You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Doing Business in The Philippines 2020Document75 pagesDoing Business in The Philippines 2020rheaNo ratings yet

- Financially Traded Products Readings PDFDocument210 pagesFinancially Traded Products Readings PDFJaspreet ChawlaNo ratings yet

- Danelia Testbanks Quiz 2345Document46 pagesDanelia Testbanks Quiz 2345Tinatini BakashviliNo ratings yet

- Domiciliary Theory: Submitted byDocument17 pagesDomiciliary Theory: Submitted byHannah Keziah Dela Cerna100% (1)

- TSN Insurance 1st ExamDocument76 pagesTSN Insurance 1st ExamHannah Keziah Dela CernaNo ratings yet

- Official Letters Patent Sagbama LGADocument7 pagesOfficial Letters Patent Sagbama LGASJ EndeleyNo ratings yet

- Red Flags - ShenanigansDocument6 pagesRed Flags - Shenanigansclmu00011No ratings yet

- VWAP & Squeeze Momentum in Day TradingDocument12 pagesVWAP & Squeeze Momentum in Day TradingPuneet NandaniNo ratings yet

- Gulfo v. Ancheta G.R. No. 175301 PDFDocument6 pagesGulfo v. Ancheta G.R. No. 175301 PDFHannah Keziah Dela CernaNo ratings yet

- Crim 2 Past CompiledDocument22 pagesCrim 2 Past CompiledHannah Keziah Dela CernaNo ratings yet

- Art. 82. Coverage. The Provisions of This Title Shall Apply To EmployeesDocument8 pagesArt. 82. Coverage. The Provisions of This Title Shall Apply To EmployeesHannah Keziah Dela Cerna100% (1)

- Narrative Report For Writ of KalikasanDocument54 pagesNarrative Report For Writ of KalikasanHannah Keziah Dela Cerna100% (2)

- Double Insurance and Over InsuranceDocument2 pagesDouble Insurance and Over InsuranceHannah Keziah Dela CernaNo ratings yet

- Leveraged ETFs and Volatility: The 33/22 StrategyDocument17 pagesLeveraged ETFs and Volatility: The 33/22 StrategybapcapNo ratings yet

- Just Compensation: Constitutional Law I ReviewDocument8 pagesJust Compensation: Constitutional Law I ReviewHannah Keziah Dela CernaNo ratings yet

- Case: Challenged in The Appellate Proceedings at Bar Is The of The Commissioner of Internal Revenue, AbsolvedDocument2 pagesCase: Challenged in The Appellate Proceedings at Bar Is The of The Commissioner of Internal Revenue, AbsolvedHannah Keziah Dela CernaNo ratings yet

- 2019 BANKING TSN First ExamDocument78 pages2019 BANKING TSN First ExamHannah Keziah Dela Cerna100% (1)

- Insurance Oral ExamDocument9 pagesInsurance Oral ExamHannah Keziah Dela CernaNo ratings yet

- CorpoRev - Jan 8 Part 1 - Dela CernaDocument4 pagesCorpoRev - Jan 8 Part 1 - Dela CernaHannah Keziah Dela CernaNo ratings yet

- CorpoRev - Jan 8 Part 3 - EmuyDocument4 pagesCorpoRev - Jan 8 Part 3 - EmuyHannah Keziah Dela CernaNo ratings yet

- Consti I Review TSN Template With SampleDocument5 pagesConsti I Review TSN Template With SampleHannah Keziah Dela CernaNo ratings yet

- !:ourt: L/epublic of TbeDocument21 pages!:ourt: L/epublic of TbeHannah Keziah Dela CernaNo ratings yet

- Mandanas v. Ochoa 2018 - G.R. No. 199802Document35 pagesMandanas v. Ochoa 2018 - G.R. No. 199802Hannah Keziah Dela CernaNo ratings yet

- General Overview: Taxation Law ReviewDocument2 pagesGeneral Overview: Taxation Law ReviewHannah Keziah Dela CernaNo ratings yet

- Constitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveDocument7 pagesConstitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveHannah Keziah Dela CernaNo ratings yet

- G.R. No. 212938Document13 pagesG.R. No. 212938Hannah Keziah Dela CernaNo ratings yet

- Tax II Second Exam TSN Partial 2Document79 pagesTax II Second Exam TSN Partial 2Hannah Keziah Dela CernaNo ratings yet

- SEC-OGCOpinionNo.09-04 - Public Offering of SecuritiesDocument4 pagesSEC-OGCOpinionNo.09-04 - Public Offering of SecuritiesHannah Keziah Dela CernaNo ratings yet

- PS322 - IR - Ch04part2 - Sociological LiberalismDocument11 pagesPS322 - IR - Ch04part2 - Sociological LiberalismHannah Keziah Dela CernaNo ratings yet

