You might also like

- Policy Framework for Lending to Micro and Small EnterprisesDocument5 pagesPolicy Framework for Lending to Micro and Small EnterprisesdibyenduNo ratings yet

- Policy For Lending To Micro and Small EnterprisesDocument8 pagesPolicy For Lending To Micro and Small Enterprisespatruni sureshkumarNo ratings yet

- Loan Policy - ObjectivesDocument46 pagesLoan Policy - Objectivesnehamittal03No ratings yet

- Axis Bank's MSME lending policyDocument5 pagesAxis Bank's MSME lending policyhiteshmohakar15No ratings yet

- Policy Guidelines HDFCDocument3 pagesPolicy Guidelines HDFCkwangdidNo ratings yet

- Microfinance Loan Policy - SBI - 20.1.2023Document25 pagesMicrofinance Loan Policy - SBI - 20.1.2023Madhusudan ParwalNo ratings yet

- Mse Lending PolicyDocument10 pagesMse Lending PolicytanweerwarsiNo ratings yet

- 22MC894E2203DDDF4E0ABCA714DCE21F8F6CDocument63 pages22MC894E2203DDDF4E0ABCA714DCE21F8F6Caspimpale1999No ratings yet

- Institute of Management Studies Davv Indore Mba (Financial Administration) Iiird Semester - Fa 303C Insurance and Bank ManagementDocument4 pagesInstitute of Management Studies Davv Indore Mba (Financial Administration) Iiird Semester - Fa 303C Insurance and Bank ManagementjaiNo ratings yet

- Updated Loan Policy To Board 31.03.2012 Sent To Ro & ZoDocument187 pagesUpdated Loan Policy To Board 31.03.2012 Sent To Ro & ZoAbhishek BoseNo ratings yet

- ABM RBI Jul-Dec'23Document14 pagesABM RBI Jul-Dec'23RaviTuduNo ratings yet

- Credit Report On MCBDocument16 pagesCredit Report On MCBuzmabhatti34No ratings yet

- RBI Direction 25 July 2022Document13 pagesRBI Direction 25 July 2022Tender infoNo ratings yet

- CMPCir1668 13 PDFDocument38 pagesCMPCir1668 13 PDFsunilNo ratings yet

- Retail Lending Policy 2010-11Document25 pagesRetail Lending Policy 2010-11Bhandup YadavNo ratings yet

- Fair Practices Code April 2023Document4 pagesFair Practices Code April 2023devyanijain553No ratings yet

- RBI Master Circular on Management of Advances for UCBsDocument57 pagesRBI Master Circular on Management of Advances for UCBsashwini.krs80No ratings yet

- PR689DLDocument17 pagesPR689DLDirector Bal JyotiNo ratings yet

- CCP Rbi Jul-Dec'23Document21 pagesCCP Rbi Jul-Dec'23RaviTuduNo ratings yet

- Financial Management AssignmentDocument12 pagesFinancial Management AssignmentrohanpujariNo ratings yet

- Loan PolicyDocument5 pagesLoan PolicySoumya BanerjeeNo ratings yet

- PPBADocument5 pagesPPBAMANISHNo ratings yet

- Credit Management Overview and Principles of LendingDocument55 pagesCredit Management Overview and Principles of LendingShilpa Grover100% (4)

- Debt To Income RatioDocument7 pagesDebt To Income Ratioco samNo ratings yet

- Credit Management Overview and Principles of LendingDocument44 pagesCredit Management Overview and Principles of LendingTavneet Singh100% (2)

- 08 Chapter-02Document35 pages08 Chapter-02Manoj ValaNo ratings yet

- State Bank of India Co-lending Policy with NBFCsDocument11 pagesState Bank of India Co-lending Policy with NBFCspatruni sureshkumarNo ratings yet

- RBI Master Circular on Exposure Norms and Restrictions for UCBsDocument30 pagesRBI Master Circular on Exposure Norms and Restrictions for UCBssohamNo ratings yet

- 8-MM 8A-MSME FinancingDocument42 pages8-MM 8A-MSME Financingsenthamarai krishnan0% (1)

- Unit III MBF22408T Credit Risk and Recovery ManagementDocument22 pagesUnit III MBF22408T Credit Risk and Recovery ManagementSheetal DwevediNo ratings yet

- BB Loan Classification and ProvisioningDocument16 pagesBB Loan Classification and ProvisioningMuhammad Ali Jinnah100% (1)

