You might also like

- Financial Accounting Global Settings - Rohini GadkariDocument26 pagesFinancial Accounting Global Settings - Rohini GadkariSahitee BasaniNo ratings yet

- Mary The Queen College of Pampanga Inc.: Agency Accounting Focus NotesDocument16 pagesMary The Queen College of Pampanga Inc.: Agency Accounting Focus NotesAllain GuanlaoNo ratings yet

- Fischer10j Ch21 TBDocument2 pagesFischer10j Ch21 TBLouiza Kyla AridaNo ratings yet

- Answer Key - Chapter 5 - 2020 EditionDocument37 pagesAnswer Key - Chapter 5 - 2020 EditionDaniel DialinoNo ratings yet

- ACCTSPTRANS All About PartnershipDocument7 pagesACCTSPTRANS All About PartnershipShailene David0% (1)

- Busicom Prob 6-8Document7 pagesBusicom Prob 6-8JrllsyNo ratings yet

- 8.0 TVM Financial PlanningDocument2 pages8.0 TVM Financial PlanningYashvi MahajanNo ratings yet

- Pracc2 ReviewerDocument8 pagesPracc2 ReviewerLucas GalingNo ratings yet

- AainvtyDocument4 pagesAainvtyRodolfo SayangNo ratings yet

- ADV2 Chapter12 QADocument4 pagesADV2 Chapter12 QAMa Alyssa DelmiguezNo ratings yet

- Part I: Installment Part I: Installment Sales (1-140) Sales (1-140)Document77 pagesPart I: Installment Part I: Installment Sales (1-140) Sales (1-140)Gale RasNo ratings yet

- Finals Quiz 2 Buscom Version 2Document3 pagesFinals Quiz 2 Buscom Version 2Kristina Angelina ReyesNo ratings yet

- Activity 1 Home Office and Branch Accounting - General ProceduresDocument4 pagesActivity 1 Home Office and Branch Accounting - General ProceduresDaenielle EspinozaNo ratings yet

- Problem: I - Statement of Affairs and Deficiency AccountDocument1 pageProblem: I - Statement of Affairs and Deficiency AccountAnn Marie GabayNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Multiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofDocument12 pagesMultiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofRie Cabigon100% (1)

- Rmbe Afar For PrintingDocument18 pagesRmbe Afar For PrintingjxnNo ratings yet

- D. All of ThemDocument6 pagesD. All of ThemRyan CapistranoNo ratings yet

- Problem 17-1, ContinuedDocument6 pagesProblem 17-1, ContinuedJohn Carlo D MedallaNo ratings yet

- NFJPIA Mockboard 2011 P2Document6 pagesNFJPIA Mockboard 2011 P2ELAIZA BASHNo ratings yet

- NCR Cup 6 - Afar: Lina Mina NinaDocument2 pagesNCR Cup 6 - Afar: Lina Mina Ninahehehedontmind meNo ratings yet

- Additional Problems On MergerDocument6 pagesAdditional Problems On MergerkakeguruiNo ratings yet

- Cost To CostDocument1 pageCost To CostAnirban Roy ChowdhuryNo ratings yet

- Solution Chapter 9Document15 pagesSolution Chapter 9BobslaneLlenos0% (2)

- Correction of Errors: Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionDocument5 pagesCorrection of Errors: Identify The Letter of The Choice That Best Completes The Statement or Answers The QuestionmaurNo ratings yet

- Activity - Chapter 4Document2 pagesActivity - Chapter 4Greta DuqueNo ratings yet

- Chapter 08 DayagDocument24 pagesChapter 08 DayagEureka Fernandez67% (6)

- Competency Appraisal UM Digos (PARTNERSHIP)Document10 pagesCompetency Appraisal UM Digos (PARTNERSHIP)Diana Faye CaduadaNo ratings yet

- Audcap1 Final OutputDocument7 pagesAudcap1 Final OutputIvan AnaboNo ratings yet

- AFARicpaDocument23 pagesAFARicpaRegine YbañezNo ratings yet

- Accounting For Special Transactions and Cost Accounting and ControlDocument12 pagesAccounting For Special Transactions and Cost Accounting and ControlRNo ratings yet

