You might also like

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Income Tax Law-Gct-1: Faculty of Law, Aligarh Muslim UniversityDocument9 pagesIncome Tax Law-Gct-1: Faculty of Law, Aligarh Muslim UniversityshivamNo ratings yet

- Part - III: History of Taxation in IndiaDocument13 pagesPart - III: History of Taxation in IndiaAbhi TripathiNo ratings yet

- PreliminaryDocument59 pagesPreliminaryAkanksha BohraNo ratings yet

- Mutius SlidesCarnivalDocument10 pagesMutius SlidesCarnivalAdib RahmanNo ratings yet

- Module 1Document73 pagesModule 1rajlaxmi swainNo ratings yet

- ITAT Appeal Procedure FunctionsDocument4 pagesITAT Appeal Procedure FunctionsRuhul AminNo ratings yet

- DT NotesDocument434 pagesDT NotesAnushka BiswasNo ratings yet

- Study Note - 2Document1 pageStudy Note - 2s4sahithNo ratings yet

- INCOME TAX NOTES 3 BASIC CONCEPTSpdfDocument18 pagesINCOME TAX NOTES 3 BASIC CONCEPTSpdfIshitaNo ratings yet

- Taxation - E-Notes - Udesh Regular - Group 1Document34 pagesTaxation - E-Notes - Udesh Regular - Group 1Uday TomarNo ratings yet

- BUSL320 - Mid Semester Exam StudyDocument4 pagesBUSL320 - Mid Semester Exam StudyAfaan Shakeeb0% (1)

- Income Tax Authorities Powers and DutiesDocument16 pagesIncome Tax Authorities Powers and Dutiesnandan velankarNo ratings yet

- Madras Bar Association v. Union of India & Anr.Document270 pagesMadras Bar Association v. Union of India & Anr.Bar & Bench100% (2)

- BC0150036. Direct TaxactionDocument11 pagesBC0150036. Direct TaxactionVIVEKANANDAN JVNo ratings yet

- Basics of Income TaxDocument15 pagesBasics of Income Taxdevi sreeNo ratings yet

- Taxation Law Project.1642Document12 pagesTaxation Law Project.1642Liya FathimaNo ratings yet

- Appeals and Procedure For Filing Appeals 2018Document69 pagesAppeals and Procedure For Filing Appeals 2018Chaithanya RajuNo ratings yet

- Income Tax Complete - E-Notes - Udesh Regular - Group 1Document250 pagesIncome Tax Complete - E-Notes - Udesh Regular - Group 1Uday Tomar100% (1)

- Aseem Chawla - Tax Disputes in IndiaDocument14 pagesAseem Chawla - Tax Disputes in IndiaJayaprakash PeriyasamyNo ratings yet

- Origin, History of Taxation in IndiaDocument3 pagesOrigin, History of Taxation in IndiastudywagishaNo ratings yet

- Taxation Law FDDocument15 pagesTaxation Law FDAyesha ThakurNo ratings yet

- Case Brief of Taxation Law by NidhiDocument5 pagesCase Brief of Taxation Law by Nidhinidhi gopakumarNo ratings yet

- I - A I T A, 1961: Ncome TAX Uthorities Under Ncome AX CTDocument6 pagesI - A I T A, 1961: Ncome TAX Uthorities Under Ncome AX CTAVNISH PRAKASHNo ratings yet

- Income TaxDocument100 pagesIncome TaxDr Sachin Chitnis M O UPHC AiroliNo ratings yet

- Court of Tax Appeals of The PhilippinesDocument14 pagesCourt of Tax Appeals of The Philippinesjohn vidadNo ratings yet

- Concept and Framework of TaxationDocument16 pagesConcept and Framework of Taxationanandbm1231750No ratings yet

- History of Tax in PakistanDocument19 pagesHistory of Tax in PakistanSaimSafdar50% (2)

- Powers of IT AuthoritiesDocument21 pagesPowers of IT AuthoritiesRishika JainNo ratings yet

- DTP Full NotesDocument114 pagesDTP Full NotesCHAITHRANo ratings yet

- Direct Tax NotesDocument65 pagesDirect Tax NotesJeevan T RNo ratings yet

- Income Tax Notes - All 5 ChaptersDocument78 pagesIncome Tax Notes - All 5 ChaptersWahid bhatNo ratings yet

