You might also like

- Statutory Construction Reviewer For MidtermsDocument6 pagesStatutory Construction Reviewer For MidtermsDanJalbuna100% (2)

- Silicon Philippines vs. Cir DigestDocument1 pageSilicon Philippines vs. Cir DigestAnny YanongNo ratings yet

- Team Sual Corporation v. CIRDocument2 pagesTeam Sual Corporation v. CIRAlyk Tumayan Calion100% (1)

- China Banking Corporation vs. CADocument1 pageChina Banking Corporation vs. CAArmstrong BosantogNo ratings yet

- Geronimo v. SantosDocument3 pagesGeronimo v. SantosDanJalbuna100% (2)

- People v. EstoniloDocument3 pagesPeople v. EstoniloDanJalbuna100% (1)

- AC4251 Group Project Written ReportDocument24 pagesAC4251 Group Project Written ReportranniamokNo ratings yet

- G.R. No. 207112 Case DigestDocument3 pagesG.R. No. 207112 Case DigestAlvin Earl NuydaNo ratings yet

- CIR vs. Goodyear Philippines, Inc. GR No. 216130, 3 August 2016Document2 pagesCIR vs. Goodyear Philippines, Inc. GR No. 216130, 3 August 2016nnn aaaNo ratings yet

- CIR V Pilipinas ShellDocument4 pagesCIR V Pilipinas ShellCedric Enriquez100% (2)

- Bonifacio Water Corp V CIR. Case DigestDocument2 pagesBonifacio Water Corp V CIR. Case DigestIan Jala CalmaresNo ratings yet

- 10 CIR Vs Lancaster Case DigestDocument1 page10 CIR Vs Lancaster Case DigestAllanNo ratings yet

- Case Digest of CIR v. Aichi ForgingDocument4 pagesCase Digest of CIR v. Aichi ForgingJeng Pion100% (1)

- Angeles V AngelesDocument3 pagesAngeles V AngelesMarife MinorNo ratings yet

- CIR vs. Burmeister 153205Document1 pageCIR vs. Burmeister 153205magenNo ratings yet

- Samar-I Electric Cooperative vs. CirDocument2 pagesSamar-I Electric Cooperative vs. CirRaquel DoqueniaNo ratings yet

- CIR V StanleyDocument15 pagesCIR V StanleyPatatas SayoteNo ratings yet

- Metrobank V CIRDocument2 pagesMetrobank V CIRReena MaNo ratings yet

- Income Tax DigestsDocument6 pagesIncome Tax Digestsada mae santoniaNo ratings yet

- 7.6. O San Agustin V CIRDocument3 pages7.6. O San Agustin V CIRshenayeeNo ratings yet

- 10 OCEANIC WIRELESS NETWORK Vs CIRDocument3 pages10 OCEANIC WIRELESS NETWORK Vs CIRIsh100% (1)

- Rhombus Energy, Inc. vs. Commissioner of Internal Revenue DigestDocument2 pagesRhombus Energy, Inc. vs. Commissioner of Internal Revenue DigestEmir Mendoza100% (1)

- Fitness by Design, Inc. v. CIR Case DigestDocument3 pagesFitness by Design, Inc. v. CIR Case DigestCareenNo ratings yet

- CIR v. CitytrustDocument2 pagesCIR v. Citytrustpawchan02No ratings yet

- Case Digest #3 - CIR Vs - Mirant PagbilaoDocument3 pagesCase Digest #3 - CIR Vs - Mirant PagbilaoMark AmistosoNo ratings yet

- Steag State Power, Inc. v. Commissioner of Internal Revenue, G.R. No. 205282, January 14, 2019 (Third Division)Document1 pageSteag State Power, Inc. v. Commissioner of Internal Revenue, G.R. No. 205282, January 14, 2019 (Third Division)John Kenneth JacintoNo ratings yet

