You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Hindu Editorials Summary (October 2019)Document75 pagesThe Hindu Editorials Summary (October 2019)Shantanu ChauhanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Wall Paintings of IndiaDocument4 pagesWall Paintings of IndiaShantanu ChauhanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Ratios and proportions explainedDocument2 pagesRatios and proportions explainedNagaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Delimitation Exercise in Jammu and KashmirDocument12 pagesDelimitation Exercise in Jammu and KashmirShantanu ChauhanNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Home Sitemap Contact UsDocument2 pagesHome Sitemap Contact UsSachin YadavNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Standard CostingDocument65 pagesStandard CostingAmit KumarNo ratings yet

- Questions Asked in PHASE 2 RBI GRADE B 2017 - Anujjindal - inDocument7 pagesQuestions Asked in PHASE 2 RBI GRADE B 2017 - Anujjindal - inShantanu Chauhan100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Reports and Indices 2018Document31 pagesReports and Indices 2018Shantanu ChauhanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Culture Complete Notes MrunalDocument51 pagesCulture Complete Notes Mrunalamarsinha198767% (6)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Nuclear Energy - IndiaDocument6 pagesNuclear Energy - IndiaShantanu ChauhanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- How To Ace The Essay Paper - IAS RANK 292 Arushi Shares How She Managed 141Document9 pagesHow To Ace The Essay Paper - IAS RANK 292 Arushi Shares How She Managed 141Shantanu ChauhanNo ratings yet

- 1st Divyang DLDocument1 page1st Divyang DLShantanu ChauhanNo ratings yet

- Indian Currency FactsDocument2 pagesIndian Currency FactsShantanu ChauhanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Visionias Civil Services Prelims Upsc Ias 2016 Answer Solution AnalysisDocument80 pagesVisionias Civil Services Prelims Upsc Ias 2016 Answer Solution AnalysisShantanu ChauhanNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Mudra YojnaDocument2 pagesMudra YojnaShantanu ChauhanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- International OrganizationsDocument15 pagesInternational OrganizationsShantanu ChauhanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- NexavarDocument3 pagesNexavarShantanu ChauhanNo ratings yet

- 2010 Sociology GuideDocument4 pages2010 Sociology GuideShantanu ChauhanNo ratings yet

- Digital Millennium Copyright ActDocument16 pagesDigital Millennium Copyright ActShantanu ChauhanNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 26 Reasons For Sentencing Talwars in Aarushi CaseDocument3 pages26 Reasons For Sentencing Talwars in Aarushi CaseShantanu Chauhan0% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Notes The Representation of The People Act, 1951 (An Analysis)Document11 pagesNotes The Representation of The People Act, 1951 (An Analysis)Sreekanth Reddy100% (1)

- AnagramDocument7 pagesAnagramShantanu Chauhan100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Iifm BhopalDocument41 pagesIifm BhopalManish GiteNo ratings yet

- CNN IbnDocument4 pagesCNN IbnShantanu ChauhanNo ratings yet

- Project Financing and AppraisalDocument27 pagesProject Financing and AppraisalShantanu ChauhanNo ratings yet

- Capitation FeeDocument3 pagesCapitation FeeShantanu ChauhanNo ratings yet

- Retail DupontDocument8 pagesRetail DupontShantanu ChauhanNo ratings yet

- SW One DXP Cost Sheet (4.5BHK+Utility) Phase 2Document1 pageSW One DXP Cost Sheet (4.5BHK+Utility) Phase 2assetcafe7No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Adv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1Document12 pagesAdv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1ria fransiscaieNo ratings yet

- Marcopper Mining CorpDocument7 pagesMarcopper Mining CorpChristine Ivy Delos SantosNo ratings yet

- 30 Free Leed Ap BD+C Sample QuestionsDocument23 pages30 Free Leed Ap BD+C Sample QuestionsSubhranshu PandaNo ratings yet

- Agile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariDocument28 pagesAgile Development: © Lpu:: Cap437: Software Engineering Practices: Ashwani Kumar TewariAnanth KallamNo ratings yet

