You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Programme Handbook PsychologyDocument19 pagesProgramme Handbook PsychologyEmilyNo ratings yet

- NCR Cup Quiz 1Document7 pagesNCR Cup Quiz 1Lara Lewis AchillesNo ratings yet

- Kieso10eChp09 MidtermDocument30 pagesKieso10eChp09 MidtermJohn FinneyNo ratings yet

- Public Sector Accounting and Administrative Practices in Nigeria Volume 1From EverandPublic Sector Accounting and Administrative Practices in Nigeria Volume 1No ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Mock CompreDocument8 pagesMock CompreRegenLudevese100% (2)

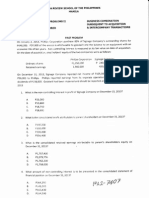

- CPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFDocument5 pagesCPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFAngelo Villadores100% (3)

- PPL CupDocument9 pagesPPL CupErrol John P. SahagunNo ratings yet

- PPL Cup DifficultDocument8 pagesPPL Cup DifficultRukia Kuchiki100% (1)

- 03 PPL CUP Difficult and ClincherDocument5 pages03 PPL CUP Difficult and ClincherDarwin LopezNo ratings yet

- PPL Cup AverageDocument7 pagesPPL Cup AverageRukia KuchikiNo ratings yet

- Loans and Receivables - Long TermDocument3 pagesLoans and Receivables - Long TermAleezaAngelaSanchezNarvadezNo ratings yet

- 2nd Year Reviewer Midterms (Compatibility)Document11 pages2nd Year Reviewer Midterms (Compatibility)Louie De La Torre0% (1)

- 13th NCR Cup Series 7 SGVDocument9 pages13th NCR Cup Series 7 SGVrcaa04No ratings yet

- Quiz BowlDocument3 pagesQuiz BowljayrjoshuavillapandoNo ratings yet

- QUIZ1PRAC1Document23 pagesQUIZ1PRAC1Marinel FelipeNo ratings yet

- QUIZ1PRAC1Document23 pagesQUIZ1PRAC1Marinel Felipe0% (1)

- FarDocument64 pagesFarBrevin PerezNo ratings yet

- Practical Accounting 2 First Pre-Board ExaminationDocument15 pagesPractical Accounting 2 First Pre-Board ExaminationKaren Eloisse89% (9)

- Practical Accounting 1: 2011 National Cpa Mock Board ExaminationDocument7 pagesPractical Accounting 1: 2011 National Cpa Mock Board ExaminationkonyatanNo ratings yet

- Bfjpia Cup 2 - Practical Accounting 1 Easy: Page 1 of 10Document10 pagesBfjpia Cup 2 - Practical Accounting 1 Easy: Page 1 of 10kristelle0marisseNo ratings yet

- NFJPIA Mockboard 2011 P1Document7 pagesNFJPIA Mockboard 2011 P1jhefster_81No ratings yet

- Nfjpia Mockboard 2011 p1 - With AnswersDocument12 pagesNfjpia Mockboard 2011 p1 - With AnswersRhea SamsonNo ratings yet

- Level 1 Questions FinalDocument10 pagesLevel 1 Questions FinalExequielCamisaCrusperoNo ratings yet

- BonusDocument5 pagesBonusbustillos_edwinjrNo ratings yet

- Amount Owed by The Business AccountingDocument3 pagesAmount Owed by The Business Accountingelsana philipNo ratings yet

- The Review Schooj. of AccountancyDocument17 pagesThe Review Schooj. of AccountancyYukiNo ratings yet

- Final Exam Cfas WoDocument11 pagesFinal Exam Cfas WoAndrei GoNo ratings yet

- Ap8501, Ap8502, Ap8503 Audit of ShareholdersDocument21 pagesAp8501, Ap8502, Ap8503 Audit of ShareholdersRits Monte100% (1)

- Practical Accounting TwoDocument25 pagesPractical Accounting TwoJoseph SalidoNo ratings yet

- Compre RevDocument7 pagesCompre RevGellez Hannah MarieNo ratings yet

- Practical Accounting TwoDocument48 pagesPractical Accounting TwoFerdinand FernandoNo ratings yet

- BFJPIA Cup Level 3 P1Document9 pagesBFJPIA Cup Level 3 P1Blessy Zedlav LacbainNo ratings yet