- ITO 2001 Industrial Relation Workman Compenstation Standing OrdersDocument74 pagesITO 2001 Industrial Relation Workman Compenstation Standing OrdersAsfandyar KhanNo ratings yet

- Can Aspect Theory Justify Overlapping of Central and State Taxes: A Critical OverviewDocument5 pagesCan Aspect Theory Justify Overlapping of Central and State Taxes: A Critical OverviewDwaipayan BanerjeeNo ratings yet

- Central Sales Tax Act, 1956: An Assignment OnDocument10 pagesCentral Sales Tax Act, 1956: An Assignment OnDezyne EcoleNo ratings yet

- Law of Taxation PDFDocument24 pagesLaw of Taxation PDFwingpa delacruzNo ratings yet

- Tax Disputes and LitigationDocument3 pagesTax Disputes and LitigationABHISHEK PARMARNo ratings yet

- 35, Kumar Raghva, Taxation, Final DraftDocument18 pages35, Kumar Raghva, Taxation, Final DraftRama KamalNo ratings yet

- Taxation Laws in IndiaDocument16 pagesTaxation Laws in IndiaAnushka SharmaNo ratings yet

- Tax Litigation in India OverviewDocument38 pagesTax Litigation in India Overviewsarthak mohan shuklaNo ratings yet

- Tax Litigation in India OverviewDocument38 pagesTax Litigation in India Overviewsarthak mohan shuklaNo ratings yet

- Chapter - 1 - Income TaxDocument8 pagesChapter - 1 - Income TaxYaksha AllolaNo ratings yet

- History of Income TaxDocument2 pagesHistory of Income TaxcasapnaNo ratings yet

- Retrospective Taxation - The Indian ExperienceDocument18 pagesRetrospective Taxation - The Indian ExperienceBrijbhan Singh RajawatNo ratings yet

- Basic Concepts: 1.1 What Is A Tax?Document31 pagesBasic Concepts: 1.1 What Is A Tax?sourav kumar rayNo ratings yet

- Answer Book Tax 2Document25 pagesAnswer Book Tax 2vinita choudharyNo ratings yet

- Appeal and Revision in Income Tax ActDocument32 pagesAppeal and Revision in Income Tax ActVaishnavi CNo ratings yet

- Basic Concepts - E-Notes - PDF OnlyDocument42 pagesBasic Concepts - E-Notes - PDF Onlyprajwalthakre2No ratings yet

- Taxation Law AssignmentDocument10 pagesTaxation Law AssignmentkrnNo ratings yet

- Income Tax AuthoritiesDocument12 pagesIncome Tax AuthoritiesRuhul AminNo ratings yet

- ExciseDocument199 pagesExciseSubashVenkataramNo ratings yet

- Amnisty For Tax and Custom DutiesDocument12 pagesAmnisty For Tax and Custom DutieserishysiNo ratings yet

- Bos 54380 CP 1Document53 pagesBos 54380 CP 1Deepak AsokanNo ratings yet

- Cp1 - Bsaic ConceptsDocument53 pagesCp1 - Bsaic Conceptsh.b. akshayaNo ratings yet

- Taxation - 6 SemesterDocument28 pagesTaxation - 6 SemesterKhalid123No ratings yet

- Income Tax Reform IndiaDocument17 pagesIncome Tax Reform IndiaGagan SinghNo ratings yet

- NotesDocument9 pagesNotesYaalesh BajajNo ratings yet

- 1.0 Introduction AY2022-23Document34 pages1.0 Introduction AY2022-23namanNo ratings yet

- Indonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaFrom EverandIndonesian Taxation: for Academics and Foreign Business Practitioners Doing Business in IndonesiaNo ratings yet

- SSRN Id2404797Document10 pagesSSRN Id2404797shivamNo ratings yet

- rf80857 Af84592 PDFDocument159 pagesrf80857 Af84592 PDFkartikeya gulatiNo ratings yet