- Att-2.1 SowDocument5 pagesAtt-2.1 SowAgung FitrillaNo ratings yet

- 2021 Remaining Ongoing CasesDocument2,517 pages2021 Remaining Ongoing CasesJulia Mar Antonete Tamayo AcedoNo ratings yet

- Expected Questions For Business Laws For June 22 ExamsDocument8 pagesExpected Questions For Business Laws For June 22 ExamsFREEFIRE IDNo ratings yet

- Final Ruckus ProposalDocument29 pagesFinal Ruckus Proposalapi-609740598No ratings yet

- Centrelink Authorisation Form ss313 - 1005enDocument6 pagesCentrelink Authorisation Form ss313 - 1005enWilliam Alister Young0% (1)

- Financial Statements British English Student Ver2Document4 pagesFinancial Statements British English Student Ver2Paulo AbrantesNo ratings yet

- Recovery and Resilience TRACC 1356Document12 pagesRecovery and Resilience TRACC 1356JESUS JUAREZ PEÑUELANo ratings yet

- 00 AY 2022-2023 CA51027 Accounting For Government and Non-Profit Organizations REVISED COURSE PLAN DUE To COVID 19 PANDEMICDocument8 pages00 AY 2022-2023 CA51027 Accounting For Government and Non-Profit Organizations REVISED COURSE PLAN DUE To COVID 19 PANDEMICJaimellNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Free GameDocument1 pageFree GameSC AyuburiNo ratings yet

- RBI's Vital Role in Regulating India's Economy and Financial SystemDocument2 pagesRBI's Vital Role in Regulating India's Economy and Financial SystemSimran hreraNo ratings yet

- Barangay transparency monitoring form titleDocument1 pageBarangay transparency monitoring form titleOmar Dizon100% (1)

- Urban MarketplaceDocument20 pagesUrban MarketplaceMae LafortezaNo ratings yet

- Equity CrowdfundingDocument13 pagesEquity CrowdfundingantonyNo ratings yet

- Yatra Online Private LimitedDocument2 pagesYatra Online Private LimitedAkhilesh kumar SrivastavaNo ratings yet

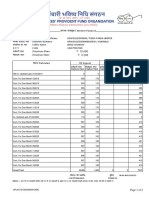

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Understanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassDocument24 pagesUnderstanding Cryptocurrencies: Bitcoin, Ethereum, and Altcoins As An Asset ClassCharlene KronstedtNo ratings yet

- SAP NetWeaver WAS Administration TrainingDocument8 pagesSAP NetWeaver WAS Administration Trainingchaduvula1995No ratings yet

- Tax Invoice DetailsDocument2 pagesTax Invoice Detailsquality fluconNo ratings yet

- Experienced Hospitality Professional Seeking New OpportunitiesDocument2 pagesExperienced Hospitality Professional Seeking New OpportunitiesValeria SpasovaNo ratings yet

- Max AR Final 130812 PDFDocument731 pagesMax AR Final 130812 PDFsnjv2621No ratings yet

- EPPM4014 Final - A168245 Nur Alifah Binti Abu SafianDocument3 pagesEPPM4014 Final - A168245 Nur Alifah Binti Abu SafianMOHAMAD FAIZAL BIN SULAIMANNo ratings yet

- The Air Rules 1982Document20 pagesThe Air Rules 1982visutsiNo ratings yet

- Cost Accounting: Level 3Document19 pagesCost Accounting: Level 3Hein Linn Kyaw100% (1)

- Cbse Cost Accounting NotesDocument154 pagesCbse Cost Accounting NotesMANDHAPALLY MANISHANo ratings yet

- Whirlpool 4 in 1 Convertible Cooling 1.5 Ton 3 Star Split Inverter AC - WhiteDocument2 pagesWhirlpool 4 in 1 Convertible Cooling 1.5 Ton 3 Star Split Inverter AC - WhiteAquib ezazNo ratings yet