- Integrated Accounting Midterm ExamDocument3 pagesIntegrated Accounting Midterm ExamAuroraNo ratings yet

- Practical Accounting 2: 2011 National Cpa Mock Board ExaminationDocument6 pagesPractical Accounting 2: 2011 National Cpa Mock Board ExaminationMary Queen Ramos-UmoquitNo ratings yet

- Eos CupFinal RoundDocument7 pagesEos CupFinal RoundMJ YaconNo ratings yet

- Accounting For ReceivableDocument2 pagesAccounting For ReceivableJEFFERSON CUTENo ratings yet

- ASSET 2019 Mock Boards - FARDocument7 pagesASSET 2019 Mock Boards - FARKenneth Christian WilburNo ratings yet

- AP AnswerKeyDocument6 pagesAP AnswerKeyRosalie E. Balhag100% (2)

- Toaz - Info Auditing PRDocument22 pagesToaz - Info Auditing PRAlbert pendangNo ratings yet

- Assement Exam-Dysas 1st Quarter-P1Document5 pagesAssement Exam-Dysas 1st Quarter-P1JohnAllenMarillaNo ratings yet

- Prac2 ReviewerDocument12 pagesPrac2 ReviewerRay Jhon Ortiz0% (1)

- Financial Quali - ADocument9 pagesFinancial Quali - ACarl AngeloNo ratings yet

- Practical Accounting 1 Mockboard 2014Document8 pagesPractical Accounting 1 Mockboard 2014Jonathan Tumamao Fernandez100% (1)

- #Test Bank - Finc - L Acctg. 2 - 3 (V)Document34 pages#Test Bank - Finc - L Acctg. 2 - 3 (V)Nhaj100% (1)

- Investment Property and Other InvestmentsDocument4 pagesInvestment Property and Other InvestmentsMiguel MartinezNo ratings yet

- Cfas Fs PreparationDocument3 pagesCfas Fs PreparationEvelina Del RosarioNo ratings yet

- Financial LiabilitiesDocument22 pagesFinancial LiabilitiesPeter Banjao100% (1)

- NFJPIA - Mockboard 2011 - AP PDFDocument6 pagesNFJPIA - Mockboard 2011 - AP PDFSteven Mark MananguNo ratings yet

- 112 Seatwork1 ForStudentsDocument5 pages112 Seatwork1 ForStudentsJoventino NebresNo ratings yet

- Soal GSLC-13 Advanced AccountingDocument7 pagesSoal GSLC-13 Advanced AccountingEunice ShevlinNo ratings yet

- P1 2ND Preboard PDFDocument9 pagesP1 2ND Preboard PDFmaria evangelistaNo ratings yet

- At December 31Document9 pagesAt December 31Josephine MercadoNo ratings yet

- NFJPIA Mockboard 2011 P2Document13 pagesNFJPIA Mockboard 2011 P2Regie Sharry Alutang PanisNo ratings yet

- Republic of The Philippines Department of Education National Capital Region Schools Division of Parañaque CityDocument2 pagesRepublic of The Philippines Department of Education National Capital Region Schools Division of Parañaque CityMaclea NopuenteNo ratings yet

- 21St Century Computer Solutions: A Manual Accounting SimulationFrom Everand21St Century Computer Solutions: A Manual Accounting SimulationNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Kieso 10 e CHP 08Document30 pagesKieso 10 e CHP 08Viet HoangNo ratings yet

- Toa Quizzer 1: Multiple ChoiceDocument18 pagesToa Quizzer 1: Multiple ChoiceRukia KuchikiNo ratings yet

- Toa Quizzer 2: Multiple ChoiceDocument20 pagesToa Quizzer 2: Multiple ChoiceRukia KuchikiNo ratings yet

- InvestmentsDocument44 pagesInvestmentsRukia Kuchiki100% (5)

- Intermediate Acct Test Bankch18Document50 pagesIntermediate Acct Test Bankch18Shuo Jia50% (2)

- CH 12Document50 pagesCH 12drealbevo100% (2)

- SS 513-1-2013 - PreviewDocument9 pagesSS 513-1-2013 - PreviewalexNo ratings yet

