You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Strategic Analysis On SonyDocument37 pagesStrategic Analysis On Sonylavkush_khannaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Test BankDocument136 pagesTest BankLouise100% (1)

- Trading Options Income: Strangle vs Double Ratio SpreadDocument1 pageTrading Options Income: Strangle vs Double Ratio Spreadsergiob63No ratings yet

- Drafting New PDFDocument253 pagesDrafting New PDFIshan SharmaNo ratings yet

- SAP Analytics Cloud for Planning Use Cases ExplainedDocument23 pagesSAP Analytics Cloud for Planning Use Cases ExplainedGasserNo ratings yet

- Bar QuestionsLAborDocument50 pagesBar QuestionsLAborBasmuthNo ratings yet

- Micro Analysis of ToyotoDocument32 pagesMicro Analysis of ToyotoMohammed Tahir100% (1)

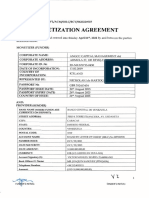

- SBLC DOA - ANGCC - SignedDocument9 pagesSBLC DOA - ANGCC - SignedfranviNo ratings yet

- JPMorgan Asia Pacific Equity Strategy 20100903Document36 pagesJPMorgan Asia Pacific Equity Strategy 20100903iamdennismiracleNo ratings yet

- Bangalore UniversityDocument2 pagesBangalore UniversitySourav ChowdhuryNo ratings yet

- The Influence of Innovation Strategy and Organizational Innovation On Innovation Quality and Performance PDFDocument38 pagesThe Influence of Innovation Strategy and Organizational Innovation On Innovation Quality and Performance PDFEdward LumentaNo ratings yet

- Rawls Theory FairDocument20 pagesRawls Theory FairIshan Sharma100% (1)

- State of Taxila v. Vir Bahadur MemorialDocument28 pagesState of Taxila v. Vir Bahadur MemorialIshan Sharma100% (2)

- State of Taxila v. Vir Bahadur MemorialDocument28 pagesState of Taxila v. Vir Bahadur MemorialIshan Sharma100% (2)

- Citystate Savings Bank V TobiasDocument2 pagesCitystate Savings Bank V TobiasBurnok SupolNo ratings yet

- In All,: LL.M., First (For Law in World Marks: (Unit-I) IsDocument2 pagesIn All,: LL.M., First (For Law in World Marks: (Unit-I) IsIshan SharmaNo ratings yet

- Posthumus Reproduction and Its Legal and Ethical ChallengesDocument6 pagesPosthumus Reproduction and Its Legal and Ethical ChallengesIshan SharmaNo ratings yet

- Posthumus Reproduction and Its Legal and Ethical ChallengesDocument6 pagesPosthumus Reproduction and Its Legal and Ethical ChallengesIshan SharmaNo ratings yet

- Constitutional Provisions Related To Health - AmanDocument13 pagesConstitutional Provisions Related To Health - AmanIshan SharmaNo ratings yet

- DP 1925Document28 pagesDP 1925kantata4No ratings yet

- Socio-cultural impact of globalization in India analyzedDocument9 pagesSocio-cultural impact of globalization in India analyzedIshan SharmaNo ratings yet

- Multid Charac Global Grebosz 2015Document14 pagesMultid Charac Global Grebosz 2015Ishan SharmaNo ratings yet

- Law and Justice in The Globalizing WorldDocument32 pagesLaw and Justice in The Globalizing WorldIshan SharmaNo ratings yet

- A Critical Methodology of Globalization - Politics of The 21st CenDocument27 pagesA Critical Methodology of Globalization - Politics of The 21st CenIshan SharmaNo ratings yet

- Code On Social SecurityDocument13 pagesCode On Social SecurityIshan SharmaNo ratings yet

- DP 1925Document28 pagesDP 1925kantata4No ratings yet

- New Text DocumentDocument1 pageNew Text DocumentIshan SharmaNo ratings yet

- Notice Directors Report 2020 Dalhousie GardensDocument17 pagesNotice Directors Report 2020 Dalhousie GardensIshan SharmaNo ratings yet

