You might also like

- Coins of England & the United Kingdom (2021): Decimal IssuesFrom EverandCoins of England & the United Kingdom (2021): Decimal IssuesEmma HowardNo ratings yet

- Kristine Jae D. Neri Bse 1B: I. True or FalseDocument5 pagesKristine Jae D. Neri Bse 1B: I. True or FalseKristine NeriNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Accounting For Sales PDFDocument20 pagesAccounting For Sales PDFJasmine Acta100% (1)

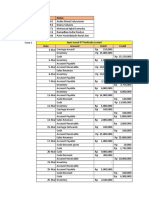

- 20 Transaction of Car BusinessDocument5 pages20 Transaction of Car BusinessPak EntertainmentNo ratings yet

- (IFA 8) - Rendy Filiang - 1402210324Document15 pages(IFA 8) - Rendy Filiang - 1402210324RENDY FILIANGNo ratings yet

- Chapter (1) The Accounting EquationDocument46 pagesChapter (1) The Accounting Equationtunlinoo.067433100% (3)

- 38209025-Grace Fidelia-Akuntansi Keuangan Dasar 1-Eksekutif AkuntansiDocument10 pages38209025-Grace Fidelia-Akuntansi Keuangan Dasar 1-Eksekutif AkuntansiGrace FideliaNo ratings yet

- Inv AudDocument32 pagesInv AudAud Balanzi100% (1)

- Accounting CycleDocument24 pagesAccounting Cycletalha ShakeelNo ratings yet

- Chapter 5 Caselette Audit of InventoryDocument33 pagesChapter 5 Caselette Audit of InventoryAnna Taylor100% (1)

- Accounting CycleDocument3 pagesAccounting Cycletalha ShakeelNo ratings yet

- Week 5 6 Adjusting Entries Second Quarter Fabm2 Pythagoras and EuclidDocument2 pagesWeek 5 6 Adjusting Entries Second Quarter Fabm2 Pythagoras and EuclidCyrus Jhun OfrinNo ratings yet

- Journal Entries Groupings AccountingDocument3 pagesJournal Entries Groupings AccountingGerlyn Mae Delantar100% (1)

- Answers To Review Questions Volume 1 - Chapter 4: CapitalDocument5 pagesAnswers To Review Questions Volume 1 - Chapter 4: CapitalRehman BilalNo ratings yet

- TK1 Team3Document22 pagesTK1 Team3Andra Cie Cee CawNo ratings yet

- TK03 Aks Liana DamayantiDocument7 pagesTK03 Aks Liana DamayantiLiana DamayantiNo ratings yet

- Audit-of-Inventory Homework AnswersDocument5 pagesAudit-of-Inventory Homework AnswersMarnelli Catalan100% (1)

- Cash BooksDocument13 pagesCash BooksWanjala RajabNo ratings yet

- Andrew AngDocument3 pagesAndrew AngShane Kimberly LubatNo ratings yet

- Audit of Inventory: Download NowDocument1 pageAudit of Inventory: Download NowMariz Julian Pang-aoNo ratings yet

- Module 2 - Caragan, Adriane Ronn B. (CORRESPONDENCE)Document6 pagesModule 2 - Caragan, Adriane Ronn B. (CORRESPONDENCE)WonnNo ratings yet

- A. Journalize The Transactions Using A Perpetual Inventory System. Date Accounts Debit CreditDocument5 pagesA. Journalize The Transactions Using A Perpetual Inventory System. Date Accounts Debit CreditMinh Anh NguyễnNo ratings yet

- Accounting Revision QuestionsDocument8 pagesAccounting Revision QuestionsFranswa MateteNo ratings yet

- Initial InvestmentDocument18 pagesInitial InvestmentLyca Mae Cubangbang100% (3)

- Accounting For EngineersDocument7 pagesAccounting For EngineersHoorain SajjadNo ratings yet

- Name: Exercise: Exercise 8-5, Recording Bad Debts Course: Acc 422 DateDocument6 pagesName: Exercise: Exercise 8-5, Recording Bad Debts Course: Acc 422 DateHelping Five (H5)No ratings yet

- Tugas Accounting PDFDocument1 pageTugas Accounting PDFjocelinNo ratings yet

- ActivityDocument4 pagesActivityDom PaciaNo ratings yet

- Tagamabja-Cfas Module 1Document15 pagesTagamabja-Cfas Module 1Berlyn Joy TagamaNo ratings yet