- Credit Authorizatio N Scheme: Presented By:-Sheenu AroraDocument18 pagesCredit Authorizatio N Scheme: Presented By:-Sheenu AroraSheenu AroraNo ratings yet

- Retail Credit Card Policy 2021Document27 pagesRetail Credit Card Policy 2021Raghav SharmaNo ratings yet

- Prudential Norms ExplanationDocument4 pagesPrudential Norms ExplanationSneha ChavanNo ratings yet

- File BLG THA IL 121390Document7 pagesFile BLG THA IL 121390logicinsideNo ratings yet

- Principles of Bank Lending & Priority Sector LendingDocument22 pagesPrinciples of Bank Lending & Priority Sector LendingSheejaVarghese100% (8)

- Short Term LoansDocument4 pagesShort Term LoansHarsh MehtaNo ratings yet

- Chapter 12 Consumer BankingDocument7 pagesChapter 12 Consumer BankingSaba AmeerNo ratings yet

- Unit 8Document8 pagesUnit 8rtrsujaladhikariNo ratings yet

- Internal Control and Compliance Risk and To Compare The Existing Credit Policy of Dhaka Bank LimitedDocument22 pagesInternal Control and Compliance Risk and To Compare The Existing Credit Policy of Dhaka Bank LimitedHafiz IslamNo ratings yet

- Cash Credit System of HDFC BankDocument38 pagesCash Credit System of HDFC Bankloveleen_mangatNo ratings yet

- Bfs - Unit II Short NotesDocument12 pagesBfs - Unit II Short NotesvelmuruganbNo ratings yet

- Co LendingDocument7 pagesCo Lending22satendraNo ratings yet

- RBI Circular For FourclosureDocument58 pagesRBI Circular For FourclosureRajesh BogulNo ratings yet

- Commercial Banking in IndiaDocument32 pagesCommercial Banking in IndiaShaifali ChauhanNo ratings yet

- Compromise Settlement Scheme For Non Performing Loans Under MSE SectorDocument2 pagesCompromise Settlement Scheme For Non Performing Loans Under MSE SectorAnshul GurhaNo ratings yet

- Procedures For Credits - ALL PDFDocument165 pagesProcedures For Credits - ALL PDFIslam MongedNo ratings yet

- Credit CardsDocument26 pagesCredit CardsPranav JadavNo ratings yet

- Credit ManagementDocument503 pagesCredit ManagementGudavalli John Raja Abhishek100% (1)

- Project Report on Banking System and Credit Schemes in IndiaDocument9 pagesProject Report on Banking System and Credit Schemes in IndiamanishteensNo ratings yet

- RBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Document7 pagesRBI Master Circular Lending To Micro Small Medium Enterprises MSME Sector 2nd July 2012KALE LAW OFFICE CORPORATE LAWYER LAW FIR TAX CONSULTANTS COMPANY LAWYER 1Divya MewaraNo ratings yet

- In Case of Manufacturing Enterprises The Calculations of Original Cost ofDocument12 pagesIn Case of Manufacturing Enterprises The Calculations of Original Cost ofVimal kumarNo ratings yet

- A Study On "MSME & Credit Appraisal" With Reference To Different Credit Appraisal and Assessment System Used by United Bank of IndiaDocument16 pagesA Study On "MSME & Credit Appraisal" With Reference To Different Credit Appraisal and Assessment System Used by United Bank of IndiaHimanshiNo ratings yet

- Bajaj Finance Limited: Moratorium PolicyDocument5 pagesBajaj Finance Limited: Moratorium PolicyhariveerNo ratings yet

- Sanaul - CECM 4th - Assignment 1Document6 pagesSanaul - CECM 4th - Assignment 1Sanaul Faisal100% (1)

- Manual SmeDocument636 pagesManual SmeSiddhesh SatputeNo ratings yet

- Project Report "Banking System" in India Introduction of BankingDocument27 pagesProject Report "Banking System" in India Introduction of BankingShruti GargNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- 62329bos50452 cp8Document186 pages62329bos50452 cp8Pabitra Kumar PrustyNo ratings yet

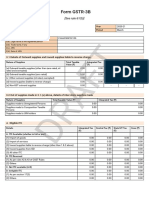

- Form GSTR-3B: (See Rule 61 (5) )Document2 pagesForm GSTR-3B: (See Rule 61 (5) )Pabitra Kumar PrustyNo ratings yet

