You might also like

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Lady M Confections case discussion questions and valuation analysisDocument11 pagesLady M Confections case discussion questions and valuation analysisRahul Sinha40% (10)

- The Valuation and Financing of Lady M Case StudyDocument4 pagesThe Valuation and Financing of Lady M Case StudyUry Suryanti Rahayu100% (3)

- The Valuation and Financing of Lady M Confections: 23600 Cash BEP 1888000,00Document4 pagesThe Valuation and Financing of Lady M Confections: 23600 Cash BEP 1888000,00Rahul VenugopalanNo ratings yet

- Fixed cost analysis and break even calculation with sales growth projectionsDocument8 pagesFixed cost analysis and break even calculation with sales growth projectionsEvelyn MonzonNo ratings yet

- Lady M SolutionDocument4 pagesLady M SolutionRahul VenugopalanNo ratings yet

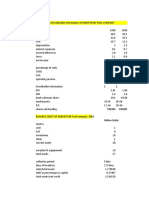

- Book1Document6 pagesBook1Bharti SutharNo ratings yet

- Lady MDocument2 pagesLady MMəhəmməd Əli HəzizadəNo ratings yet

- Valuation of Lady M Case Questions PDFDocument3 pagesValuation of Lady M Case Questions PDFJane Susan Thomas25% (4)

- Lady M Confections - v3Document29 pagesLady M Confections - v3Shamsuzzaman Sun75% (4)

- Robert Reid Lady M Confections SubmissionDocument13 pagesRobert Reid Lady M Confections SubmissionSam Nderitu100% (1)

- Unit 2 Case Study Guidelines - Lady M Confections Revised 10.4.18Document11 pagesUnit 2 Case Study Guidelines - Lady M Confections Revised 10.4.18Neel PatelNo ratings yet

- Lady M Case - 08.07.2016Document14 pagesLady M Case - 08.07.2016Sabyasachi Mukerji40% (5)

- Solucion Caso Lady MDocument13 pagesSolucion Caso Lady Mjohana irma ore pizarroNo ratings yet

- Lady M DCF TemplateDocument4 pagesLady M DCF Templatednesudhudh100% (1)

- Pros and Cons of Operating LeverageDocument3 pagesPros and Cons of Operating LeverageAntonius CliffSetiawanNo ratings yet

- The Valuation and Financing of Lady M. Confections PDFDocument1 pageThe Valuation and Financing of Lady M. Confections PDFHasbi AsidikNo ratings yet

- Air Thread ReportDocument13 pagesAir Thread ReportDHRUV SONAGARA100% (2)

- New Heritage DollDocument26 pagesNew Heritage DollJITESH GUPTANo ratings yet

- Airthread Connections NidaDocument15 pagesAirthread Connections NidaNidaParveen100% (1)

- AirThread G015Document6 pagesAirThread G015sahildharhakim83% (6)

- New DollDocument2 pagesNew DollJuyt HertNo ratings yet

- Merck Evaluates Drug Licensing OpportunityDocument29 pagesMerck Evaluates Drug Licensing OpportunityAbinash Behera60% (5)

- MIdland FInalDocument7 pagesMIdland FInalFarida100% (8)

- Nike Case Final Group 4Document15 pagesNike Case Final Group 4Monika Maheshwari100% (1)

- Airthread DCF Vs ApvDocument6 pagesAirthread DCF Vs Apvapi-239586293No ratings yet

- AirThread ConnectionDocument26 pagesAirThread ConnectionAnandNo ratings yet

- Ocean CarriersDocument17 pagesOcean CarriersMridula Hari33% (3)

- Dell's Working Capital - Case Analysis - G05Document2 pagesDell's Working Capital - Case Analysis - G05Srikanth Kumar Konduri100% (11)

- Case 34 - The Wm. Wrigley Jr. CompanyDocument72 pagesCase 34 - The Wm. Wrigley Jr. CompanyQUYNH100% (1)