- Accounts Payable - CreditDocument4 pagesAccounts Payable - CreditJabonJohnKennethNo ratings yet

- Suggested Solution: Balance Sheet Beg End Beg EndDocument8 pagesSuggested Solution: Balance Sheet Beg End Beg EndSerien SeaNo ratings yet

- Bits and Pieces LTDDocument1 pageBits and Pieces LTDAndrea SalazarNo ratings yet

- Assignment 2Document13 pagesAssignment 2Lyca Mae Cubangbang100% (2)

- Questions Relating To Calculations in Question 1Document3 pagesQuestions Relating To Calculations in Question 1Liliana CiuraruNo ratings yet

- Accounting For Merchandising Operations ExercisesDocument4 pagesAccounting For Merchandising Operations ExercisesthachuuuNo ratings yet

- ACC111 Project Ram WholesaleDocument42 pagesACC111 Project Ram WholesaleHashimRazaNo ratings yet

- Q - Part CDocument5 pagesQ - Part CTrần Thu TrangNo ratings yet

- d4 Question Bank For Web 1 1 PDFDocument60 pagesd4 Question Bank For Web 1 1 PDFBarun Kumar SinghNo ratings yet

- Employee Id Employee Campaign Designation 1St Pay 2Nd PayDocument6 pagesEmployee Id Employee Campaign Designation 1St Pay 2Nd PayDan SoroteNo ratings yet

- Technical EnglishDocument3 pagesTechnical EnglishNicole AngomasNo ratings yet

- Preeti FileDocument7 pagesPreeti Fileravinder pal singhNo ratings yet

- Soal 1 Dan WDocument1 pageSoal 1 Dan WFirdausNo ratings yet

- Journal Entries and Adjusting EntriesDocument3 pagesJournal Entries and Adjusting EntriesGarp BarrocaNo ratings yet

- Ebin Belderol TB and WorksheetDocument11 pagesEbin Belderol TB and WorksheetMarielle Ebin100% (3)

- The Hospitality Business ToolkitDocument18 pagesThe Hospitality Business ToolkitOanaa Coman100% (1)

- M SamiDocument5 pagesM SamiMah rukh M.yaqoobNo ratings yet

- Steve Austine de OcampoDocument33 pagesSteve Austine de OcampoJamaica MoralejaNo ratings yet

- Practice SetDocument100 pagesPractice SetZamantha Oliveros100% (1)

- Cima Edition 15 Worksheet CASH FLOWDocument3 pagesCima Edition 15 Worksheet CASH FLOWananditaNo ratings yet

- AISAE 101 - Assessment 5 - Morales Mariel MaeDocument6 pagesAISAE 101 - Assessment 5 - Morales Mariel MaeMariel Mae MoralesNo ratings yet

- Homework On Inventories: Problem 1Document3 pagesHomework On Inventories: Problem 1Amy SpencerNo ratings yet

- 9 Fundamentals of Accounting December 2019Document5 pages9 Fundamentals of Accounting December 2019Suhail AhmedNo ratings yet

- Module I Basic AccountingDocument11 pagesModule I Basic Accountingpaul amo100% (1)

- Activity Sheet 5.1 FINAL 1Document4 pagesActivity Sheet 5.1 FINAL 1Francine Anne NalicatNo ratings yet

- Salsse Roofing Services Was Formed On December 01, 2016. The Following Transactions TookDocument7 pagesSalsse Roofing Services Was Formed On December 01, 2016. The Following Transactions TookDipika tasfannum salamNo ratings yet

- Bba Ii Semester Bba204B21: Financial Accounting Time: 2 Hours Max. Marks: 70Document3 pagesBba Ii Semester Bba204B21: Financial Accounting Time: 2 Hours Max. Marks: 70S Sumaiya SamrinNo ratings yet

- Latihan Kasus - Application of Perpetual Vs Periodic System 2110111041 - Frisca AprilliaDocument8 pagesLatihan Kasus - Application of Perpetual Vs Periodic System 2110111041 - Frisca AprilliawibuNo ratings yet

- Siti Nur Apriyani - 2009102 - PAK-7A - Tugas 3 AKHOSDocument5 pagesSiti Nur Apriyani - 2009102 - PAK-7A - Tugas 3 AKHOSS Nur ApriyaniNo ratings yet

- Option A $51,000. Beginning Balance $ 53,000 Less: Uncollectibles $ - 2,000 Ending Balance $ 51,000Document3 pagesOption A $51,000. Beginning Balance $ 53,000 Less: Uncollectibles $ - 2,000 Ending Balance $ 51,000mohitgaba19No ratings yet

