis Approach: Multiple ChoicehyosungloverNo ratings yet

- Supply Chain Management at Mahindra & MahindraDocument19 pagesSupply Chain Management at Mahindra & MahindraSiddharthThaparNo ratings yet

- Chapter - 2: Inventory Control: © 1. IntroductionDocument22 pagesChapter - 2: Inventory Control: © 1. IntroductionsajithNo ratings yet