You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Asian Financial Crisis 3Document2 pagesAsian Financial Crisis 3Naila MehboobNo ratings yet

- Memo WritingDocument3 pagesMemo WritingNaila Mehboob100% (1)

- Book 1Document104 pagesBook 1Naila MehboobNo ratings yet

- Book 1Document104 pagesBook 1Naila MehboobNo ratings yet

- Memo WritingDocument3 pagesMemo WritingNaila Mehboob100% (1)

- Asian Financial Crisis 3Document2 pagesAsian Financial Crisis 3Naila MehboobNo ratings yet

- Foreign Policy 3Document3 pagesForeign Policy 3Naila MehboobNo ratings yet

- The Asian Financial Crisis of 1997-1998Document3 pagesThe Asian Financial Crisis of 1997-1998Naila MehboobNo ratings yet

- Memo WritingDocument3 pagesMemo WritingNaila Mehboob100% (1)

- Asian Financial Crisis 2Document3 pagesAsian Financial Crisis 2Naila MehboobNo ratings yet

- Foriegn PolicyDocument3 pagesForiegn PolicyNaila MehboobNo ratings yet

- Asian Financial Crisis 3Document2 pagesAsian Financial Crisis 3Naila MehboobNo ratings yet

- Second Feasibility Report On Opening of Comsats Institute of Information Technology Sub Campus in AbbottabadDocument2 pagesSecond Feasibility Report On Opening of Comsats Institute of Information Technology Sub Campus in AbbottabadNaila MehboobNo ratings yet

- Foreign Policy2Document2 pagesForeign Policy2Naila MehboobNo ratings yet

- EconomicsDocument6 pagesEconomicsNaila MehboobNo ratings yet

- Economic GrowthDocument4 pagesEconomic GrowthNaila MehboobNo ratings yet

- Feasibility Report Opening of Warid FranchiseDocument2 pagesFeasibility Report Opening of Warid FranchiseNaila MehboobNo ratings yet

- Factors of Economic GrowthDocument16 pagesFactors of Economic GrowthNaila MehboobNo ratings yet

- The Bank of KhyberDocument15 pagesThe Bank of KhyberNaila Mehboob100% (2)

- Bank ReconciliationDocument2 pagesBank ReconciliationNaila MehboobNo ratings yet

- Feasibility Report Opening of CIIT Sub Campus in AbbottabadDocument2 pagesFeasibility Report Opening of CIIT Sub Campus in AbbottabadNaila Mehboob100% (1)

- How To Write ProgressReportDocument1 pageHow To Write ProgressReportNaila MehboobNo ratings yet

- Coenzymes and Their Role in Regulation of Metabolic ProcessesDocument1 pageCoenzymes and Their Role in Regulation of Metabolic ProcessesNaila MehboobNo ratings yet

- Pakistan StudiesDocument5 pagesPakistan StudiesNaila MehboobNo ratings yet

- Impact of Performance Appraisal System On Employee Productivity in Telecom Sector of PakistanDocument7 pagesImpact of Performance Appraisal System On Employee Productivity in Telecom Sector of PakistanNaila MehboobNo ratings yet

- Light Visibilty Problem On Motor Way During FogDocument2 pagesLight Visibilty Problem On Motor Way During FogNaila MehboobNo ratings yet

- QuizDocument3 pagesQuizNaila MehboobNo ratings yet

- Telenor Nafisa Interview ReportDocument7 pagesTelenor Nafisa Interview ReportNaila MehboobNo ratings yet

- Assg 2 Methodology Naila Bibi MS (MS) 1Document7 pagesAssg 2 Methodology Naila Bibi MS (MS) 1Naila MehboobNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MRD 2015Document191 pagesMRD 2015Russel SarachoNo ratings yet

- Letter of CreditDocument6 pagesLetter of CreditVarun ChandwaniNo ratings yet

- Key differences between AAOIFI and IFRSDocument10 pagesKey differences between AAOIFI and IFRSE-cHa PineappleNo ratings yet

