You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Concept Note of The Proposed ResearchDocument3 pagesConcept Note of The Proposed ResearchMtanaNo ratings yet

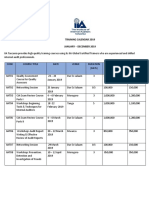

- Training Calender 2020 PDFDocument5 pagesTraining Calender 2020 PDFMtana100% (1)

- Training Calender 2020 PDFDocument5 pagesTraining Calender 2020 PDFMtana100% (1)

- IIA Calender 2019Document5 pagesIIA Calender 2019MtanaNo ratings yet

- EconomicsDocument11 pagesEconomicsMtanaNo ratings yet

- Finance Term PaperDocument10 pagesFinance Term PaperMtanaNo ratings yet

- Jack Ma's Vision for the Electronic World Trade Platform to Help SMEsDocument1 pageJack Ma's Vision for the Electronic World Trade Platform to Help SMEsMtanaNo ratings yet

- Presentation On The New Nbaa Bylaws: Registration and Practicing Bylaws 2017 By: Agnes Kessy (Adv.) 28 April 2017Document23 pagesPresentation On The New Nbaa Bylaws: Registration and Practicing Bylaws 2017 By: Agnes Kessy (Adv.) 28 April 2017MtanaNo ratings yet

- Economic AssignmentDocument1 pageEconomic AssignmentMtanaNo ratings yet

- 2 How MGMT Perpetrates FraudDocument3 pages2 How MGMT Perpetrates FraudMtanaNo ratings yet

- 460 Term Paper ExampleDocument18 pages460 Term Paper ExampleLyra Kay BatiancilaNo ratings yet

- Markets Analysis SWOTDocument8 pagesMarkets Analysis SWOTMtanaNo ratings yet

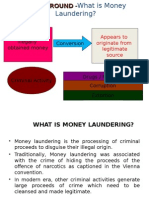

- Accountants Annual Conference - Overview of Money LaunderingDocument23 pagesAccountants Annual Conference - Overview of Money LaunderingMtanaNo ratings yet

- Term Paper GuidelinesDocument8 pagesTerm Paper GuidelinesNer InnNo ratings yet

- Principles of Fraud Detection Part1Document2 pagesPrinciples of Fraud Detection Part1MtanaNo ratings yet

- Environmental Audititing 2006Document15 pagesEnvironmental Audititing 2006MtanaNo ratings yet

- Misappropriation of AssetsDocument2 pagesMisappropriation of AssetsMtanaNo ratings yet

- 5.public Sector AuditDocument15 pages5.public Sector AuditMtanaNo ratings yet

- 5.public Sector AuditDocument15 pages5.public Sector AuditMtanaNo ratings yet

- Accountants Annual Conference - Overview of Money LaunderingDocument23 pagesAccountants Annual Conference - Overview of Money LaunderingMtanaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Oliver V Phil Savings BankDocument3 pagesOliver V Phil Savings BankBeverlyn JamisonNo ratings yet

- Dissertation Topic On Financial Risk ManagementDocument8 pagesDissertation Topic On Financial Risk ManagementWriteMyCustomPaperSingapore100% (1)

- Financial Analysis and Accounting RecordsDocument11 pagesFinancial Analysis and Accounting RecordsRobert HamiltonNo ratings yet

- Servicewide Specialists V CADocument2 pagesServicewide Specialists V CASocNo ratings yet

- Budgetary Control Lesson GuideDocument11 pagesBudgetary Control Lesson GuiderscjatNo ratings yet

- The Largest 100 Credit UnionsDocument6 pagesThe Largest 100 Credit Unionseduluz1976No ratings yet

- The Souk Al-Manakh CrashDocument18 pagesThe Souk Al-Manakh CrashNzugu HoffmanNo ratings yet

- Bharat Sanchar Nigam Limited: Customer Application FormDocument4 pagesBharat Sanchar Nigam Limited: Customer Application FormmadhurialamuriNo ratings yet