- Food Defense Plan: B G A in N N S I A T L Ea Industries Limited / 1 Aug 2022 / KanavDocument4 pagesFood Defense Plan: B G A in N N S I A T L Ea Industries Limited / 1 Aug 2022 / Kanavvaishnavi100% (1)

- Base SuperstructureDocument4 pagesBase SuperstructureDebleena TaNo ratings yet

- Century Properties, Inc. vs. BabianoDocument21 pagesCentury Properties, Inc. vs. BabianoErlaine GalloNo ratings yet

- A Gangster - S Kiss 2Document195 pagesA Gangster - S Kiss 2Brixton StormNo ratings yet

- My DayDocument3 pagesMy DayАлина СамусьNo ratings yet

- General Mathematics (2ND Quarter Exam)Document2 pagesGeneral Mathematics (2ND Quarter Exam)IVY AGUAS100% (1)

- Equipment Interference Code of PracticeDocument147 pagesEquipment Interference Code of PracticeMarkos ArakasNo ratings yet

- RLR - 7 LaxamanaDocument6 pagesRLR - 7 LaxamanaLaxamana, MarcNo ratings yet

- B-39, Hosiery Complex Phase-2 Noida: Over Time Sheet Month of Aug-22Document8 pagesB-39, Hosiery Complex Phase-2 Noida: Over Time Sheet Month of Aug-22id internationalNo ratings yet

- Avangrid Networks vs. Matthew DunlapDocument12 pagesAvangrid Networks vs. Matthew DunlapMaine Trust For Local NewsNo ratings yet

- Historical Roads Preservation GuideDocument86 pagesHistorical Roads Preservation GuideCAP History LibraryNo ratings yet

- Reflection EssayDocument4 pagesReflection Essayapi-384143523No ratings yet

- Worldwide Address ListDocument40 pagesWorldwide Address Listmusaismail8863No ratings yet

- Chapter 5Document13 pagesChapter 5Dhea CahyaNo ratings yet

- Implementation-of-Risk-Management-In-the-Construction-Industry-in-Developing-CountriesDocument22 pagesImplementation-of-Risk-Management-In-the-Construction-Industry-in-Developing-CountriesIsmail A IsmailNo ratings yet

- Cybersecurity Course Quiz With AnswersDocument2 pagesCybersecurity Course Quiz With AnswersTarik AmezianeNo ratings yet

- NYLA Talent Performers Manual 2021 (Talent)Document6 pagesNYLA Talent Performers Manual 2021 (Talent)Jasmine KhasawnehNo ratings yet

- Strategic Planning For Avoidance of Catastrophic Flood ConsequencesDocument10 pagesStrategic Planning For Avoidance of Catastrophic Flood ConsequencesKOPSIDAS ODYSSEASNo ratings yet

- For Individual Citizens and Resident Aliens Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionDocument2 pagesFor Individual Citizens and Resident Aliens Earning Purely Compensation Income and Individuals Engaged in Business and Practice of ProfessionLhyraNo ratings yet

- Agricultural TenancyDocument20 pagesAgricultural TenancyJel LyNo ratings yet

- Emma Jane AustenDocument4 pagesEmma Jane Austen4vrwqrtrd2No ratings yet

- Earned Value Management For Construction Projects PDFDocument1 pageEarned Value Management For Construction Projects PDFHammad AhmedNo ratings yet

- Advincula Vs Macabata (A.C. No. 7204 March 7, 2007)Document2 pagesAdvincula Vs Macabata (A.C. No. 7204 March 7, 2007)Kevin Degamo50% (2)

- Reaction Paper 2Document2 pagesReaction Paper 2BRYAN PIELNo ratings yet

- Earl Johnson v. General Electric, 840 F.2d 132, 1st Cir. (1988)Document11 pagesEarl Johnson v. General Electric, 840 F.2d 132, 1st Cir. (1988)Scribd Government DocsNo ratings yet

- Welsh Premier Times Issue 7Document12 pagesWelsh Premier Times Issue 7Duke AlexandruNo ratings yet

- 厨房助理求职信Document7 pages厨房助理求职信ewaw35mrNo ratings yet

- Learning Task 18Document2 pagesLearning Task 18Marlhen Euge SanicoNo ratings yet