You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Loan Syndication-Structure, Pricing and Deal MakingDocument30 pagesLoan Syndication-Structure, Pricing and Deal Makingjaya100% (7)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Currency SwapDocument7 pagesCurrency SwaprethviNo ratings yet

- FICO Credit ScoreDocument4 pagesFICO Credit ScoreCarol100% (1)

- Mac OS X Security ChecklistDocument8 pagesMac OS X Security ChecklistHomerKhanNo ratings yet

- ENISA-IoT Validation WorkshopDocument29 pagesENISA-IoT Validation WorkshopHomerKhanNo ratings yet

- NIST SP 800-163r1Document55 pagesNIST SP 800-163r1HomerKhanNo ratings yet

- Yahoo Breach LessonsDocument38 pagesYahoo Breach LessonsHomerKhanNo ratings yet

- 03-Cisco Configuration Professional (Lab) : Ahmed SultanDocument1 page03-Cisco Configuration Professional (Lab) : Ahmed SultanHomerKhanNo ratings yet

- YubiKey Manual v3.3Document41 pagesYubiKey Manual v3.3HomerKhanNo ratings yet

- Yum CommandsDocument2 pagesYum Commandsbaraka08No ratings yet

- Cisco Switch Security Configuration GuideDocument86 pagesCisco Switch Security Configuration GuideBen HetrickNo ratings yet

- Sip Security Mechanism:a State-Of-The-Art ReviewDocument9 pagesSip Security Mechanism:a State-Of-The-Art Reviewkoalla01No ratings yet

- Key Management: - How Many Are There? - Who Creates Them? - Where Are They Stored? - EtcDocument4 pagesKey Management: - How Many Are There? - Who Creates Them? - Where Are They Stored? - EtcHomerKhanNo ratings yet

- 2012 08 ComFortePCI White PaperDocument21 pages2012 08 ComFortePCI White PaperHomerKhanNo ratings yet

- 2012 08 ComFortePCI White PaperDocument21 pages2012 08 ComFortePCI White PaperHomerKhanNo ratings yet

- Phishing Resource GuideDocument3 pagesPhishing Resource GuideHomerKhanNo ratings yet

- App Sec and Dev OpsDocument19 pagesApp Sec and Dev OpsHomerKhanNo ratings yet

- Web Security Interview Questions and AnswersDocument8 pagesWeb Security Interview Questions and Answersvenkat1034No ratings yet

- Choose Australian Super Nomination FormDocument1 pageChoose Australian Super Nomination FormHomerKhanNo ratings yet

- Key Management: - How Many Are There? - Who Creates Them? - Where Are They Stored? - EtcDocument4 pagesKey Management: - How Many Are There? - Who Creates Them? - Where Are They Stored? - EtcHomerKhanNo ratings yet

- Mobile Top TenDocument29 pagesMobile Top TenHimanshu SharmaNo ratings yet

- Remote Access VulnerabilitiesDocument3 pagesRemote Access VulnerabilitiesHomerKhanNo ratings yet

- Securing Merchant Terminals Remote Access FINAL 7 July 2015Document16 pagesSecuring Merchant Terminals Remote Access FINAL 7 July 2015HomerKhanNo ratings yet

- CIT2251 CCNA Security SyllabusDocument4 pagesCIT2251 CCNA Security SyllabusHomerKhanNo ratings yet

- 8 Steps To Secure and Harden Cisco RouterDocument6 pages8 Steps To Secure and Harden Cisco RouterchiweekokNo ratings yet

- Iowa State University: Business Impact Analysis and Risk Assessment For Information ResourcesDocument12 pagesIowa State University: Business Impact Analysis and Risk Assessment For Information ResourcesHomerKhanNo ratings yet

- Visa BP SBDocument8 pagesVisa BP SBHomerKhanNo ratings yet

- DSS Clearing and Sanitization MatrixDocument4 pagesDSS Clearing and Sanitization MatrixHomerKhanNo ratings yet

- 8 Steps To Secure and Harden Cisco RouterDocument6 pages8 Steps To Secure and Harden Cisco RouterchiweekokNo ratings yet

- PCI DSS 3.1 Impact On WiFi Security PDFDocument7 pagesPCI DSS 3.1 Impact On WiFi Security PDFHomerKhanNo ratings yet

