You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter Sixteen Test Item File Problems: Tif Problem Sixteen - 1 Rollovers Under Section 85 - Essay QuestionsDocument68 pagesChapter Sixteen Test Item File Problems: Tif Problem Sixteen - 1 Rollovers Under Section 85 - Essay Questionsarhamoh0% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Aefpm5487a 2023Document4 pagesAefpm5487a 2023enjoy enjoy enjoyNo ratings yet

- VAT On Sale of Goods and PropertiesDocument55 pagesVAT On Sale of Goods and PropertiesNEstanda100% (1)

- Good & Service Tax: 1. What Is GST?Document5 pagesGood & Service Tax: 1. What Is GST?Rabin DebnathNo ratings yet

- Sre 2022 and 2023Document4 pagesSre 2022 and 2023barangaymaharlikawest017No ratings yet

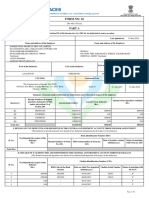

- GSTR3B 27BCGPS7468K1ZR 062022Document3 pagesGSTR3B 27BCGPS7468K1ZR 062022Aman JaiswalNo ratings yet

- Atal Pension Yojana Subscriber FormDocument1 pageAtal Pension Yojana Subscriber FormTarsem SoniNo ratings yet

- Notes in Organization and Functions of The BirDocument5 pagesNotes in Organization and Functions of The BirNinaNo ratings yet

- ECON 13 - Reflection Paper No. 1Document1 pageECON 13 - Reflection Paper No. 1Leianneza PioquintoNo ratings yet

- 2024Document664 pages2024vikenveerNo ratings yet

- Why Engineers Need To Understand The Financial Statements?: Contemporary Engineering Economics, 5th Edition. ©2010Document8 pagesWhy Engineers Need To Understand The Financial Statements?: Contemporary Engineering Economics, 5th Edition. ©2010GhostNo ratings yet

- Bharat Sanchar Nigam Limited: Invoice For Post Paid ServicesDocument2 pagesBharat Sanchar Nigam Limited: Invoice For Post Paid ServicessuryaNo ratings yet

- Income Taxation ReviewerDocument9 pagesIncome Taxation ReviewerAira MabezaNo ratings yet

- Chapter 2 - Income From House PropertyDocument15 pagesChapter 2 - Income From House PropertyPuran GuptaNo ratings yet

- 0006 Abdul Qadir MemonDocument114 pages0006 Abdul Qadir Memonflower4u2008No ratings yet

- Self Assessment Tax or Selfish Assessment TaxDocument9 pagesSelf Assessment Tax or Selfish Assessment TaxABC 123No ratings yet

- 5th Chapter Assessement of IndividualDocument13 pages5th Chapter Assessement of IndividualManjunath R IligerNo ratings yet

- TAX RefExamDocument16 pagesTAX RefExamjeralyn juditNo ratings yet

- Tax Identification Number (TIN) Taxpayer Form Fee DeadlineDocument2 pagesTax Identification Number (TIN) Taxpayer Form Fee DeadlineFabiano JoeyNo ratings yet

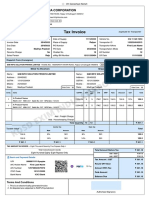

- A5 InvoiceDocument1 pageA5 InvoiceVaibhav PritwaniNo ratings yet

- Flipkart Labels 01 Apr 2024 09 52Document1 pageFlipkart Labels 01 Apr 2024 09 524frontenterprises.2023No ratings yet

- Head LightDocument1 pageHead Light166.b.com.3.sxcNo ratings yet

- Azepm3818m 2018-19 PDFDocument2 pagesAzepm3818m 2018-19 PDFlogu prabhuNo ratings yet

- Salaryslip June 2022Document2 pagesSalaryslip June 2022Raja BabuNo ratings yet

- Talenta Payslip PT Kobus Smart Service Agu 2023 SOPIAN PANCA PUTRADocument1 pageTalenta Payslip PT Kobus Smart Service Agu 2023 SOPIAN PANCA PUTRASopianpancputraNo ratings yet

- Etaxguide Cit Transfer Pricing Guidelines 6th EditionDocument182 pagesEtaxguide Cit Transfer Pricing Guidelines 6th EditionSamNo ratings yet

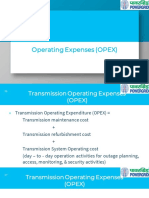

- Operating Expenses (OPEX)Document9 pagesOperating Expenses (OPEX)ASH TVNo ratings yet

- Annex B-2Document1 pageAnnex B-2Von Virchel VallesNo ratings yet

- Indian Customs EDI System - ExportsDocument8 pagesIndian Customs EDI System - ExportsSuperintendentHqrs CustomsStatisticsNo ratings yet

- Tata Aig General Insurance Co LTD: Insured Declared Value (IDV) 557000.00Document5 pagesTata Aig General Insurance Co LTD: Insured Declared Value (IDV) 557000.00ApoorvNo ratings yet