You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- R12 Enhancements CheatSheetDocument5 pagesR12 Enhancements CheatSheetssunils7No ratings yet

- AUE2601+MO+001 2017 4 eDocument207 pagesAUE2601+MO+001 2017 4 eBrilliantNo ratings yet

- Special Journals Lecture No. 6Document25 pagesSpecial Journals Lecture No. 6Yuu100% (1)

- Intercompany Invoice: Bill To Billing InfoDocument3 pagesIntercompany Invoice: Bill To Billing InfoAlankar GuptaNo ratings yet

- Noncurrent Asset Held For Sale Problem 8-1Document11 pagesNoncurrent Asset Held For Sale Problem 8-1Clarisse Pelayo50% (2)

- Module I. Prior Period ErrorsDocument4 pagesModule I. Prior Period ErrorsMelanie SamsonaNo ratings yet

- ACC107 P1 EXAM With Key AnswerDocument9 pagesACC107 P1 EXAM With Key AnswerRyan Malanum AbrioNo ratings yet

- FABM1 Q4 Module 10Document20 pagesFABM1 Q4 Module 10Earl Christian BonaobraNo ratings yet

- The Administrative FunctionsDocument84 pagesThe Administrative FunctionsErly Mae100% (9)

- Presentation 2 - Audit of Intangible AssetsDocument27 pagesPresentation 2 - Audit of Intangible AssetsPaula De RuedaNo ratings yet

- Hydrocarbon Sector Skill Council: Education Qualification & Experience RequirementDocument10 pagesHydrocarbon Sector Skill Council: Education Qualification & Experience RequirementRedmi OfficeNo ratings yet

- Self Test Questions: Penyajian Laporan Keuangan (Psak 1)Document3 pagesSelf Test Questions: Penyajian Laporan Keuangan (Psak 1)AnnonymoesNo ratings yet

- Financial Analysis - Maruti Udyog LimitedDocument100 pagesFinancial Analysis - Maruti Udyog LimitedNithish JainNo ratings yet

- Kimmel Excersice 9Document11 pagesKimmel Excersice 9Jay LazaroNo ratings yet

- Sage x3 Solution Capabilities Guide 2021Document73 pagesSage x3 Solution Capabilities Guide 2021PDF ImporterNo ratings yet

- DP 28434Document235 pagesDP 28434Ankitha KavyaNo ratings yet

- Example:: To Record Depreciation From - ToDocument21 pagesExample:: To Record Depreciation From - Todebate ddNo ratings yet

- ACCO 208 - Business TaxationDocument14 pagesACCO 208 - Business TaxationEvelyn LabhananNo ratings yet

- This Study Resource Was: Problem 1-PatentDocument6 pagesThis Study Resource Was: Problem 1-PatentJan JanNo ratings yet

- New General Ledger Accounting 2: PDF Download From SAP Help Portal: Created On February 20, 2014Document4 pagesNew General Ledger Accounting 2: PDF Download From SAP Help Portal: Created On February 20, 2014mrobayorNo ratings yet

- Role of Public Financial Management in Risk Management For Developing Country GovernmentsDocument31 pagesRole of Public Financial Management in Risk Management For Developing Country GovernmentsFreeBalanceGRPNo ratings yet

- CH 03Document26 pagesCH 03Aries Gonzales CaraganNo ratings yet

- Listado 22Document1,047 pagesListado 22HéctorValleNo ratings yet

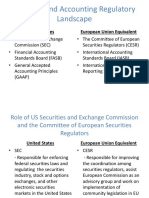

- Financial and Accounting Regulatory LandscapeDocument7 pagesFinancial and Accounting Regulatory LandscapeDiana Mindru StrenerNo ratings yet

- Accounts Receivable Control Account in The General Ledger of Montgomery CompanyDocument2 pagesAccounts Receivable Control Account in The General Ledger of Montgomery CompanyIshanNo ratings yet

- JAIIB AFM Practice MCQs Part 1Document17 pagesJAIIB AFM Practice MCQs Part 1preetmehtaNo ratings yet

- Erc Qualification Standards: Position SG Education Experience Training Eligibiliy Additional Requirements Accountant IIIDocument9 pagesErc Qualification Standards: Position SG Education Experience Training Eligibiliy Additional Requirements Accountant IIIArafat BauntoNo ratings yet

- Aarogyasri Health Care Trust 592023105847423Document19 pagesAarogyasri Health Care Trust 592023105847423Srikar PNo ratings yet

- Characteristics of The Accounting Information SystemDocument2 pagesCharacteristics of The Accounting Information SystemNoraini Abd RahmanNo ratings yet

- Icai ConceptsDocument36 pagesIcai ConceptsKarthik VadlamudiNo ratings yet