- s815035 AbstractDocument22 pagess815035 Abstractkartikeya gulatiNo ratings yet

- AJZ2018b PDFDocument22 pagesAJZ2018b PDFEva WilsonNo ratings yet

- F 780Document53 pagesF 780kartikeya gulatiNo ratings yet

- Issues Challenges and Problems With Tax Evasion TH PDFDocument21 pagesIssues Challenges and Problems With Tax Evasion TH PDFkartikeya gulatiNo ratings yet

- Determinants of Tax Evasion in The Developing Economies: A Structural Equation Model Approach of The Case of GhanaDocument11 pagesDeterminants of Tax Evasion in The Developing Economies: A Structural Equation Model Approach of The Case of GhanaAbdu MohammedNo ratings yet

- Tax Avoidance, Human Capital Accumulation and Economic GrowthDocument25 pagesTax Avoidance, Human Capital Accumulation and Economic Growthkartikeya gulatiNo ratings yet

- Tax Avoidance, Human Capital Accumulation and Economic GrowthDocument20 pagesTax Avoidance, Human Capital Accumulation and Economic Growthkartikeya gulatiNo ratings yet

- s815035 AbstractDocument22 pagess815035 Abstractkartikeya gulatiNo ratings yet

- Tax Avoidance Versus Tax Evasion On Some PDFDocument14 pagesTax Avoidance Versus Tax Evasion On Some PDFkartikeya gulatiNo ratings yet

- Determining "Likeness" Under The GATS: Squaring The Circle?: Economic Research and Statistics DivisionDocument53 pagesDetermining "Likeness" Under The GATS: Squaring The Circle?: Economic Research and Statistics DivisionPrem KumarNo ratings yet

- Tax Evasion and Economic Growth PDFDocument27 pagesTax Evasion and Economic Growth PDFkartikeya gulatiNo ratings yet

- ND PDFDocument45 pagesND PDFkartikeya gulatiNo ratings yet

- Ersd200801 e PDFDocument37 pagesErsd200801 e PDFkartikeya gulatiNo ratings yet

- Gatt1994 Art14 Gatt47 PDFDocument9 pagesGatt1994 Art14 Gatt47 PDFkartikeya gulatiNo ratings yet

- Wto Analytical Index: 1 Article Xix 1.1 Text of Article XIXDocument20 pagesWto Analytical Index: 1 Article Xix 1.1 Text of Article XIXkartikeya gulatiNo ratings yet

- Legitimate Expectations - Interpretation of Tariff Concessions in Article IiDocument8 pagesLegitimate Expectations - Interpretation of Tariff Concessions in Article Iikartikeya gulatiNo ratings yet

- QR PDFDocument10 pagesQR PDFkartikeya gulatiNo ratings yet

- 4qeppart4 PDFDocument16 pages4qeppart4 PDFAasthaNo ratings yet

- GATTDocument93 pagesGATTGeeta KhobreakrNo ratings yet

- Zeroing in Anti Dumping PDFDocument27 pagesZeroing in Anti Dumping PDFkartikeya gulatiNo ratings yet

- 09 - Chapter 3 PDFDocument50 pages09 - Chapter 3 PDFkartikeya gulatiNo ratings yet

- An Analysis of WTO & GATT PDFDocument12 pagesAn Analysis of WTO & GATT PDFLiezel SundiamNo ratings yet

- Unforeseen Developments - Safeguards PDFDocument14 pagesUnforeseen Developments - Safeguards PDFkartikeya gulatiNo ratings yet

- From GATT To WTO and BeyondDocument65 pagesFrom GATT To WTO and BeyondFaiz AhmedNo ratings yet

- Agreement On Safeguards - Commentary PDFDocument32 pagesAgreement On Safeguards - Commentary PDFkartikeya gulatiNo ratings yet

- QR PDFDocument10 pagesQR PDFkartikeya gulatiNo ratings yet

- Agreement On SafeguardsDocument9 pagesAgreement On SafeguardsasifanisNo ratings yet

- Jurnal GCG MankeuDocument10 pagesJurnal GCG Mankeubudhi suryanto100% (1)

- #42 - Ador v. Jamila and Co.Document1 page#42 - Ador v. Jamila and Co.Kê MilanNo ratings yet

- Motion To Reconsider 3 14 FinalDocument14 pagesMotion To Reconsider 3 14 FinalJamil B. AsumNo ratings yet

