You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Test Bank For Advanced Financial Accounting 10th Edition by Christensen PDFDocument71 pagesTest Bank For Advanced Financial Accounting 10th Edition by Christensen PDFa1086940450% (2)

- L 1Document5 pagesL 1Elizabeth Espinosa ManilagNo ratings yet

- Chapter 26 - Fundamentals of Corporate Finance 9th Edition - Test BankDocument23 pagesChapter 26 - Fundamentals of Corporate Finance 9th Edition - Test BankKellyGibbons100% (3)

- Products: Product List Updated As On 5-Sep-20Document8 pagesProducts: Product List Updated As On 5-Sep-20Kunal KashyapNo ratings yet

- Poem PoemDocument5 pagesPoem PoemElizabeth Espinosa ManilagNo ratings yet

- Cash To Accrual Accounting PDFDocument8 pagesCash To Accrual Accounting PDFElizabeth Espinosa ManilagNo ratings yet

- Robo-Advisors or Robo-Advisers Are A Class of Financial Adviser That ProvideDocument4 pagesRobo-Advisors or Robo-Advisers Are A Class of Financial Adviser That ProvideElizabeth Espinosa ManilagNo ratings yet

- G. Major Assumptions and Summary of Findings and Conclusions 1. Market FeasibilityDocument3 pagesG. Major Assumptions and Summary of Findings and Conclusions 1. Market FeasibilityElizabeth Espinosa Manilag100% (1)

- Finquiz Formula Sheet Cfa Level Iii 2019Document4 pagesFinquiz Formula Sheet Cfa Level Iii 2019Elizabeth Espinosa ManilagNo ratings yet

- Salomon Vs SalomonDocument7 pagesSalomon Vs SalomonRochakNo ratings yet

- Corporate Law Object ClauseDocument34 pagesCorporate Law Object ClausedaariyakNo ratings yet

- GPR 304 - LBA I Course Outline 2023Document18 pagesGPR 304 - LBA I Course Outline 2023Kimberly OdumbeNo ratings yet

- Basel IV & CRR II: Revised Standardised Approach For Market RiskDocument52 pagesBasel IV & CRR II: Revised Standardised Approach For Market RiskNasim AkhtarNo ratings yet

- Cost of CapitalDocument4 pagesCost of Capitalkomal mishraNo ratings yet

- Companies Act 2016 - TechnicalDocument13 pagesCompanies Act 2016 - TechnicalbukugendangNo ratings yet

- FactorsDocument4 pagesFactorsMerazul Islam MerazNo ratings yet

- Real Estate Mortgage Investment Conduits (Remics) Reporting InformationDocument63 pagesReal Estate Mortgage Investment Conduits (Remics) Reporting Informationhg202No ratings yet

- Prime White Cement Corp. v. IAC, 220 SCRA 103 (1993)Document11 pagesPrime White Cement Corp. v. IAC, 220 SCRA 103 (1993)bentley CobyNo ratings yet

- Advance Acct CH 3NDocument18 pagesAdvance Acct CH 3NtemedebereNo ratings yet

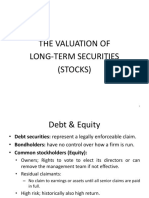

- Lecture - 4: The Valuation of Long-Term Securities (Stocks)Document54 pagesLecture - 4: The Valuation of Long-Term Securities (Stocks)Muhammad AfzalNo ratings yet

- Overdraft LimitDocument8 pagesOverdraft LimitMy EMailNo ratings yet

- Far Eastern University - Makati: Discussion ProblemsDocument2 pagesFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNo ratings yet

- Week Ten - Comparative International Auditing and Corporate GovernanceDocument31 pagesWeek Ten - Comparative International Auditing and Corporate GovernanceCoffee JellyNo ratings yet

- New Syllabus: NOTE: 1Document32 pagesNew Syllabus: NOTE: 1suresh1No ratings yet

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Ys (Kkadu Ekud: (Accounting Standards)Document175 pagesYs (Kkadu Ekud: (Accounting Standards)Aalam KhanNo ratings yet

- Welcome To My: PresentationDocument8 pagesWelcome To My: PresentationImran KhanNo ratings yet

- Share CapitalDocument17 pagesShare Capitalzydeco.14No ratings yet

- FDRM Unit I Session 2,3 & 4Document18 pagesFDRM Unit I Session 2,3 & 4N ArunsankarNo ratings yet

- Merger and Acquisition Transactions Under Ohada Law: 1. Why Do Companies Enter Into M&A Transactions in Africa?Document6 pagesMerger and Acquisition Transactions Under Ohada Law: 1. Why Do Companies Enter Into M&A Transactions in Africa?Che DivineNo ratings yet

- Civil Law Bar Exam Answers - PartnershipDocument8 pagesCivil Law Bar Exam Answers - PartnershipclarkNo ratings yet

- PSX Rule BookDocument212 pagesPSX Rule BookMuneer Dhamani100% (1)

- Depository & Non-Depository Financial Institutions of BangladeshDocument7 pagesDepository & Non-Depository Financial Institutions of BangladeshProbortok Somaj50% (2)

- Reviewer Corpo ExamDocument9 pagesReviewer Corpo ExamDel Rosario MarianNo ratings yet

- WIIMDocument95 pagesWIIMvesperNo ratings yet

- M & A - ICAI ChecklistDocument3 pagesM & A - ICAI Checklistgnsr_1984No ratings yet