- Financial Literacy Concept Digest: Standards Key ConceptsDocument8 pagesFinancial Literacy Concept Digest: Standards Key ConceptsJustin Magnanao100% (1)

- CERTIFIED CREDIT PROFESSIONAL PREVIOUS YEAR QUESTIONSDocument10 pagesCERTIFIED CREDIT PROFESSIONAL PREVIOUS YEAR QUESTIONShariNo ratings yet

- Credit Risk Management On Ethiopian Commercial Banks": Case of Selected Commercial Banks in Adama TownDocument36 pagesCredit Risk Management On Ethiopian Commercial Banks": Case of Selected Commercial Banks in Adama TownAbdii Dhufeera100% (2)

- Section 8 Business FinanceDocument11 pagesSection 8 Business FinanceLeeana MaharajNo ratings yet

- The Impacts of Financial Challenges in Case of Real Estate Developers in EthiopiaDocument7 pagesThe Impacts of Financial Challenges in Case of Real Estate Developers in Ethiopiatesfalem kirosNo ratings yet

- Student ManualDocument55 pagesStudent Manualmikeb92556No ratings yet

- Chapter 10 Credit AnalysisDocument69 pagesChapter 10 Credit AnalysisRobertus GaniNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaIBBF FitnessNo ratings yet

- History and Advantages of Bartering SystemsDocument13 pagesHistory and Advantages of Bartering SystemsJohn TurnerNo ratings yet

- METROPOLITAN BANK and TRUST COMPANY VDocument1 pageMETROPOLITAN BANK and TRUST COMPANY VJay R CristobalNo ratings yet

- Reserve Bank of IndiaDocument27 pagesReserve Bank of IndiaRajesh SukhaniNo ratings yet

- HDFC Credit Card Charge DetailsDocument11 pagesHDFC Credit Card Charge DetailsVarun G ShenoyNo ratings yet

- Effect of Liquidity Risk On Performance of Deposit Money Banks in NigeriaDocument6 pagesEffect of Liquidity Risk On Performance of Deposit Money Banks in NigeriaEditor IJTSRDNo ratings yet

- Open Pdfcoffee - Com San Beda Credit Transactions PDF FreeDocument33 pagesOpen Pdfcoffee - Com San Beda Credit Transactions PDF FreeMark OrlinoNo ratings yet

- Module 1: Expense Report Overview and Basic Setup Module OverviewDocument38 pagesModule 1: Expense Report Overview and Basic Setup Module OverviewMohammad Nabi BaderyNo ratings yet

- New Law Increases Number of Creditworthy KenyansDocument1 pageNew Law Increases Number of Creditworthy KenyansEmeka NkemNo ratings yet

- The Center Court Phase 1 Price List GurgaonDocument5 pagesThe Center Court Phase 1 Price List GurgaonBharat ChatrathNo ratings yet

- STD X CH 3 Money and Credit Notes (21-22)Document6 pagesSTD X CH 3 Money and Credit Notes (21-22)Dhwani ShahNo ratings yet

- Internal Continuous Assessment of Monetary Performance in AfghanistanDocument13 pagesInternal Continuous Assessment of Monetary Performance in AfghanistanVikas SinghNo ratings yet

- Bank Management Summary - Chapter OneDocument6 pagesBank Management Summary - Chapter Oneabshir sugoowNo ratings yet

- Bank GuaranteeDocument30 pagesBank GuaranteeKaruna ThatsitNo ratings yet

- Navitar-Immersive World-RFQ For 2 HM4K 178 HL Lenses For Christie Griffyn 4K32 Dual Cove-2020!09!09 - V1Document3 pagesNavitar-Immersive World-RFQ For 2 HM4K 178 HL Lenses For Christie Griffyn 4K32 Dual Cove-2020!09!09 - V1BoanergeNo ratings yet