- Statements of Financial Position As at 31 December 2009 and 2010Document3 pagesStatements of Financial Position As at 31 December 2009 and 2010mohitgaba19No ratings yet

- QDocument4 pagesQmohitgaba19No ratings yet

- 4299259Document7 pages4299259mohitgaba19No ratings yet

- The Following Information Is Available For Bakers CorporationDocument3 pagesThe Following Information Is Available For Bakers Corporationmohitgaba19No ratings yet

- Wakeland Community Hospital Statement of Operations For The Years Ended December 31, 20X1 and 20X0 (In Thousands) Particulars RevenuesDocument10 pagesWakeland Community Hospital Statement of Operations For The Years Ended December 31, 20X1 and 20X0 (In Thousands) Particulars Revenuesmohitgaba19100% (1)

- 321772Document3 pages321772mohitgaba19No ratings yet

- True / False QuestionsDocument3 pagesTrue / False Questionsmohitgaba19No ratings yet

- Financial Break-Even L.J.'s Toys Just Purchased A 200,000 Machine To Produce Toy CarsDocument1 pageFinancial Break-Even L.J.'s Toys Just Purchased A 200,000 Machine To Produce Toy Carsmohitgaba19No ratings yet

- RequiredDocument2 pagesRequiredmohitgaba19No ratings yet

- Whole Unit % EUP-material Beginning Work in Process Unit Started and Completed Ending Work in Process Total Equivalent UnitDocument3 pagesWhole Unit % EUP-material Beginning Work in Process Unit Started and Completed Ending Work in Process Total Equivalent Unitmohitgaba19No ratings yet

- 2811501Document12 pages2811501mohitgaba19100% (1)

- InstructionsDocument4 pagesInstructionsmohitgaba19No ratings yet

- InstructionsDocument3 pagesInstructionsmohitgaba19No ratings yet

- 2944021Document3 pages2944021mohitgaba19No ratings yet

- Answer 3Document4 pagesAnswer 3mohitgaba19No ratings yet

- 641139Document3 pages641139mohitgaba19No ratings yet

- 3271010Document4 pages3271010mohitgaba19No ratings yet

- 552748Document3 pages552748mohitgaba19No ratings yet

- Carlos CompanyDocument5 pagesCarlos Companymohitgaba19No ratings yet

- 648235Document5 pages648235mohitgaba19No ratings yet

- Catalogue of Palaearctic Coleoptera Vol.4 2007Document471 pagesCatalogue of Palaearctic Coleoptera Vol.4 2007asmodeus822No ratings yet

- Nurse Education Today: Natalie M. Agius, Ann WilkinsonDocument8 pagesNurse Education Today: Natalie M. Agius, Ann WilkinsonSobiaNo ratings yet

- Network Tools and Protocols Lab 2: Introduction To Iperf3Document17 pagesNetwork Tools and Protocols Lab 2: Introduction To Iperf3Fabio MenesesNo ratings yet

- National Industrial Policy 2010 (Bangla)Document46 pagesNational Industrial Policy 2010 (Bangla)Md.Abdulla All Shafi0% (1)

- Thermo Scientific 49iq: Ozone Analyzer-UV PhotometricDocument2 pagesThermo Scientific 49iq: Ozone Analyzer-UV PhotometricAnish KarthikeyanNo ratings yet

- Sow and Learning ObjectivesDocument14 pagesSow and Learning ObjectivesEhsan AzmanNo ratings yet

- 2022+ACCF+111+Class+test+2 Moderated+versionDocument8 pages2022+ACCF+111+Class+test+2 Moderated+versionLucas LuluNo ratings yet

- Fulltext PDFDocument454 pagesFulltext PDFVirmantas JuoceviciusNo ratings yet

- Iecex Bas 13.0069XDocument4 pagesIecex Bas 13.0069XFrancesco_CNo ratings yet

- Installation ManualDocument16 pagesInstallation ManualJosé Manuel García MartínNo ratings yet

- Paper Cutting 6Document71 pagesPaper Cutting 6Vidya AdsuleNo ratings yet

- 4th - STD - MM - Kerala Reader Malayalam Vol 1Document79 pages4th - STD - MM - Kerala Reader Malayalam Vol 1Rajsekhar GNo ratings yet