- "How Well Am I Doing?" Statement of Cash Flows: Managerial Accounting, 9/eDocument51 pages"How Well Am I Doing?" Statement of Cash Flows: Managerial Accounting, 9/eMARY JUSTINE PAQUIBOTNo ratings yet

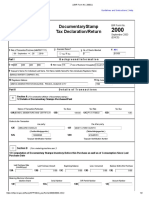

- Drafted BIR Form No. 2000Document2 pagesDrafted BIR Form No. 2000Kevin Besa100% (1)

- Jun Zen Ralph Yap BSA - 3 Year Let's CheckDocument2 pagesJun Zen Ralph Yap BSA - 3 Year Let's CheckJunzen Ralph Yap100% (1)

- Act13 Orquia-Anndhrea Bsa-32Document3 pagesAct13 Orquia-Anndhrea Bsa-32Clint RoblesNo ratings yet

- SW - NpoDocument1 pageSW - NpoGwy HipolitoNo ratings yet

- Ans To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsDocument188 pagesAns To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsLouise GazaNo ratings yet

- Mga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Document12 pagesMga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Hannah Jane UmbayNo ratings yet

- MAS - Group 5Document7 pagesMAS - Group 5beleky watersNo ratings yet

- A Government Employee May Claim The Tax InformerDocument3 pagesA Government Employee May Claim The Tax InformerYuno NanaseNo ratings yet

- Practical Accounting 2 - ExaminationDocument10 pagesPractical Accounting 2 - ExaminationPrincess Claris ArauctoNo ratings yet

- Aud Theo Part 2Document10 pagesAud Theo Part 2Naia Gonzales0% (2)

- Consolidating Balance SheetsDocument4 pagesConsolidating Balance Sheetsangel2199No ratings yet

- 1398236Document3 pages1398236mohitgaba19No ratings yet

- AC 300 Activity - 04.11.2023 Groupings: Group 1 Group 2 Group 3 Group 4 Group 5 Group 6Document2 pagesAC 300 Activity - 04.11.2023 Groupings: Group 1 Group 2 Group 3 Group 4 Group 5 Group 6Frencis A. EsquierdoNo ratings yet

- Chapter 12-14Document18 pagesChapter 12-14Serena Van Der WoodsenNo ratings yet

- Finals - Receivables 2 Exercises WithoutDocument4 pagesFinals - Receivables 2 Exercises WithoutA.B AmpuanNo ratings yet

- Practical Accounti ng2: Business CombinationsDocument9 pagesPractical Accounti ng2: Business CombinationsKath SapitanNo ratings yet

- AA2Q1Document1 pageAA2Q1Sweet EmmeNo ratings yet

- 6 ACCT 2A&B C. OperationDocument10 pages6 ACCT 2A&B C. OperationShannon Mojica100% (1)

- Solution Chapter 6Document10 pagesSolution Chapter 6Clarize R. MabiogNo ratings yet

- Abc Stock AcquisitionDocument13 pagesAbc Stock AcquisitionMary Joy AlbandiaNo ratings yet

- Audit ReviewDocument9 pagesAudit ReviewephraimNo ratings yet

- CBS Corporation Purchased 10Document12 pagesCBS Corporation Purchased 10Stella SabaoanNo ratings yet

- HB Quiz 2018-2021Document3 pagesHB Quiz 2018-2021Allyssa Kassandra LucesNo ratings yet

- 25781306Document19 pages25781306GuinevereNo ratings yet

- Buscom Quiz 2 MidtermDocument2 pagesBuscom Quiz 2 MidtermRafael Capunpon VallejosNo ratings yet

- Midterm Exam No. 2Document1 pageMidterm Exam No. 2Anie MartinezNo ratings yet

- HOBA QuestionsDocument7 pagesHOBA QuestionsKristine CorporalNo ratings yet

- The Balance Sheet For The Partnership of JJ CC and TTDocument1 pageThe Balance Sheet For The Partnership of JJ CC and TTdagohoy kennethNo ratings yet

- Consolidation Finanacial StatementDocument38 pagesConsolidation Finanacial Statementsneha9121No ratings yet

- COS 103 - Variable Costing ExercisesDocument2 pagesCOS 103 - Variable Costing ExercisesAivie Pangilinan100% (1)

- Ilovepdf - Merged (5) - English - 1665416895Document6 pagesIlovepdf - Merged (5) - English - 1665416895Durga DeviNo ratings yet