- CONTEXT CORP. v. CIR - DigestDocument2 pagesCONTEXT CORP. v. CIR - DigestMark Genesis RojasNo ratings yet

- Case Digest of GR No 153204Document1 pageCase Digest of GR No 153204Ivan ChuaNo ratings yet

- Cir vs. Pascor Realty and Development CorporationDocument2 pagesCir vs. Pascor Realty and Development Corporationmaki Amancio100% (1)

- Adamson vs. Court of Appeals 2009Document3 pagesAdamson vs. Court of Appeals 2009joyce100% (1)

- Advertising Associates vs. CADocument2 pagesAdvertising Associates vs. CAJyrnaRhea80% (5)

- Abakada Guro Vs ErmitaDocument1 pageAbakada Guro Vs Ermitaapril75No ratings yet

- Antam Pawnshop Corp. vs. CIRDocument1 pageAntam Pawnshop Corp. vs. CIRPaolo AdalemNo ratings yet

- Rizal Commercial Banking vs. CIRDocument3 pagesRizal Commercial Banking vs. CIRMarife MinorNo ratings yet

- Republic V Salud HIzonDocument2 pagesRepublic V Salud HIzonPJ Hong100% (1)

- ETPI Vs CIRDocument2 pagesETPI Vs CIRSophiaFrancescaEspinosaNo ratings yet

- CIR Vs Seagate, GR 153866Document3 pagesCIR Vs Seagate, GR 153866Mar Develos100% (1)

- CIR Vs General Foods DigestDocument3 pagesCIR Vs General Foods DigestGil Aldrick FernandezNo ratings yet

- CIR Vs Cebu Toyo CorporationDocument2 pagesCIR Vs Cebu Toyo Corporationjancelmido1100% (2)

- CIR Vs Standard CharteredDocument2 pagesCIR Vs Standard CharteredFatzie MendozaNo ratings yet

- In Case of Denial of Protest: Referral To Solgen For CollectionDocument2 pagesIn Case of Denial of Protest: Referral To Solgen For Collectionkim_santos_20100% (1)

- CIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Document2 pagesCIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Digna LausNo ratings yet

- CIR v. Cadiz Sugar FarmersDocument6 pagesCIR v. Cadiz Sugar Farmersamareia yap100% (1)

- Cir v. Acesite DigestDocument3 pagesCir v. Acesite DigestkathrynmaydevezaNo ratings yet

- DIGEST - BPI Vs CIR 2005Document2 pagesDIGEST - BPI Vs CIR 2005Mocha BearNo ratings yet

- RCBC V CirDocument4 pagesRCBC V CirleighsiazonNo ratings yet

- CIR Vs Sony PhilippinesDocument1 pageCIR Vs Sony PhilippinesLouie SalladorNo ratings yet

- 1smied Vs CirDocument2 pages1smied Vs CirBam BathanNo ratings yet

- My Digest - CIR vs. Pascor Realty, GR 128315Document4 pagesMy Digest - CIR vs. Pascor Realty, GR 128315Guiller MagsumbolNo ratings yet

- Adamson vs. CADocument2 pagesAdamson vs. CAAices Salvador100% (2)

- G.R. No. 104151 March 10, 1995 - Cir Vs Atlas Mining DigestDocument1 pageG.R. No. 104151 March 10, 1995 - Cir Vs Atlas Mining DigestRichel Dean Solis100% (1)

- CIR vs. Standard Insurance: SummaryDocument4 pagesCIR vs. Standard Insurance: SummaryIshNo ratings yet

- Kepco Vs CIRDocument3 pagesKepco Vs CIRLizzette Dela PenaNo ratings yet

- CIR vs. Placer DomeDocument4 pagesCIR vs. Placer DomeAngelo Castillo100% (1)

- American Express International v. CIR CTA Case No. 6099 (April 19, 2002)Document2 pagesAmerican Express International v. CIR CTA Case No. 6099 (April 19, 2002)Francis Xavier Sinon100% (1)