- GRMCE NewDocument245 pagesGRMCE NewIshan SharmaNo ratings yet

- Drafting New 2Document253 pagesDrafting New 2Ishan SharmaNo ratings yet

- Template of Resume For CS Trainee PDFDocument2 pagesTemplate of Resume For CS Trainee PDFjanardhan CA,CSNo ratings yet

- Labour Law ProjectDocument25 pagesLabour Law ProjectIshan SharmaNo ratings yet

- Document From BhimikaDocument3 pagesDocument From BhimikaIshan SharmaNo ratings yet

- ChandigarhDocument3 pagesChandigarhIshan SharmaNo ratings yet

- GRMCE NewDocument245 pagesGRMCE NewIshan SharmaNo ratings yet

- Update Your CV Daily or After Every One Hour So That It Can Remain in The Top. 2. Directly Approaching The CompaniesDocument1 pageUpdate Your CV Daily or After Every One Hour So That It Can Remain in The Top. 2. Directly Approaching The CompaniesIshan SharmaNo ratings yet

- Document From BhimikaDocument3 pagesDocument From BhimikaIshan SharmaNo ratings yet

- Document From BhimikaDocument3 pagesDocument From BhimikaIshan SharmaNo ratings yet

- DocumentDocument1 pageDocumentIshan SharmaNo ratings yet

- Corporate Financial Reporting PDFDocument3 pagesCorporate Financial Reporting PDFIshan SharmaNo ratings yet

- SolutionDocument3 pagesSolutionmaiaaaaNo ratings yet

- OMNIA Presentation ENGDocument30 pagesOMNIA Presentation ENGdharampal dhimanNo ratings yet

- TDS Return Late Fee Tax DeductibilityDocument5 pagesTDS Return Late Fee Tax DeductibilityDivyaNo ratings yet

- Leadway Assurance Competitor AnalysisDocument8 pagesLeadway Assurance Competitor AnalysisAlayo AdedapoNo ratings yet

- DDR 2015 en fr0000053548Document264 pagesDDR 2015 en fr0000053548Cao LongNo ratings yet

- Accounting - Business Plan SampleDocument51 pagesAccounting - Business Plan SamplejohnpenoniaNo ratings yet

- Unitop MEE CatalogDocument7 pagesUnitop MEE CatalogSaket SharmaNo ratings yet

- MTD638Document20 pagesMTD638Ayla KowNo ratings yet

- Major Challages of Organization CompleteDocument11 pagesMajor Challages of Organization Completekhawar hafeezNo ratings yet

- NFL Stars Score in Real Estate: Thousands Flee Syrian OffensiveDocument56 pagesNFL Stars Score in Real Estate: Thousands Flee Syrian OffensivestefanoNo ratings yet

- Questions Chapter 16 FinanceDocument23 pagesQuestions Chapter 16 FinanceJJNo ratings yet

- Account Statement: Page 1 of 3Document3 pagesAccount Statement: Page 1 of 3achyut kumarNo ratings yet

- Kurwitu Ventures LTD Annual Report Financial Statements For The Year Ended 31st Dec 2017 PDFDocument44 pagesKurwitu Ventures LTD Annual Report Financial Statements For The Year Ended 31st Dec 2017 PDFKibet KiptooNo ratings yet

- A Study On Overview of Employee Attrition Rate in India 150759937Document5 pagesA Study On Overview of Employee Attrition Rate in India 150759937Pramit NarayanNo ratings yet

- National Policy On Commuted Overtime For Medical & Dental PersonnelDocument13 pagesNational Policy On Commuted Overtime For Medical & Dental PersonnelNopepsi SobetwaNo ratings yet

- Cayman Lakeside Estate Investment Guide - Cayman Islands - DSR Asset Management LTDDocument12 pagesCayman Lakeside Estate Investment Guide - Cayman Islands - DSR Asset Management LTDProperty Cayman IslandsNo ratings yet

- Computer Accounting Project WorkDocument7 pagesComputer Accounting Project Workapi-319474134No ratings yet

- Home Buying CalculatorDocument7 pagesHome Buying CalculatorDan CliffeNo ratings yet

- From Seers to Sen: The Evolution of Economic DevelopmentDocument22 pagesFrom Seers to Sen: The Evolution of Economic DevelopmentBusola Esther DunmadeNo ratings yet