- AXIS BANK Annual-Report-2010Document177 pagesAXIS BANK Annual-Report-2010Vasundhara KediaNo ratings yet

- Mitsubishi Annual Statement 2010Document192 pagesMitsubishi Annual Statement 2010buddyNo ratings yet

- CF Mid Term - Revision Set 1Document11 pagesCF Mid Term - Revision Set 1linhngo.31221020350No ratings yet

- Activity in Inventory Estimation, Retail InventoryDocument2 pagesActivity in Inventory Estimation, Retail InventoryTrisha VillegasNo ratings yet

- Chapter 12, Problem 1COMP: (To Record Issuance of 4,000 Preferred Shares in Excess of Par)Document1 pageChapter 12, Problem 1COMP: (To Record Issuance of 4,000 Preferred Shares in Excess of Par)Varun SharmaNo ratings yet

- Professional TrainingDocument2 pagesProfessional TrainingBreak ForexNo ratings yet

- Revised Capital StructureDocument39 pagesRevised Capital StructureKrishna AgarwalNo ratings yet

- Canara Bank Annual Report 2010 11Document217 pagesCanara Bank Annual Report 2010 11Sagar KedarNo ratings yet

- Wiley CFA Test Bank 180408 (40 Preguntas) - PDF - Net Present Value - Internal Rate of ReturnDocument23 pagesWiley CFA Test Bank 180408 (40 Preguntas) - PDF - Net Present Value - Internal Rate of ReturndbohnentvNo ratings yet

- Basfin 1Document4 pagesBasfin 1Joshua AlfanteNo ratings yet

- Accounting Text Book - 2019Document37 pagesAccounting Text Book - 2019Shenali NupehewaNo ratings yet

- PNL Account Cashflow Forecast: Missing ValuesDocument5 pagesPNL Account Cashflow Forecast: Missing ValuespiyaNo ratings yet

- Maam CoryDocument3 pagesMaam CoryCHERIE ANN APRIL SULITNo ratings yet

- Cards Mega-Mastercard Terms and ConditionsDocument1 pageCards Mega-Mastercard Terms and Conditionsmohannad.aldahakNo ratings yet

- Revision Test Papers: Common For Intermediate (IPC) Course Group - IDocument192 pagesRevision Test Papers: Common For Intermediate (IPC) Course Group - IRonaldobalaji26122000 Balaji100% (1)

- Kpi DictionaryDocument18 pagesKpi DictionaryjbarbosaNo ratings yet

- FABM1 Book of AccountsDocument33 pagesFABM1 Book of AccountsMicah BlazaNo ratings yet

- ES301 Engineering-Economics Chapter-5 Depreciation PDFDocument14 pagesES301 Engineering-Economics Chapter-5 Depreciation PDFSandra WendamNo ratings yet

- Worksheet 18 Company Issue of SharesDocument5 pagesWorksheet 18 Company Issue of SharesNishanth ChoudharyNo ratings yet

- 2024 04 1 04 34 43 Statement - 1704323083904Document22 pages2024 04 1 04 34 43 Statement - 1704323083904karthickNo ratings yet

- النظام المحاسبي الكامل (اليوميه &القوائم &التحليلات والايضاحات المتتمه للقوايم الماليه)Document2,103 pagesالنظام المحاسبي الكامل (اليوميه &القوائم &التحليلات والايضاحات المتتمه للقوايم الماليه)MAZIN SALAHELDEENNo ratings yet

- Capital Structure TheoriesDocument47 pagesCapital Structure Theoriesamol_more37No ratings yet

- Report On Financial Reporting PDFFFDocument38 pagesReport On Financial Reporting PDFFFMohit AroraNo ratings yet

- Audit of PPE - Homework - AnswersDocument15 pagesAudit of PPE - Homework - AnswersMarnelli CatalanNo ratings yet

- PNC MT Examination Finacc 3Document3 pagesPNC MT Examination Finacc 3joevitt delfinadoNo ratings yet

- Wiley - Chapter 9: Inventories: Additional Valuation IssuesDocument20 pagesWiley - Chapter 9: Inventories: Additional Valuation IssuesIvan BliminseNo ratings yet

- Karvy Demat ScamDocument4 pagesKarvy Demat ScamcdhjvkfyutdtjyNo ratings yet