- Supreme Court: Petitioner, vs. RespondentDocument12 pagesSupreme Court: Petitioner, vs. RespondentHannah Keziah Dela CernaNo ratings yet

- G.R. No. 139802 - VICENTE PONCE vs. ALSONS CEMENT CORPORATION, ET AL.Document9 pagesG.R. No. 139802 - VICENTE PONCE vs. ALSONS CEMENT CORPORATION, ET AL.Hannah Keziah Dela CernaNo ratings yet

- G.R. No. L-28138Document4 pagesG.R. No. L-28138Hannah Keziah Dela CernaNo ratings yet

- Power Homes v. SEC - G.R. No. 164182 PDFDocument7 pagesPower Homes v. SEC - G.R. No. 164182 PDFHannah Keziah Dela CernaNo ratings yet

- G.R. No. L-36081Document6 pagesG.R. No. L-36081Hannah Keziah Dela CernaNo ratings yet

- G.R. No. L-23794Document3 pagesG.R. No. L-23794Hannah Keziah Dela CernaNo ratings yet

- Macroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulDocument21 pagesMacroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulMaria KulawikNo ratings yet

- Market IndicatorsDocument7 pagesMarket Indicatorssantosh kumar mauryaNo ratings yet

- NikeDocument10 pagesNikeCarissa KusumaNo ratings yet

- 1112 Ias 21 Consolidation of Foreign Subsidiary Practice RevisionDocument24 pages1112 Ias 21 Consolidation of Foreign Subsidiary Practice RevisionElie YabroudiNo ratings yet

- AmlaDocument8 pagesAmlaRenz AmonNo ratings yet

- Tb02 - Test Bank Chapter 2 Tb02 - Test Bank Chapter 2Document45 pagesTb02 - Test Bank Chapter 2 Tb02 - Test Bank Chapter 2Renz AlconeraNo ratings yet

- Global Financial ManagementDocument17 pagesGlobal Financial ManagementMamta GroverNo ratings yet

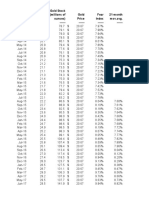

- Fear Index M3 Gold Stock (Billions of (Millions of Gold Fear 21-Month Dollars) Ounces) Price Index Mov - Avg.Document25 pagesFear Index M3 Gold Stock (Billions of (Millions of Gold Fear 21-Month Dollars) Ounces) Price Index Mov - Avg.dhaulNo ratings yet

- Kim - Sbi Etf Sensex PDFDocument45 pagesKim - Sbi Etf Sensex PDFRmc RmcNo ratings yet

- Cyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityDocument7 pagesCyient LTD.: Q1FY20: Weak Quarter, Lack VisibilityADNo ratings yet

- SACL Update On The Scheme of Arrangement Between Starafrica and Its Members and Its CreditorsDocument1 pageSACL Update On The Scheme of Arrangement Between Starafrica and Its Members and Its CreditorsBusiness Daily ZimbabweNo ratings yet

- Kitkungvan CVDocument1 pageKitkungvan CVGoran LojpurNo ratings yet

- ZBB Energy Corporation: Form S-1Document53 pagesZBB Energy Corporation: Form S-1Ankur DesaiNo ratings yet

- HSBC Holdings PLCDocument13 pagesHSBC Holdings PLCdebubkp2042No ratings yet

- Tianjin Plastics (China) : Maple EnergyDocument11 pagesTianjin Plastics (China) : Maple EnergySoraya ReneNo ratings yet

- Final Proposal (Chee)Document13 pagesFinal Proposal (Chee)Faraliza JumayleezaNo ratings yet

- Argentina - Letter of Support For Joint ProposalDocument14 pagesArgentina - Letter of Support For Joint ProposalBAE NegociosNo ratings yet

- DB ISIN DE000DB7XHP3 and ISIN XS1071551474Document76 pagesDB ISIN DE000DB7XHP3 and ISIN XS1071551474omidreza tabrizianNo ratings yet

- Unilever TodayDocument34 pagesUnilever TodayEmee Haque50% (2)

- National Stock Exchange of India (NSE)Document16 pagesNational Stock Exchange of India (NSE)Mohit SuranaNo ratings yet

- Akd Equity Research ReportDocument11 pagesAkd Equity Research ReportZahid UsmanNo ratings yet

- International Business Hill An Asian Perpective Chapter 9Document29 pagesInternational Business Hill An Asian Perpective Chapter 9HafeezAbdullahNo ratings yet

- 1.1.1 Derivatives - IntroductionDocument27 pages1.1.1 Derivatives - Introductionmanojbhatia1220No ratings yet