You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Reviewer ToaDocument25 pagesReviewer ToaFlorence CuansoNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- FINALFederal Civil ProcedureDocument63 pagesFINALFederal Civil Procedurekashitampo0% (1)

- KP - Procedure, Execution, CasesDocument10 pagesKP - Procedure, Execution, CasesMarie AlejoNo ratings yet

- Immigration Law OutlineDocument53 pagesImmigration Law OutlineIan Quin100% (1)

- Finman3 Report DiscussionDocument5 pagesFinman3 Report DiscussionFlorence CuansoNo ratings yet

- AP 5904Q InvestmentsDocument14 pagesAP 5904Q InvestmentsFlorence CuansoNo ratings yet

- 00 Table of ContentsDocument10 pages00 Table of ContentsFlorence CuansoNo ratings yet

- Practical Accounting 2 With AnswersDocument13 pagesPractical Accounting 2 With AnswersFlorence CuansoNo ratings yet

- Chapter 8 Internal Control and CBISDocument9 pagesChapter 8 Internal Control and CBISFlorence CuansoNo ratings yet

- CH 10Document11 pagesCH 10Florence CuansoNo ratings yet

- CHAPTER 21 - Investment in Equity SecuritiesDocument8 pagesCHAPTER 21 - Investment in Equity SecuritiesFlorence CuansoNo ratings yet

- April D. Chandler v. Volunteers of America, 11th Cir. (2015)Document29 pagesApril D. Chandler v. Volunteers of America, 11th Cir. (2015)Scribd Government DocsNo ratings yet

- Chavez V. Public Estates Authority 384 SCRA 152: FactsDocument15 pagesChavez V. Public Estates Authority 384 SCRA 152: FactsSalma GurarNo ratings yet

- Census PDFDocument31 pagesCensus PDFAnonymous TwMZy5lNo ratings yet

- 50 People Vs Suarez, G.R. No. 111193. January 28, 1997Document6 pages50 People Vs Suarez, G.R. No. 111193. January 28, 1997Perry YapNo ratings yet

- Senator Tolentino Privilege SpeechDocument5 pagesSenator Tolentino Privilege SpeechGARCIA, AxlNo ratings yet

- Government Auditing Standards Amendment IIDocument74 pagesGovernment Auditing Standards Amendment IISahil AsimNo ratings yet

- 1 Condidional Acceptance IRS 3176C VerdanaDocument6 pages1 Condidional Acceptance IRS 3176C VerdanaKenneth Michael DeLashmuttNo ratings yet

- Apex Court of IndiaDocument2 pagesApex Court of IndiaRajeevNo ratings yet

- Can A Contractor Claim For Loss of Profit On Omitted WorksDocument2 pagesCan A Contractor Claim For Loss of Profit On Omitted WorksMdms Payoe100% (1)

- Public International Law & Human RightsDocument37 pagesPublic International Law & Human RightsVenkata Ramana100% (3)

- Conflict & Cooperation ReadingsDocument2 pagesConflict & Cooperation Readingsapi-261009456No ratings yet

- Department of Labor: MALJ CHAPTER A03Document27 pagesDepartment of Labor: MALJ CHAPTER A03USA_DepartmentOfLaborNo ratings yet

- At The End of World War II - BeginningDocument2 pagesAt The End of World War II - BeginningSuryaNo ratings yet

- Applying For A National Insurance NumbeDocument2 pagesApplying For A National Insurance NumbegrungeshoesNo ratings yet

- E-Ticket Inet Ref 246091 Booking Ref 184236 Online Ref 232532 PNR M9B74A Inv No 174857Document16 pagesE-Ticket Inet Ref 246091 Booking Ref 184236 Online Ref 232532 PNR M9B74A Inv No 174857Aditya YadavNo ratings yet

- Failure To File Pre-Trial BriefDocument4 pagesFailure To File Pre-Trial BriefattymelNo ratings yet

- Choose A Legal Structure For Your Business 6Document11 pagesChoose A Legal Structure For Your Business 6vidrascuNo ratings yet

- Plopenio v. DAR DigestDocument2 pagesPlopenio v. DAR Digestdeguia2340027No ratings yet

- DEED OF ABSOLUTE SALE - SampleDocument2 pagesDEED OF ABSOLUTE SALE - SampleRoland Rosales100% (1)

- G.O 46 Dt. 01.06.2016Document7 pagesG.O 46 Dt. 01.06.2016gchatlaNo ratings yet

- Rishi DrdoDocument4 pagesRishi DrdoRishikesh MeenaNo ratings yet

- Job Applicant Rejection LetterDocument3 pagesJob Applicant Rejection LettercynyoNo ratings yet

- Javier Ortiz Villegas, A200 975 995 (BIA July 1, 2016)Document4 pagesJavier Ortiz Villegas, A200 975 995 (BIA July 1, 2016)Immigrant & Refugee Appellate Center, LLC100% (1)

- Sagrado Orden de Precadores v. NacocoDocument6 pagesSagrado Orden de Precadores v. NacocojNo ratings yet

- Legal Forms PretestDocument7 pagesLegal Forms PretestMichael MatnaoNo ratings yet

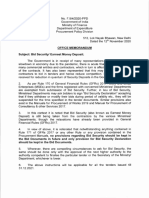

- Bid Security - Earnest Money Deposit PDFDocument2 pagesBid Security - Earnest Money Deposit PDFSaurabh KumarNo ratings yet

- London Diplomatic List - May 2023Document140 pagesLondon Diplomatic List - May 2023Ali ZilbermanNo ratings yet