- Maec Sem III Assignments 2020 21Document10 pagesMaec Sem III Assignments 2020 21Pabitra Kumar PrustyNo ratings yet

- Sant Gadge Baba Sant Gadge Baba Amravati U Amravati UniversityDocument7 pagesSant Gadge Baba Sant Gadge Baba Amravati U Amravati UniversityPabitra Kumar PrustyNo ratings yet

- IIPC & Final Mock Test Schedule May 2021Document4 pagesIIPC & Final Mock Test Schedule May 2021Pabitra Kumar PrustyNo ratings yet

- Indian Income Tax Return Acknowledgement: PAN NameDocument1 pageIndian Income Tax Return Acknowledgement: PAN NamePabitra Kumar PrustyNo ratings yet

- Assignments: Post Grduate Diploma in Management (PGDIM) Advance Diploma in Management (ADIM) Diploma in Management (DIM)Document6 pagesAssignments: Post Grduate Diploma in Management (PGDIM) Advance Diploma in Management (ADIM) Diploma in Management (DIM)Pabitra Kumar Prusty0% (1)

- Contract note cum tax invoiceDocument4 pagesContract note cum tax invoicePabitra Kumar PrustyNo ratings yet

- Supt (Finance) 2801Document4 pagesSupt (Finance) 2801Pabitra Kumar PrustyNo ratings yet

- Senior Faculty (Engine) Dated 28.01.2021Document4 pagesSenior Faculty (Engine) Dated 28.01.2021Pabitra Kumar PrustyNo ratings yet

- ISCA Quick RevisionDocument22 pagesISCA Quick RevisionzaaackNo ratings yet

- District Court CuttackDocument6 pagesDistrict Court CuttackAma AganaNo ratings yet

- E-Ticket For Gwalior Fort: Important InformationDocument2 pagesE-Ticket For Gwalior Fort: Important InformationPabitra Kumar PrustyNo ratings yet

- Duplicate: Alice Blue Financial Services PVT LTDDocument1 pageDuplicate: Alice Blue Financial Services PVT LTDPabitra Kumar PrustyNo ratings yet

- Formation and Functions of ShgsDocument29 pagesFormation and Functions of ShgsJyothiNo ratings yet

- Draf T: Form GSTR-3BDocument3 pagesDraf T: Form GSTR-3BPabitra Kumar PrustyNo ratings yet

- Wmcustomer 17188897 HU7 CustomerInvoiceDocument1 pageWmcustomer 17188897 HU7 CustomerInvoicePabitra Kumar PrustyNo ratings yet

- T Bact OintmentDocument8 pagesT Bact OintmentAditya RajNo ratings yet

- Personal Loan Application FormDocument29 pagesPersonal Loan Application FormPabitra Kumar PrustyNo ratings yet

- Trading JournalDocument17 pagesTrading JournalPabitra Kumar PrustyNo ratings yet

- C 09 S 4Document12 pagesC 09 S 4Ruwina Ayman100% (2)

- CPT Date Postpone - Notice Punjab Haryana High Court Clerk PostsDocument1 pageCPT Date Postpone - Notice Punjab Haryana High Court Clerk PostsPabitra Kumar PrustyNo ratings yet

- S No Name of Examination Date of Advt. Closing Date Date of ExamDocument2 pagesS No Name of Examination Date of Advt. Closing Date Date of ExamKavya SivakumarNo ratings yet

- Free 10: Open Demat Account in 5 Minutes Pay Just / TradeDocument1 pageFree 10: Open Demat Account in 5 Minutes Pay Just / TradePabitra Kumar PrustyNo ratings yet

- Plastic Recycling Business PlanDocument4 pagesPlastic Recycling Business PlanPabitra Kumar Prusty100% (1)

- What Should A Business Plan CoverDocument3 pagesWhat Should A Business Plan CoverAnkit PandeyNo ratings yet

- 23mar2020154856 - 20200323154842detailedadvt Contractposts Mar2020 Final 20.03Document6 pages23mar2020154856 - 20200323154842detailedadvt Contractposts Mar2020 Final 20.03Abhishek JainNo ratings yet

- Msme Application FormDocument7 pagesMsme Application FormPabitra Kumar PrustyNo ratings yet

- SL No Particulars Quantity Rate AmountDocument1 pageSL No Particulars Quantity Rate AmountPabitra Kumar PrustyNo ratings yet