- The Financial Detective CaseDocument6 pagesThe Financial Detective Caseashwini patilNo ratings yet

- Arcadian Microarray TechnologiesDocument20 pagesArcadian Microarray Technologies0407199050% (2)

- Sampa Video Home Delivery ProjectDocument26 pagesSampa Video Home Delivery ProjectFaradilla Karnesia100% (2)

- Marriott Corporation - K - AbridgedDocument9 pagesMarriott Corporation - K - AbridgedDurgaprasad Velamala100% (5)

- Monmouth Inc SolutionDocument9 pagesMonmouth Inc SolutionPedro José ZapataNo ratings yet

- Dell's Working CapitalDocument20 pagesDell's Working Capitalapi-371968795% (21)

- PPTXDocument8 pagesPPTXWriters Wing100% (2)

- Tire City Spreadsheet SolutionDocument6 pagesTire City Spreadsheet Solutionalmasy99100% (1)

- AirThread Valuation MethodsDocument21 pagesAirThread Valuation MethodsSon NguyenNo ratings yet

- Pacific Grove Spice Company Case Write UpDocument3 pagesPacific Grove Spice Company Case Write UpVaishnavi Gnanasekaran100% (4)

- New Heritage Doll CompanDocument9 pagesNew Heritage Doll CompanArima ChatterjeeNo ratings yet

- Nike CaseDocument7 pagesNike CaseNindy Darista100% (1)

- Average EV/Sales, EV/EBITDA and P/E Ratios for Automotive CompaniesDocument6 pagesAverage EV/Sales, EV/EBITDA and P/E Ratios for Automotive CompaniesAhmed NiazNo ratings yet

- Carter's LBO CaseDocument3 pagesCarter's LBO CaseNoah57% (7)

- Case AnalysisDocument11 pagesCase AnalysisSagar Bansal50% (2)

- TCI's Financial Performance and Forecasts 1993-1997Document8 pagesTCI's Financial Performance and Forecasts 1993-1997Kyeli TanNo ratings yet

- Ocean Carries HBS Case StudyDocument4 pagesOcean Carries HBS Case StudyRatul EsrarNo ratings yet

- Case 8 - Diamond DCF ModelDocument2 pagesCase 8 - Diamond DCF ModelAudrey AngNo ratings yet

- Pacific Grove Spice CompanyDocument7 pagesPacific Grove Spice CompanySajjad Ahmad100% (1)

- Outreach Networks Case Study SolutionDocument2 pagesOutreach Networks Case Study SolutionEaston Griffin0% (1)

- Eastboro Case SolutionDocument22 pagesEastboro Case Solutionuddindjm100% (2)

- Monmouth Case SolutionDocument19 pagesMonmouth Case Solutiondave25% (4)

- Safari 3Document4 pagesSafari 3Bharti SutharNo ratings yet

- John M CaseDocument10 pagesJohn M Caseadrian_simm100% (1)

- Icm 0785Document12 pagesIcm 0785Dêvâl Pãtěl100% (3)

- Multiplex ProjectionsDocument2 pagesMultiplex ProjectionsTheHackersdenNo ratings yet

- Boston Beer ExcelDocument6 pagesBoston Beer ExcelNarinderNo ratings yet

- Projected Financials and Valuation of a Pharmaceutical CompanyDocument14 pagesProjected Financials and Valuation of a Pharmaceutical Companyvardhan100% (1)

- End Term Examination Corporate Restructuring and Business Valuation TERM IV, PGP, 2020 Name - Puneet Garg Roll No - 19P101Document7 pagesEnd Term Examination Corporate Restructuring and Business Valuation TERM IV, PGP, 2020 Name - Puneet Garg Roll No - 19P101Puneet GargNo ratings yet

- Sales Expected To Increase by 8%Document11 pagesSales Expected To Increase by 8%WiSeVirGoNo ratings yet

- 14 - Chapter 3Document79 pages14 - Chapter 3monuNo ratings yet

- Lipura Ts Module8EntrepDocument7 pagesLipura Ts Module8EntrepPrincess Enrian Quintana PolinarNo ratings yet

