You might also like

- 04 04 FIG Questions AnswersDocument65 pages04 04 FIG Questions AnswersAbcdef100% (2)

- How To Install The Updated Pag-IBIG Egov ConverterDocument12 pagesHow To Install The Updated Pag-IBIG Egov Convertermarx marolina46% (13)

- Distance Learning Module Advanced Taxation CFM-300 PDFDocument128 pagesDistance Learning Module Advanced Taxation CFM-300 PDFKafonyi John100% (1)

- JE, GL, TB Magpantay RevisedDocument22 pagesJE, GL, TB Magpantay RevisedJasmine Acta100% (1)

- Accounting Test Bank - Bank ReconciliationDocument2 pagesAccounting Test Bank - Bank ReconciliationAyesha RGNo ratings yet

- 5.1 Seatwork Quiz Receivable FinancingDocument2 pages5.1 Seatwork Quiz Receivable FinancingSean Aaron Segucio0% (1)

- Lorico Inventories Sim AnswersDocument11 pagesLorico Inventories Sim Answersmaica G.No ratings yet

- Pq-Cash and Cash EquivalentsDocument3 pagesPq-Cash and Cash EquivalentsJanella PatriziaNo ratings yet

- Ppe ProblemsDocument4 pagesPpe ProblemsChristine joyNo ratings yet

- Handouts 1 P1Document3 pagesHandouts 1 P1Cristopher IanNo ratings yet

- Loans and Receivables - Long TermDocument3 pagesLoans and Receivables - Long TermAleezaAngelaSanchezNarvadezNo ratings yet

- Quiz InvestmentsDocument2 pagesQuiz InvestmentsstillwinmsNo ratings yet

- Cash and Cash EquivalentDocument5 pagesCash and Cash EquivalentPau SantosNo ratings yet

- Janet Wooster Owns A Retail Store That Sells New andDocument2 pagesJanet Wooster Owns A Retail Store That Sells New andAmit PandeyNo ratings yet

- Quiz 1Document9 pagesQuiz 1Czarhiena SantiagoNo ratings yet

- 03 Cash and Cash Equivalents (Student)Document27 pages03 Cash and Cash Equivalents (Student)Christina Dulay50% (2)

- This Study Resource Was: (Stale Check)Document2 pagesThis Study Resource Was: (Stale Check)Lyca Mae CubangbangNo ratings yet

- Problem I.: Borrowing Cost - ExercisesDocument2 pagesProblem I.: Borrowing Cost - Exercisesjingyuu kim100% (1)

- SA1 Submissions: Standalone AssessmentDocument11 pagesSA1 Submissions: Standalone AssessmentYenNo ratings yet

- Far 6673Document4 pagesFar 6673Marinel Felipe0% (1)

- Far Review - Notes and Receivable AssessmentDocument6 pagesFar Review - Notes and Receivable AssessmentLuisa Janelle BoquirenNo ratings yet

- Chapter 1 Acctg 5Document11 pagesChapter 1 Acctg 5Angelica MayNo ratings yet

- Financial Accounting - ReceivablesDocument7 pagesFinancial Accounting - ReceivablesKim Cristian MaañoNo ratings yet

- Instruction. Encircle The Letter That Corresponds To Your Answer. Do Not Use Pencils. Avoid ErasuresDocument6 pagesInstruction. Encircle The Letter That Corresponds To Your Answer. Do Not Use Pencils. Avoid ErasuresstillwinmsNo ratings yet

- D7Document11 pagesD7neo14No ratings yet

- Cq1 Topics Far2901 To 2926 PDF FreeDocument9 pagesCq1 Topics Far2901 To 2926 PDF FreeKlomoNo ratings yet

- La Consolacion College-Manila: School of Business and AccountancyDocument20 pagesLa Consolacion College-Manila: School of Business and AccountancyKasey PastorNo ratings yet

- Aud ReconDocument8 pagesAud ReconShaine PacsonNo ratings yet

- Phinma - University of Iloilo Bam 006: Midterm Exam: Amount UncollectibleDocument4 pagesPhinma - University of Iloilo Bam 006: Midterm Exam: Amount Uncollectiblehoneyjoy salapantanNo ratings yet

- Proof of CashDocument2 pagesProof of Cashmjc24100% (2)

- Financial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyDocument8 pagesFinancial Accounting and Reporting University of Luzon Cash and Cash Equivalents College of AccountancyJamhel MarquezNo ratings yet

- Ppe 2Document7 pagesPpe 2Lara Lewis Achilles50% (2)

- FAR Cash and Cash EquivalentsDocument2 pagesFAR Cash and Cash EquivalentsXander AquinoNo ratings yet

- Equity YyyDocument33 pagesEquity YyyJude SantosNo ratings yet

- 1st Answer Keys PPT - Ia 2Document44 pages1st Answer Keys PPT - Ia 2mia uyNo ratings yet