- OID Demystified (Somewhat)Document6 pagesOID Demystified (Somewhat)Reznick Group NMTC PracticeNo ratings yet

- Reasons Banks Require Liquidity and Capital AdequacyDocument21 pagesReasons Banks Require Liquidity and Capital AdequacyThanhTuyenNguyenNo ratings yet

- ECON212 Sample Final ExamDocument17 pagesECON212 Sample Final Examstharan23No ratings yet

- Managerial Finance Course OverviewDocument23 pagesManagerial Finance Course OverviewDibakar DasNo ratings yet

- Sihi V IacDocument2 pagesSihi V IacFrancis Kyle Cagalingan SubidoNo ratings yet

- UMass Finance 301 Exam Study GuideDocument8 pagesUMass Finance 301 Exam Study GuideMuhammad Waqar ZahidNo ratings yet

- A Research Study On The Effects of CashlDocument93 pagesA Research Study On The Effects of CashlWynona PinlacNo ratings yet

- EAST WEST - Ewb Bills Collect 08302018Document3 pagesEAST WEST - Ewb Bills Collect 08302018Junior MiicNo ratings yet

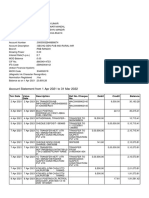

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandNo ratings yet

- 010 G.R. No. 112392 February 29, 2000 BPI Vs CADocument7 pages010 G.R. No. 112392 February 29, 2000 BPI Vs CArodolfoverdidajrNo ratings yet

- Business Transactions and Their AnalysisDocument21 pagesBusiness Transactions and Their AnalysisNelcie Batan100% (1)

- Valuation Report On Multistory Building-Hritik AwasthyDocument13 pagesValuation Report On Multistory Building-Hritik AwasthyEr Hritik AwasthyNo ratings yet

- Govt Central Registry Rules Form IDocument9 pagesGovt Central Registry Rules Form ISonam VijNo ratings yet

- Regulatory Framework for Business Transactions MCQDocument20 pagesRegulatory Framework for Business Transactions MCQEJ EduqueNo ratings yet

- Comparison of Post Office Savings SchemesDocument1 pageComparison of Post Office Savings SchemeskabitabalaNo ratings yet

- Sales Items by Date 04jun2019 03jul2019Document6 pagesSales Items by Date 04jun2019 03jul2019Lia AsyifaNo ratings yet

- Kotak Mahindra BankDocument23 pagesKotak Mahindra BankSai VasudevanNo ratings yet

- Deed of Sale and Mortgage AssumptionDocument1 pageDeed of Sale and Mortgage Assumptiongarrybramos100% (8)

- Research Project Credit CardsDocument9 pagesResearch Project Credit CardsVikas Bansal0% (1)

- Case StudiesDocument21 pagesCase Studiesrinkirola7576No ratings yet

- Interbank GIRO (IBG) MEPS Instant TransferDocument1 pageInterbank GIRO (IBG) MEPS Instant TransferZulhairiNo ratings yet

- T24 CustomerDocument28 pagesT24 CustomerMahmoud Shoman67% (3)

- Hong Kong Banking and Finance NoteDocument4 pagesHong Kong Banking and Finance NoteArrisNo ratings yet

- B1-114091947 Details PDFDocument5 pagesB1-114091947 Details PDFKannanThangavelNo ratings yet

- Jharkhand Draft Industrial Policy 2010Document22 pagesJharkhand Draft Industrial Policy 2010IndustrialpropertyinNo ratings yet

- Pass BookDocument12 pagesPass Booksagarg94gmailcom100% (1)

- Timeline: The Failure of The Royal Bank of ScotlandDocument7 pagesTimeline: The Failure of The Royal Bank of ScotlandFailure of Royal Bank of Scotland (RBS) Risk Management100% (1)