You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Group10 SecC HRMDocument8 pagesGroup10 SecC HRMBollapragada Sai SravanthiNo ratings yet

- Manh Manhattan Active Warehouse Management Mawm Level 1 en PDFDocument2 pagesManh Manhattan Active Warehouse Management Mawm Level 1 en PDFpunitha_pNo ratings yet

- Marketing Strategies of Jhonson and JhonsonDocument32 pagesMarketing Strategies of Jhonson and JhonsonRanjeet Rajput50% (2)

- Quarter 4 Entrep Handout 2 With WW PTDocument5 pagesQuarter 4 Entrep Handout 2 With WW PTRodalyn Pang-ot100% (1)

- BASIC MARKETING: A Marketing Strategy Planning Approach by JR., William Perreault, Joseph Cannon and E. Jerome McCarthy - 19e, TEST BANK 0078028981Document141 pagesBASIC MARKETING: A Marketing Strategy Planning Approach by JR., William Perreault, Joseph Cannon and E. Jerome McCarthy - 19e, TEST BANK 0078028981jksnmmmNo ratings yet

- Introduction To ValuationDocument5 pagesIntroduction To ValuationRG VergaraNo ratings yet

- Bus E-Ticket PNR-3258892-TS191127211416801004IKXEDocument1 pageBus E-Ticket PNR-3258892-TS191127211416801004IKXEDiwakar GurramNo ratings yet

- MELISSA HERMANN (Formerly Peck) : (315) 391-5188 ObjectiveDocument2 pagesMELISSA HERMANN (Formerly Peck) : (315) 391-5188 ObjectiveluckyNo ratings yet

- AS 17 Segment Reporting - Objective Type Question PDFDocument44 pagesAS 17 Segment Reporting - Objective Type Question PDFrsivaramaNo ratings yet

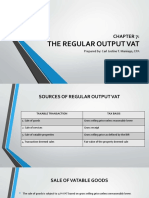

- Lecture Chapter 7 The Regular Output VatDocument17 pagesLecture Chapter 7 The Regular Output VatChristian PelimcoNo ratings yet

- Goodwill & PSR Final Revision SPCCDocument43 pagesGoodwill & PSR Final Revision SPCCHeer SirwaniNo ratings yet

- External Environment and Organizational StructureDocument11 pagesExternal Environment and Organizational StructurePrajna DeyNo ratings yet

- Summer Traning Project ReportDocument13 pagesSummer Traning Project ReportMayank SaxenaNo ratings yet

- Formato Modelo de Conocimiento de Embarque - Bill of Lading Clase Mayo 10Document1 pageFormato Modelo de Conocimiento de Embarque - Bill of Lading Clase Mayo 10Andres Fernando Millan PereaNo ratings yet

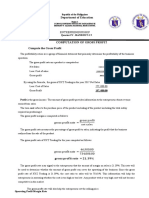

- Updated Reminders in The Assessment of TheDocument7 pagesUpdated Reminders in The Assessment of Therian.lee.b.tiangcoNo ratings yet

- Consumer Behavior: Consumer Behavior:: Consumer Perception Consumer PerceptionDocument50 pagesConsumer Behavior: Consumer Behavior:: Consumer Perception Consumer PerceptionRafpli SyaputraNo ratings yet

- Philippine Christian University: Preliminary ExaminationDocument5 pagesPhilippine Christian University: Preliminary Examinationleo pigafetaNo ratings yet

- William D. Fiser: Senior Construction Project Manager / EstimatorDocument2 pagesWilliam D. Fiser: Senior Construction Project Manager / EstimatorFirdaus PanthakyNo ratings yet

- Unit3 Logistics Concepts StudentsDocument39 pagesUnit3 Logistics Concepts Studentstriplej189No ratings yet

- Application of Porter 5 Forces To The Banking Industry by Anthony Tapiwa MazikanaDocument8 pagesApplication of Porter 5 Forces To The Banking Industry by Anthony Tapiwa MazikanaVishant KumarNo ratings yet

- In Strategy, Project Leadership and Pmos: WWW - Sbs.EduDocument8 pagesIn Strategy, Project Leadership and Pmos: WWW - Sbs.EduDiana KilelNo ratings yet

- Business Marketing: A Framework For MarketingDocument5 pagesBusiness Marketing: A Framework For MarketingJfSernioNo ratings yet

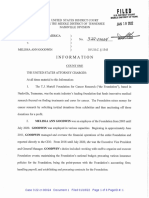

- USA v. Goodwin, InformationDocument6 pagesUSA v. Goodwin, InformationBillboardNo ratings yet

- Formatted Quantitative Aptitude For IBPS Clerk Prelims 2022 Solutions PDFDocument17 pagesFormatted Quantitative Aptitude For IBPS Clerk Prelims 2022 Solutions PDFZubair RahmanNo ratings yet

- 5f-Management and OperationsDocument17 pages5f-Management and OperationsMak PussNo ratings yet

- Productivity in Construction IndustryDocument13 pagesProductivity in Construction IndustryIzreen IsnainiNo ratings yet

- Brochure For: Unified Guidelines For Selection of Petrol Pump DealershipDocument24 pagesBrochure For: Unified Guidelines For Selection of Petrol Pump DealershipAbhinav YadavNo ratings yet

- Affidavit For A Lost Cheque: Family Responsibility Office PO Box 200 STN A Oshawa ON L1H 0C5Document1 pageAffidavit For A Lost Cheque: Family Responsibility Office PO Box 200 STN A Oshawa ON L1H 0C5boss_lekNo ratings yet

- R3 Pricelist Normal Units Fifty Seven PromenadeDocument1 pageR3 Pricelist Normal Units Fifty Seven PromenadeRani RdsNo ratings yet

- Entrepreneurship Reviewer (2nd Periodical)Document22 pagesEntrepreneurship Reviewer (2nd Periodical)casumbalmckaylacharmianNo ratings yet