You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Job AnalysisDocument5 pagesJob AnalysisEMMANUELNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- HCOB 2103 Course Outline Co-Operative PhilosophyDocument3 pagesHCOB 2103 Course Outline Co-Operative PhilosophyEMMANUEL100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- HCOB 2103 Course Outline Co-Operative PhilosophyDocument3 pagesHCOB 2103 Course Outline Co-Operative PhilosophyEMMANUELNo ratings yet

- Report BevDocument28 pagesReport BevEMMANUEL100% (2)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Participant Material 8.2.4.1A: Cash Receipts Scots Form: 1. Obtain An Understanding of The Scot 1.1 Automated TechniquesDocument9 pagesParticipant Material 8.2.4.1A: Cash Receipts Scots Form: 1. Obtain An Understanding of The Scot 1.1 Automated TechniquesHaley TranNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- LANDBANK Gatdula Majorie D.Document8 pagesLANDBANK Gatdula Majorie D.Vince CedricNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- TIde Merchant Onbaording TrainingDocument49 pagesTIde Merchant Onbaording TrainingMeenakshi RaminaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- E - Banking in IndiaDocument23 pagesE - Banking in Indiaaviran_profNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- ADCB WBG TCs English Sep2017 - tcm9 103698Document70 pagesADCB WBG TCs English Sep2017 - tcm9 103698Pulsara RajarathneNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Moya, UgandaDocument17 pagesMoya, UgandaBenjamin Agyeman-Duah OtiNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Mattewos KinfeDocument70 pagesMattewos Kinfechuchu100% (2)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Ifs Cat 2Document16 pagesIfs Cat 2sureshNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Research Report (Abhinav Thakur)Document49 pagesResearch Report (Abhinav Thakur)RAVÉNNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- LUMS Sports VouchersDocument1 pageLUMS Sports VouchersOmer ZahidNo ratings yet

- Customer Satisfaction Towards Online Banking (A Study On Dinajpur City)Document102 pagesCustomer Satisfaction Towards Online Banking (A Study On Dinajpur City)Nokib Ahammed0% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Proposal Final Edited FinalDocument22 pagesProposal Final Edited FinalNyakoojo simonNo ratings yet

- A Project On Banking SectorDocument81 pagesA Project On Banking SectorAkbar SinghNo ratings yet

- The Rise of Customer-Oriented BankingDocument13 pagesThe Rise of Customer-Oriented BankingoussamaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A HandBook On Finacle Work Flow Process 1st EditionDocument79 pagesA HandBook On Finacle Work Flow Process 1st EditionShekhar Suman100% (2)

- Wells Fargo BankDocument10 pagesWells Fargo BankVandana RellanNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

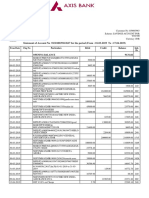

- Bank Statement 2019Document2 pagesBank Statement 2019Vivek AroraNo ratings yet

- Kisi Bing (Aat)Document22 pagesKisi Bing (Aat)Swesty ParamithaNo ratings yet

- PSB OnlineDocument3 pagesPSB Onlinesubhi deNo ratings yet

- Electronic Banking: Tele-Banking: Tele-Banking Service Is Provided by Phone. To Access An Account It IsDocument10 pagesElectronic Banking: Tele-Banking: Tele-Banking Service Is Provided by Phone. To Access An Account It IsFahimKhanDeepNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Milestones in The Journey For Nation BuildingDocument5 pagesMilestones in The Journey For Nation BuildingkapilbakhruNo ratings yet

- M&B Tutorial 1Document4 pagesM&B Tutorial 1Tamy SengNo ratings yet

- ProjectProposal 2013682 Dec21Document2 pagesProjectProposal 2013682 Dec21Hasibul HasanNo ratings yet

- A Report ON "Digitalization and Acquisitions Of: HDFC Bank"Document40 pagesA Report ON "Digitalization and Acquisitions Of: HDFC Bank"Sambhavi SinghNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Financial Capability and Digital Adoption For Online ShoppingDocument8 pagesFinancial Capability and Digital Adoption For Online ShoppingRoldan AzueloNo ratings yet

- ACC 121 - Chapter 2Document15 pagesACC 121 - Chapter 2Rose Ann LazatinNo ratings yet

- The Impact of The Internet Upon Bank MarketingDocument17 pagesThe Impact of The Internet Upon Bank MarketingEman MostafaNo ratings yet

- SURVEY QUESTIONNAIRE - Online BankingDocument4 pagesSURVEY QUESTIONNAIRE - Online BankingEstrada, Jemuel A.No ratings yet

- Chapter 5Document33 pagesChapter 5Praveen VijayNo ratings yet

- Commerce 1 GRD 12 ProjectDocument12 pagesCommerce 1 GRD 12 ProjectNeriaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)