- AmBank Card Application Form 2021Document15 pagesAmBank Card Application Form 2021Ore MacheNo ratings yet

- Sample Payoff Request LetterDocument1 pageSample Payoff Request Letterklg_consultant868860% (5)

- Working Capital Consortium FinancingDocument10 pagesWorking Capital Consortium FinancingShahzad SaifNo ratings yet

- ACC 102 - Accounts ReceivableDocument3 pagesACC 102 - Accounts Receivablewerter werterNo ratings yet

- BCO126 Mathematics of Finance: 3 Ects Spring Semester 2022Document38 pagesBCO126 Mathematics of Finance: 3 Ects Spring Semester 2022summerNo ratings yet

- DW Data 2014 q4Document15 pagesDW Data 2014 q4helpdotunNo ratings yet

- The Effect of COVID-19 on Banking Sector PerformanceDocument7 pagesThe Effect of COVID-19 on Banking Sector PerformanceMuhamad syahiir syauqii Mohamad yunus80% (5)

- Credit Risk Models Iv: Understanding and Pricing Cdos: Abel ElizaldeDocument52 pagesCredit Risk Models Iv: Understanding and Pricing Cdos: Abel ElizaldeDavid PrietoNo ratings yet

- Banks' Risk Management: A Comparison Study of UAE National and Foreign BanksDocument16 pagesBanks' Risk Management: A Comparison Study of UAE National and Foreign Bankssajid bhattiNo ratings yet

- HKICPA QP Exam (Module A) May2007 AnswerDocument13 pagesHKICPA QP Exam (Module A) May2007 Answercynthia tsuiNo ratings yet

- Banking Kpi Encyclopedia Preview PDFDocument5 pagesBanking Kpi Encyclopedia Preview PDFAbcd100% (2)

- Reviewing the 1991 Local Government Code to Improve Lives Through Fiscal ReformsDocument34 pagesReviewing the 1991 Local Government Code to Improve Lives Through Fiscal ReformsKevin RiveraNo ratings yet

- Credit Policy of J&K BankDocument64 pagesCredit Policy of J&K BankBilal Ah Parray100% (3)

- Pepa Project FinalDocument25 pagesPepa Project FinalSoundharya SomarajuNo ratings yet

- BNPL As A New Financial Instrument & Its Impact On Consumer's Buying BehaviourDocument16 pagesBNPL As A New Financial Instrument & Its Impact On Consumer's Buying BehaviourAshish kujurNo ratings yet

- Spouses Eduardo and Lydia Silos Vs PNBDocument1 pageSpouses Eduardo and Lydia Silos Vs PNBgregbaccayNo ratings yet

- Student Credit Card FAQDocument7 pagesStudent Credit Card FAQMoin KaserNo ratings yet

- O2 Refresh Key Info PDFDocument1 pageO2 Refresh Key Info PDFIbrahim El AminNo ratings yet

- Prozone by StockupdatesDocument181 pagesProzone by Stockupdatesstockupdates2012No ratings yet

- Unit 12 - BankingDocument92 pagesUnit 12 - BankingNhung Cẩm NguyễnNo ratings yet

- International Harvester Macleod Inc. V.Document6 pagesInternational Harvester Macleod Inc. V.Elmer Dela CruzNo ratings yet

- Fomc Statements - Side-By-sideDocument2 pagesFomc Statements - Side-By-sideurbanovNo ratings yet

- SWOT Analysis of BangladeshDocument31 pagesSWOT Analysis of BangladeshRifa TasfiaNo ratings yet

- Final Exam ReviewDocument6 pagesFinal Exam ReviewYolandaNo ratings yet

- Money and Banking Project - Soneri BankDocument29 pagesMoney and Banking Project - Soneri Banklushcheese100% (8)

- Researching Financing OptionsDocument2 pagesResearching Financing OptionsAbdulRehman100% (1)

- Chapter 7 Jan.22Document56 pagesChapter 7 Jan.22AaaNo ratings yet

- Identifying Text Structure #1Document3 pagesIdentifying Text Structure #1Ethiopia FurnNo ratings yet

- The Power of CreditDocument32 pagesThe Power of CreditSanjay RagupathyNo ratings yet

- U.S. Department of Education Student Loan Litigation ManualDocument69 pagesU.S. Department of Education Student Loan Litigation ManualmovingtocanadaNo ratings yet