- Kepco Vs CIR Case DigestDocument2 pagesKepco Vs CIR Case DigestFrancisca Paredes100% (1)

- Microsoft Vs CIRDocument1 pageMicrosoft Vs CIRKaren Mae ServanNo ratings yet

- RCBC V CIRDocument2 pagesRCBC V CIRPJ Hong100% (1)

- Panasonic Imaging Corp. Vs CIRDocument1 pagePanasonic Imaging Corp. Vs CIRbrendamanganaanNo ratings yet

- Bpi V Cir DigestDocument3 pagesBpi V Cir DigestkathrynmaydevezaNo ratings yet

- 02 Philippine Dream Company Inc. vs. CIRDocument13 pages02 Philippine Dream Company Inc. vs. CIREnma KozatoNo ratings yet

- Jardine Davies Insurance Brokers vs. AliposaDocument2 pagesJardine Davies Insurance Brokers vs. AliposaCarlota Nicolas Villaroman100% (1)

- 106 Pilipinas Total Gas Vs CIRDocument3 pages106 Pilipinas Total Gas Vs CIRPia100% (1)

- 36 - PILIPINAS TOTAL GAS vs. CIRDocument2 pages36 - PILIPINAS TOTAL GAS vs. CIRLEIGH TARITZ GANANCIALNo ratings yet

- Republic vs. Spouses RegultoDocument8 pagesRepublic vs. Spouses RegultoDanJalbunaNo ratings yet

- Republic vs. Spouses RegultoDocument8 pagesRepublic vs. Spouses RegultoDanJalbunaNo ratings yet

- Demand Letter For SupportDocument2 pagesDemand Letter For SupportDanJalbuna100% (5)

- People v. SamsonDocument2 pagesPeople v. SamsonDanJalbuna0% (1)

- People v. HidalgoDocument2 pagesPeople v. HidalgoDanJalbunaNo ratings yet

- People v. Frankie GuereroDocument2 pagesPeople v. Frankie GuereroDanJalbunaNo ratings yet

- People v. Barberan (Digest)Document3 pagesPeople v. Barberan (Digest)DanJalbunaNo ratings yet

- People v. AsamuddinDocument3 pagesPeople v. AsamuddinDanJalbunaNo ratings yet

- Cabas v. SususcoDocument3 pagesCabas v. SususcoDanJalbuna0% (1)

- Corporate Code of The PhilippinesDocument11 pagesCorporate Code of The PhilippinesDanJalbunaNo ratings yet

- Filinvest v. Century Iron WorksDocument3 pagesFilinvest v. Century Iron WorksDanJalbunaNo ratings yet

- ASB Realty v. Ortigas & Co. LTDDocument3 pagesASB Realty v. Ortigas & Co. LTDDanJalbunaNo ratings yet

- A New World To Worry AboutDocument6 pagesA New World To Worry AboutDanJalbunaNo ratings yet

- Land, Titles and DeedsDocument4 pagesLand, Titles and DeedsDanJalbunaNo ratings yet

- Fallen 44Document6 pagesFallen 44DanJalbuna100% (1)

- Digests For Cases On AppealDocument12 pagesDigests For Cases On AppealDanJalbunaNo ratings yet

- Ac 3103Document2 pagesAc 3103Lance UrichNo ratings yet

- Chamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesDocument30 pagesChamika's Style: Hairstylist: Braids, Twist, Cornrows, Those Type of Hair StylesUmarNo ratings yet

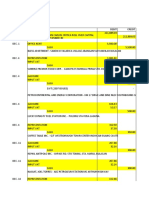

- 12linsteel Book of Account DecemberDocument54 pages12linsteel Book of Account DecemberCarlos_CriticaNo ratings yet

- Short Notes On Public FinanceDocument3 pagesShort Notes On Public FinanceJakir_bnkNo ratings yet