- United States v. Arsalan Nosrati, 51 F.3d 269, 4th Cir. (1995)Document5 pagesUnited States v. Arsalan Nosrati, 51 F.3d 269, 4th Cir. (1995)Scribd Government DocsNo ratings yet

- Taruc vs. Dela CruzDocument1 pageTaruc vs. Dela CruzKP DAVAO CITYNo ratings yet

- 007 Security ManagementDocument13 pages007 Security ManagementShibu ArjunanNo ratings yet

- Advertisements: Philippine Law ReviewersDocument20 pagesAdvertisements: Philippine Law ReviewersJexelle Marteen Tumibay PestañoNo ratings yet

- Section 3 of The CBA Reads: The Company Agrees To Require As A Condition ofDocument3 pagesSection 3 of The CBA Reads: The Company Agrees To Require As A Condition ofMigs GayaresNo ratings yet

- Digested Case in Transportation Law Gatchalian vs. CADocument3 pagesDigested Case in Transportation Law Gatchalian vs. CASerneiv YrrejNo ratings yet

- BIGAMYDocument25 pagesBIGAMYKherry LoNo ratings yet

- PP vs. GravilDocument9 pagesPP vs. GravilBea CapeNo ratings yet

- Comsavings Bank Vs Sps. CapistranoDocument1 pageComsavings Bank Vs Sps. CapistranoJean UcolNo ratings yet

- Filipino Parents of LGBT in The Lens of Global Sustainability and Climate Justice Dissecting Filipino Values As Engage in Environmental EthicsDocument2 pagesFilipino Parents of LGBT in The Lens of Global Sustainability and Climate Justice Dissecting Filipino Values As Engage in Environmental EthicsKay Santos FernandezNo ratings yet

- AZUELA v. CA Case DigestDocument2 pagesAZUELA v. CA Case DigestNOLLIE CALISING100% (2)

- rightsED Tackling Sexual Harassment PDFDocument29 pagesrightsED Tackling Sexual Harassment PDFLukepouNo ratings yet

- Bridge Leases Contract, Property, & StatusDocument17 pagesBridge Leases Contract, Property, & StatusAaron Goh100% (1)

- Memorial - Case of Article 21,19,14Document13 pagesMemorial - Case of Article 21,19,14chetan gwalioryjain64% (14)

- Letter To KARE-11 TV - October 2015 Gun Control DebateDocument2 pagesLetter To KARE-11 TV - October 2015 Gun Control DebateBryan StrawserNo ratings yet

- General Remedies in TortDocument41 pagesGeneral Remedies in TortOJASWANI DIXITNo ratings yet

- PR Mallya Nirav and MehulfinalDocument2 pagesPR Mallya Nirav and Mehulfinalshivani shindeNo ratings yet

- Francisco Motors Corp. v. Court of Appeals, 309 SCRA 72 (1999)Document23 pagesFrancisco Motors Corp. v. Court of Appeals, 309 SCRA 72 (1999)inno KalNo ratings yet

- Trans 1 PDFDocument238 pagesTrans 1 PDFMichaelCorbin100% (1)

- OCA vs. Judge FloroDocument7 pagesOCA vs. Judge Florocatrina lobatonNo ratings yet

- Supreme Court E-Library: Information at Your FingertipsDocument15 pagesSupreme Court E-Library: Information at Your FingertipsGabriel EmersonNo ratings yet

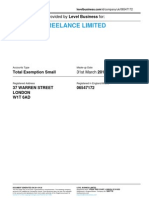

- BROWNIE FREELANCE LIMITED - Company Accounts From Level BusinessDocument5 pagesBROWNIE FREELANCE LIMITED - Company Accounts From Level BusinessLevel BusinessNo ratings yet

- Alto-Yap Vs GanDocument3 pagesAlto-Yap Vs GanMia Dela CruzNo ratings yet

- Final Draft AsianDocument7 pagesFinal Draft Asianapi-295691859No ratings yet

- Peralta Vs CSCDocument7 pagesPeralta Vs CSCJanette SumagaysayNo ratings yet

- Fue Leung v. IACDocument2 pagesFue Leung v. IAClealdeosaNo ratings yet

- Kasinatian Sa Bukid (A3)Document19 pagesKasinatian Sa Bukid (A3)Llpdc NociNo ratings yet