- QUIZ 4.1 Investments PDFDocument4 pagesQUIZ 4.1 Investments PDFGirly CrisostomoNo ratings yet

- ACT1205 - Module 4 - Audit of Fixed AssetsDocument7 pagesACT1205 - Module 4 - Audit of Fixed AssetsIo AyaNo ratings yet

- Far Eastern University - Makati: Discussion ProblemsDocument2 pagesFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNo ratings yet

- This Study Resource Was: Problem 1Document2 pagesThis Study Resource Was: Problem 1Michelle J UrbodaNo ratings yet

- FAR Test BankDocument17 pagesFAR Test BankMa. Efrelyn A. BagayNo ratings yet

- Loans ReceivableDocument1 pageLoans ReceivableJanidelle Swiftie67% (3)

- Encantadia Practice SetDocument17 pagesEncantadia Practice SetIrahq Yarte Torrejos100% (2)

- Prob 3Document3 pagesProb 3jikee11No ratings yet

- Wasting AssetsDocument4 pagesWasting AssetsjomelNo ratings yet

- Impairment of Loans: Comparison of "Incurred Loss Approach" and "Expected Credit Loss Impairment Approach"Document33 pagesImpairment of Loans: Comparison of "Incurred Loss Approach" and "Expected Credit Loss Impairment Approach"Christine Joy Rapi MarsoNo ratings yet

- CHAPTER 8 Intermediate Acctng 1Document58 pagesCHAPTER 8 Intermediate Acctng 1Tessang OnongenNo ratings yet

- Conceptual Framework and Accounting Standards: Janesene N. Sol MWF 1:00-2:00 PMDocument4 pagesConceptual Framework and Accounting Standards: Janesene N. Sol MWF 1:00-2:00 PMJanesene SolNo ratings yet

- Answer Key Activity 40Document4 pagesAnswer Key Activity 40MAXINE CLAIRE CUTINGNo ratings yet

- Module 1 Notes and Loans Receivable PDFDocument43 pagesModule 1 Notes and Loans Receivable PDFALEXA GENMARY GULFAN0% (1)

- Problem 4Document6 pagesProblem 4jhobsNo ratings yet

- P1 & TOA Quizzer (UE) (Cash & Cash Equivalents) PDFDocument10 pagesP1 & TOA Quizzer (UE) (Cash & Cash Equivalents) PDFrandy0% (1)

- Acc 11 HandoutDocument5 pagesAcc 11 HandoutRenalyn MadeloNo ratings yet

- Audit of Cash and ReceivablesDocument3 pagesAudit of Cash and ReceivablesTheQUICKbrownFOX100% (2)

- B. Inventory EstimationDocument6 pagesB. Inventory EstimationAce TevesNo ratings yet

- Cash and Cash Equivalents QuizDocument2 pagesCash and Cash Equivalents QuizMarkJoven Bergantin100% (1)

- Problems CCEDocument10 pagesProblems CCERafael Renz DayaoNo ratings yet

- Drill - ReceivablesDocument7 pagesDrill - ReceivablesMark Domingo MendozaNo ratings yet

- Intermediate Accounting Exercise 2 FinalsDocument2 pagesIntermediate Accounting Exercise 2 FinalsJune Maylyn MarzoNo ratings yet

- P1 Day4 RMDocument15 pagesP1 Day4 RMSharmaine Sur100% (1)

- Cash-And-Cash-Equivalent - Answers On HandoutDocument6 pagesCash-And-Cash-Equivalent - Answers On HandoutElaine AntonioNo ratings yet

- Accounts Receivable: Notwithstanding, Are Classified As Current AssetsDocument13 pagesAccounts Receivable: Notwithstanding, Are Classified As Current AssetsAdyangNo ratings yet

- ACCTG-206B-FIRST-PREBOARD Without AnswerDocument16 pagesACCTG-206B-FIRST-PREBOARD Without AnswerRheu ReyesNo ratings yet

- FAR-Midterm ExamDocument19 pagesFAR-Midterm ExamTxos Vaj100% (1)

- Peer Mentoring PretestxxDocument7 pagesPeer Mentoring PretestxxronnelNo ratings yet

- Criminal Tax Cases: Within Their Territorial and Original JurisdictionDocument1 pageCriminal Tax Cases: Within Their Territorial and Original Jurisdictionmarx marolinaNo ratings yet

- Chi-Squared: Test For Goodness of FitDocument14 pagesChi-Squared: Test For Goodness of Fitmarx marolinaNo ratings yet

- Finals Answer KeyDocument13 pagesFinals Answer Keymarx marolinaNo ratings yet

- Member Transfer FormDocument1 pageMember Transfer Formmarx marolinaNo ratings yet