- MarketingResearch Ch1 IntroductionDocument34 pagesMarketingResearch Ch1 IntroductionTanvir Ahmad ShourovNo ratings yet

- Group2 Batch2 Spencer Retail LTDDocument6 pagesGroup2 Batch2 Spencer Retail LTDsambhav jainNo ratings yet

- Market Segmentation WorksheetDocument3 pagesMarket Segmentation WorksheetAmelia TaylorNo ratings yet

- Schwab One Account AgreementDocument112 pagesSchwab One Account AgreementcadeadmanNo ratings yet

- Wholesaler of Glow Sticks Offers Bulk DealsDocument3 pagesWholesaler of Glow Sticks Offers Bulk DealsfaryalNo ratings yet

- InvoiceDocument1 pageInvoicePrithu SinghNo ratings yet

- Amazon vs Flipkart Ratio Analysis Group 03Document14 pagesAmazon vs Flipkart Ratio Analysis Group 03Srishti JoshiNo ratings yet

- Assessing Marketing Channel PerformanceDocument14 pagesAssessing Marketing Channel PerformanceRavi GuptaNo ratings yet

- Petrobras Case StudyDocument13 pagesPetrobras Case Studykid.hahnNo ratings yet

- Innovative Financial ServicesDocument9 pagesInnovative Financial ServicesShubham GuptaNo ratings yet

- Dale EA DescriptionDocument5 pagesDale EA Descriptionbilly linggNo ratings yet

- MetaTrader 5 Tutorial For Beginners + PDF Guide - EA Trading AcademyDocument20 pagesMetaTrader 5 Tutorial For Beginners + PDF Guide - EA Trading AcademyBhuvaneshwaran BN100% (2)

- Relevant Market of Big Basket, Netfliex, PaytmDocument2 pagesRelevant Market of Big Basket, Netfliex, PaytmSparsh AgrawalNo ratings yet

- Trade Finance Products PDFDocument34 pagesTrade Finance Products PDFNurulhikmah RoslanNo ratings yet

- Financial Crisis of 2000sDocument180 pagesFinancial Crisis of 2000sIvan M100% (1)

- LNG Export Diversification and Demand Security A Comparative Study of Major ExportersDocument9 pagesLNG Export Diversification and Demand Security A Comparative Study of Major ExportersMypc PersonalNo ratings yet

- IPO and Cost of Venture CapitalistsDocument41 pagesIPO and Cost of Venture CapitalistsJa takNo ratings yet

- MAFA Notes Old SyllabusDocument61 pagesMAFA Notes Old SyllabusDeep JoshiNo ratings yet

- CRM Modules Erp SystemDocument4 pagesCRM Modules Erp SystemSaleemAhmedNo ratings yet

- Footwear Trading: Patterns and PracticeDocument30 pagesFootwear Trading: Patterns and PracticeumidgrtNo ratings yet

- Principles Marketing Group 2 2 1Document19 pagesPrinciples Marketing Group 2 2 1bé Đức 4 tuổiNo ratings yet

- asset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewDocument42 pagesasset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewBURUNDI1No ratings yet

- Faq's For F &aDocument17 pagesFaq's For F &amcaviimsNo ratings yet

- Otieno - The Value Chain Analysis in Telkom Kenya PDFDocument54 pagesOtieno - The Value Chain Analysis in Telkom Kenya PDFzaid Al ZoubiNo ratings yet

- Accounting Firm Marketing PlanDocument49 pagesAccounting Firm Marketing PlanPalo Alto Software100% (9)

- Environmental RegulationsDocument18 pagesEnvironmental RegulationsRAHULNo ratings yet

- PMIRDocument124 pagesPMIRhashvishuNo ratings yet

- Bajaj Holdings Investment 24042019Document3 pagesBajaj Holdings Investment 24042019anjugaduNo ratings yet