- Cloud Computing PolicyDocument8 pagesCloud Computing PolicyHomerKhanNo ratings yet

- Journalizing, Posting and BalancingDocument21 pagesJournalizing, Posting and Balancinganuradha100% (1)

- Money market rolesDocument2 pagesMoney market rolesAilaJeanineNo ratings yet

- SExam2 PDFDocument4 pagesSExam2 PDFdicheyaNo ratings yet

- Credit Creation by Commercial BanksDocument19 pagesCredit Creation by Commercial BanksSaumitra RaneNo ratings yet

- Idbi BankDocument1 pageIdbi BankSakinah SNo ratings yet

- N I Act 1881Document42 pagesN I Act 1881Hemendra GuptaNo ratings yet

- PDFDocument8 pagesPDFEmanuelNo ratings yet

- Kotak Mahindra Bank 121121123739 Phpapp02Document112 pagesKotak Mahindra Bank 121121123739 Phpapp02RahulSinghNo ratings yet

- Lahore School of Economics Financial Management I Time Value of Money - 3 Assignment 4Document2 pagesLahore School of Economics Financial Management I Time Value of Money - 3 Assignment 4Ahmed ZafarNo ratings yet

- Simple AnnuityDocument2 pagesSimple AnnuityArden AnagapNo ratings yet

- Chime Bank Statement NirtDocument3 pagesChime Bank Statement Nirtfehijan689No ratings yet

- Data Analysis On Financial InclusionDocument21 pagesData Analysis On Financial InclusionHeidi Bell50% (2)

- A Study On 269SS & 269 TDocument4 pagesA Study On 269SS & 269 TsivaranjanNo ratings yet

- University Faisalabad Cash Account Engineering Wing Student Fees Challan 1484238Document1 pageUniversity Faisalabad Cash Account Engineering Wing Student Fees Challan 1484238Abdullah HaiderNo ratings yet

- Detailed StatementDocument33 pagesDetailed Statementwolf8585.inNo ratings yet

- Foreign Currency Deposits: R.A 6426, SEC 8Document38 pagesForeign Currency Deposits: R.A 6426, SEC 8Israel BandonillNo ratings yet

- Capic Hexagon - MCRDocument34 pagesCapic Hexagon - MCROlufemi MoyegunNo ratings yet

- Monetary Policy Framework in The PhilippinesDocument3 pagesMonetary Policy Framework in The PhilippinesRhenaNo ratings yet

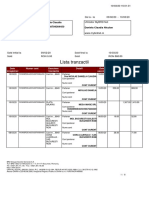

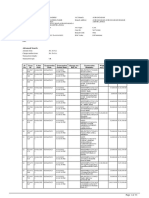

- Transacti On Date & Time Transacti On ID Internal Transacti On ID Journal No Debit Mobile/E Nterprise ID Debit CBS Account No Debit Account Name Debit CircleDocument3 pagesTransacti On Date & Time Transacti On ID Internal Transacti On ID Journal No Debit Mobile/E Nterprise ID Debit CBS Account No Debit Account Name Debit CirclePratik BansodeNo ratings yet

- 213-C-46295-Assignment Acc Xi BrsDocument7 pages213-C-46295-Assignment Acc Xi BrsMannatNo ratings yet

- Affidavit Details Loan DefaultDocument3 pagesAffidavit Details Loan DefaultAnn SCNo ratings yet

- Banking Awareness Hand Book by Er. G C Nayak PDFDocument86 pagesBanking Awareness Hand Book by Er. G C Nayak PDFTapas Kumar NandiNo ratings yet

- Chapter 18Document29 pagesChapter 18UsmanNo ratings yet

- Ebesun Co4Document8 pagesEbesun Co4Chidinma NnoliNo ratings yet

- Money and Monetary StandardsDocument40 pagesMoney and Monetary StandardsZenedel De JesusNo ratings yet

- Renaissance University, Indore Proforma of First Page of PresentationsDocument7 pagesRenaissance University, Indore Proforma of First Page of PresentationsMudit MaheshwariNo ratings yet

- Federal Reserve Consumer Credit-G.19Document3 pagesFederal Reserve Consumer Credit-G.19Jackson SinnenbergNo ratings yet