- Finals Answer KeyDocument6 pagesFinals Answer Keymarx marolinaNo ratings yet

- Quiz On Apr30Document3 pagesQuiz On Apr30marx marolinaNo ratings yet

- Actg 321 Gill Syllabus Fall 2013Document11 pagesActg 321 Gill Syllabus Fall 2013marx marolinaNo ratings yet

- Within 100% 30% 30% 160% 50%: ShiftDocument2 pagesWithin 100% 30% 30% 160% 50%: Shiftmarx marolinaNo ratings yet

- SMALL AND MEDIUM EntitiesDocument19 pagesSMALL AND MEDIUM Entitiesmarx marolinaNo ratings yet

- Fallacies Of: AmbiguityDocument16 pagesFallacies Of: Ambiguitymarx marolinaNo ratings yet

- Supreme CourtDocument8 pagesSupreme Courtmarx marolinaNo ratings yet

- Crim Pro NotesDocument55 pagesCrim Pro Notesmarx marolina100% (1)

- ButlerDocument9 pagesButler2013studyNo ratings yet

- Fin2bsat Quiz1 InvProperty Fund PpeDocument5 pagesFin2bsat Quiz1 InvProperty Fund PpeMarvin San JuanNo ratings yet

- MST Practice QuestionsDocument11 pagesMST Practice QuestionsLaw GuruNo ratings yet

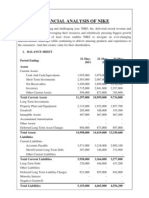

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- Impartial Fulfillment in Principles of AccountingDocument177 pagesImpartial Fulfillment in Principles of AccountingIlarde, Charles Ezra S.No ratings yet

- Cox and Kings Annual Report 2018Document228 pagesCox and Kings Annual Report 2018RAKESHKUMAR JAINNo ratings yet

- FABM2 Week 12 13 AsynchDocument8 pagesFABM2 Week 12 13 AsynchKhaira PeraltaNo ratings yet

- MarketingDocument13 pagesMarketingAnkit JenaNo ratings yet

- The Rule of Ethiopian Tax-ProfessionalDocument36 pagesThe Rule of Ethiopian Tax-ProfessionalMinaw BelayNo ratings yet

- Intermediate Accounting 15Th Edition Kieso Solutions Manual Full Chapter PDFDocument36 pagesIntermediate Accounting 15Th Edition Kieso Solutions Manual Full Chapter PDFjoyce.limon427100% (14)

- Agrani Bank at ADocument13 pagesAgrani Bank at AOhidNo ratings yet

- Manufacturing Accounts NotesDocument9 pagesManufacturing Accounts NotesFegason FegyNo ratings yet

- Excercise Sheet Lectures 1 and 2 Spring 2022Document16 pagesExcercise Sheet Lectures 1 and 2 Spring 2022Mohamed ZaitoonNo ratings yet

- 02 Accounting Process (Student)Document31 pages02 Accounting Process (Student)Christina DulayNo ratings yet

- Lesson 1 SFPDocument14 pagesLesson 1 SFPLydia Rivera100% (3)

- Movie ApplicationDocument12 pagesMovie ApplicationLas Vegas Review-JournalNo ratings yet

- 2003 BMGF 990pf Part 2Document296 pages2003 BMGF 990pf Part 2shikha.mindfulNo ratings yet

- 34 Accounting For Income Tax Intermediate Accounting 2 - CompressDocument4 pages34 Accounting For Income Tax Intermediate Accounting 2 - CompressKIMBERLY BEZARNo ratings yet

- Financial Accounting 8Th Edition Libby Solutions Manual Full Chapter PDFDocument36 pagesFinancial Accounting 8Th Edition Libby Solutions Manual Full Chapter PDFphyllis.horan125100% (11)

- Maujan - PK: Nothing Ventured Nothing GainedDocument35 pagesMaujan - PK: Nothing Ventured Nothing GainedZulqarnain Aamir JamalNo ratings yet

- Phillips Carbon Black (PHICAR) : Growth Momentum To Sustain..Document9 pagesPhillips Carbon Black (PHICAR) : Growth Momentum To Sustain..hashximNo ratings yet

- List of Banks in EthiopiaDocument20 pagesList of Banks in EthiopiaTewodros2014No ratings yet

- 04 Laboratory Worksheet 1 PDFDocument3 pages04 Laboratory Worksheet 1 PDFCristal Emerald BlazoNo ratings yet

- Laws of Guyana 28.01Document150 pagesLaws of Guyana 28.01Marlon98T423No ratings yet

- Accounting MCQsDocument12 pagesAccounting MCQsLaraib AliNo ratings yet

- Assignment of Management of Working Capital: Topic: Cash BudgetDocument10 pagesAssignment of Management of Working Capital: Topic: Cash BudgetDavinder Singh BanssNo ratings yet

- CHAPTER 3 Fundamental of ACC IDocument19 pagesCHAPTER 3 Fundamental of ACC IME100% (1)