- Transcendental Meditaton ProgramDocument3 pagesTranscendental Meditaton Programacharyaprakash0% (3)

- Antibiotics and Their Types, Uses, Side EffectsDocument4 pagesAntibiotics and Their Types, Uses, Side EffectsSpislgal PhilipNo ratings yet

- 5EMA BB Dem&Sup VW Bu&Se - 2.35&48&PDDocument13 pages5EMA BB Dem&Sup VW Bu&Se - 2.35&48&PDkashinath09No ratings yet

- Raw:/storage/emulated/0/download/1623980378472 - 1623980347729 - PE 4 Module 2Document11 pagesRaw:/storage/emulated/0/download/1623980378472 - 1623980347729 - PE 4 Module 2Marvin Espenocilla EspeñoNo ratings yet

- New Generation of Reinforcement For Transportation Infrastructure - tcm45-590833Document5 pagesNew Generation of Reinforcement For Transportation Infrastructure - tcm45-590833RevaNo ratings yet

- Reducing Motor Vehicle Crashes in B.C.Document260 pagesReducing Motor Vehicle Crashes in B.C.Jeff NagelNo ratings yet

- EVC AC Charger CatalogDocument2 pagesEVC AC Charger CatalogRaison AutomationNo ratings yet

- English Paper 1 Mark Scheme: Cambridge Lower Secondary Sample Test For Use With Curriculum Published in September 2020Document11 pagesEnglish Paper 1 Mark Scheme: Cambridge Lower Secondary Sample Test For Use With Curriculum Published in September 2020ABEER RATHINo ratings yet

- Mucic Acid Test: PrincipleDocument3 pagesMucic Acid Test: PrincipleKrizzi Dizon GarciaNo ratings yet

- PS-8955 Zinc Alloy ElectrodepositedDocument8 pagesPS-8955 Zinc Alloy ElectrodepositedArturo Palacios100% (1)

- Canon JX 500 - 200 - Service ManualDocument154 pagesCanon JX 500 - 200 - Service ManualFritz BukowskyNo ratings yet

- Box Transport MechanismDocument36 pagesBox Transport MechanismInzi Gardezi81% (16)

- Description Features: Maximizing IC PerformanceDocument1 pageDescription Features: Maximizing IC Performanceledaurora123No ratings yet

- Mitsubishi IC Pneumatic Forklift PDFDocument5 pagesMitsubishi IC Pneumatic Forklift PDFfdpc1987No ratings yet

- Landis+Gyr Model EM5300 Class 0.5 Electricity Meter 14-2-63Document5 pagesLandis+Gyr Model EM5300 Class 0.5 Electricity Meter 14-2-63kulukundunguNo ratings yet

- LoratadinaDocument3 pagesLoratadinapapaindoNo ratings yet

- Modal Verbs EjercicioDocument2 pagesModal Verbs EjercicioAngel sosaNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- Real Life: Construction Management Guide from A-ZFrom EverandReal Life: Construction Management Guide from A-ZRating: 4.5 out of 5 stars4.5/5 (4)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- A Place of My Own: The Architecture of DaydreamsFrom EverandA Place of My Own: The Architecture of DaydreamsRating: 4 out of 5 stars4/5 (242)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Civil Engineer's Handbook of Professional PracticeFrom EverandCivil Engineer's Handbook of Professional PracticeRating: 4.5 out of 5 stars4.5/5 (2)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Pressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedFrom EverandPressure Vessels: Design, Formulas, Codes, and Interview Questions & Answers ExplainedRating: 5 out of 5 stars5/5 (1)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- The Aqua Group Guide to Procurement, Tendering and Contract AdministrationFrom EverandThe Aqua Group Guide to Procurement, Tendering and Contract AdministrationMark HackettRating: 4 out of 5 stars4/5 (1)

- Principles of Welding: Processes, Physics, Chemistry, and MetallurgyFrom EverandPrinciples of Welding: Processes, Physics, Chemistry, and MetallurgyRating: 4 out of 5 stars4/5 (1)

- The Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialFrom EverandThe Complete HVAC BIBLE for Beginners: The Most Practical & Updated Guide to Heating, Ventilation, and Air Conditioning Systems | Installation, Troubleshooting and Repair | Residential & CommercialNo ratings yet

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceFrom EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceRating: 4 out of 5 stars4/5 (1)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsFrom EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsRating: 4.5 out of 5 stars4.5/5 (2)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!From EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Rating: 4.5 out of 5 stars4.5/5 (8)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)