You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Unique Pricing Strategies of FlipkartDocument3 pagesUnique Pricing Strategies of Flipkartpari shuklaNo ratings yet

- Gmail - Paytm - Your Train Ticket - AGRA FORT (AF) - KODERMA (KQR) - 3A PDFDocument4 pagesGmail - Paytm - Your Train Ticket - AGRA FORT (AF) - KODERMA (KQR) - 3A PDFSuraj0% (1)

- 11 Dreamer: App Setup: 1) Download and Install Android StudioDocument7 pages11 Dreamer: App Setup: 1) Download and Install Android StudiosiddharthNo ratings yet

- Human Resources Accounting Concepts Objectives Models and CriticismDocument10 pagesHuman Resources Accounting Concepts Objectives Models and Criticismpavan kumarNo ratings yet

- Unit - 2: Corporate Incorporation and ManagementDocument74 pagesUnit - 2: Corporate Incorporation and Managementpavan kumarNo ratings yet

- ListDocument713 pagesListpavan kumarNo ratings yet

- Annualreport201819forwebfinal PDFDocument356 pagesAnnualreport201819forwebfinal PDFpavan kumarNo ratings yet

- Compitation TribunalDocument6 pagesCompitation Tribunalpavan kumarNo ratings yet

- Oneliners Current Affairs PDFDocument20 pagesOneliners Current Affairs PDFsach5793No ratings yet

- SujeetTiwari Fintech DhanukarFMFT04 PDFDocument10 pagesSujeetTiwari Fintech DhanukarFMFT04 PDFUprising TopicsNo ratings yet

- Account STMT XX4967 23122023Document22 pagesAccount STMT XX4967 23122023Sanjoy RoyNo ratings yet

- Slice Account Statement - Jun '22Document7 pagesSlice Account Statement - Jun '22Gowtham ChallaNo ratings yet

- Ey The Battle For The Indian Consumer PDFDocument44 pagesEy The Battle For The Indian Consumer PDFRAHULMISHRA1188No ratings yet

- IndiaFintech Enablers, NotDisruptors20210929Document69 pagesIndiaFintech Enablers, NotDisruptors20210929Saurabh SharmaNo ratings yet

- Current Affairs April-July, 2016-1 PDFDocument123 pagesCurrent Affairs April-July, 2016-1 PDFtrisha100% (1)

- HDFC Bank Statement FormatDocument15 pagesHDFC Bank Statement FormatMd SharidNo ratings yet

- OpTransactionHistory01 10 2022Document28 pagesOpTransactionHistory01 10 2022Anonymous KlEDCj9No ratings yet

- Project For 6th Semester On EcommerceDocument45 pagesProject For 6th Semester On EcommerceRahul patiNo ratings yet

- Case StudyPaytmDocument21 pagesCase StudyPaytmHemant Sudhir WavhalNo ratings yet

- Statement 2023MTH10 430547526Document4 pagesStatement 2023MTH10 430547526shoykapoorNo ratings yet

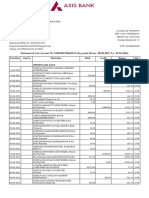

- Statement of Axis Account No:921010025595120 For The Period (From: 01-04-2021 To: 31-03-2022)Document23 pagesStatement of Axis Account No:921010025595120 For The Period (From: 01-04-2021 To: 31-03-2022)Mahakaal Digital PointNo ratings yet

- Jss Science and Technology University: Sri Jayachamarajendra College of Engineering, MysuruDocument11 pagesJss Science and Technology University: Sri Jayachamarajendra College of Engineering, MysuruM-18 Manish K GowdaNo ratings yet

- Paytm Annual Report 2023Document468 pagesPaytm Annual Report 2023greeshmaNo ratings yet

- A Study On Comparison of Customer SatisfactionDocument63 pagesA Study On Comparison of Customer SatisfactionSumith MohanNo ratings yet

- Monthly Current Affairs Capsule September 2018 PDFDocument35 pagesMonthly Current Affairs Capsule September 2018 PDFbhajjiNo ratings yet

- Marketing Strategies of PaytmDocument6 pagesMarketing Strategies of PaytmRethiksha SesurajNo ratings yet

- MD Wasim Ansari, Paytm, PPTDocument20 pagesMD Wasim Ansari, Paytm, PPTMd WasimNo ratings yet

- Ramkesh New Statment-1Document13 pagesRamkesh New Statment-1rajmeenameenaji9797No ratings yet

- Mansi Rawat Major ProjectDocument45 pagesMansi Rawat Major ProjectSunil VermaNo ratings yet

- BBAG MPR and STR LISTSDocument25 pagesBBAG MPR and STR LISTShimanshu ranjanNo ratings yet

- Assignment - Product Manager (Gateway) - SmallcaseDocument7 pagesAssignment - Product Manager (Gateway) - SmallcaseVikash ChoudharyNo ratings yet

- OpTransactionHistory28 09 2021Document30 pagesOpTransactionHistory28 09 2021samboopathiNo ratings yet

- Paytm 6 Months StatementDocument27 pagesPaytm 6 Months StatementRaghav SharmaNo ratings yet

- Vijay Shekhar Sharama India's Youngest Business TycoonDocument11 pagesVijay Shekhar Sharama India's Youngest Business TycoonKrisha SabalparaNo ratings yet

- Statement Jun 20 XXXXXXXX0037Document8 pagesStatement Jun 20 XXXXXXXX0037Harikrishna GoudNo ratings yet