- VATable Transaction Practice PDFDocument2 pagesVATable Transaction Practice PDFJester LimNo ratings yet

- 13 - Tax Law - Customs Law - 271219Document25 pages13 - Tax Law - Customs Law - 271219Sushil BansalNo ratings yet

- Ongc ETP AnkleshwarDocument174 pagesOngc ETP Ankleshwarprocesspipingdesign100% (1)

- TenderDocument PDFDocument44 pagesTenderDocument PDFpmcmbharat264No ratings yet

- GST RCM 010419Document5 pagesGST RCM 010419DilipNo ratings yet

- For Educational Purposes Only Don'T Sell!! Test Bank - Bus. & Trans. TXDocument38 pagesFor Educational Purposes Only Don'T Sell!! Test Bank - Bus. & Trans. TX?????No ratings yet

- Bitumen Price List Wef 16-05-2014Document5 pagesBitumen Price List Wef 16-05-2014Srinivas Nayakuni50% (2)

- E-Arşiv Fatura: Page 1 / 1Document1 pageE-Arşiv Fatura: Page 1 / 1waelzaki077No ratings yet

- Invitation For Annual Maintenance Contract For Tescan SEM VEGA WITH OXFORD EDS UNIT (Proprietary Item)Document11 pagesInvitation For Annual Maintenance Contract For Tescan SEM VEGA WITH OXFORD EDS UNIT (Proprietary Item)Dean GeorgeNo ratings yet

- Invoice Samsung SoundBarDocument1 pageInvoice Samsung SoundBardumtakaNo ratings yet

- BH027242 BTEC HNCD Hospitality Management Units Issue2Document243 pagesBH027242 BTEC HNCD Hospitality Management Units Issue2Pawan CoomarNo ratings yet

- Revised Tax Position Paper ENGDocument8 pagesRevised Tax Position Paper ENGPedro Dias da SilvaNo ratings yet

- House No.-C-8/408, Sultan Puri, New Delhi-110086 +91-9968553555Document3 pagesHouse No.-C-8/408, Sultan Puri, New Delhi-110086 +91-9968553555The Cultural CommitteeNo ratings yet

- Kieso Ifrs2e SM Ch13Document84 pagesKieso Ifrs2e SM Ch13christianoNo ratings yet

- Open SyllabusDocument15 pagesOpen Syllabusanshu sharmaNo ratings yet

- Quiz I General Principles of TaxationDocument3 pagesQuiz I General Principles of Taxationkristian datinguinooNo ratings yet

- DSIR Blog - All About RND Tax Benefits and Incentives in India PDFDocument17 pagesDSIR Blog - All About RND Tax Benefits and Incentives in India PDFsgdsjNo ratings yet

- Vivafit Fitness Business PlanDocument11 pagesVivafit Fitness Business PlanJon CamilleriNo ratings yet

- Questions On Computation of Net GST PayableDocument24 pagesQuestions On Computation of Net GST PayablesneakyblackskullNo ratings yet

- MCQpublicDocument16 pagesMCQpublicShalini Singh IPSANo ratings yet

- All About GST REFUNDS - Refrence ManualDocument451 pagesAll About GST REFUNDS - Refrence ManualSwarnadevi GanesanNo ratings yet

- 11.EBS R12.1 AR Tax Processing Oracle EBSDocument23 pages11.EBS R12.1 AR Tax Processing Oracle EBSANUPNo ratings yet

- CV Fifa Jaya Sport - Memorial JournalDocument6 pagesCV Fifa Jaya Sport - Memorial JournalMiskaNo ratings yet

- GST Complier Ca InterDocument84 pagesGST Complier Ca InterMansi Nayyar0% (1)

- An Evolution of Tax Payers Perception On The Value Added Tax in NigeriaDocument8 pagesAn Evolution of Tax Payers Perception On The Value Added Tax in NigeriaBlessine BlessineNo ratings yet