You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Mika, Geoffrey-Kaizen Event Implementation Manual-Society of Manufacturing Engineers (SME) (2006) PDFDocument236 pagesMika, Geoffrey-Kaizen Event Implementation Manual-Society of Manufacturing Engineers (SME) (2006) PDFAlexandra Ps100% (3)

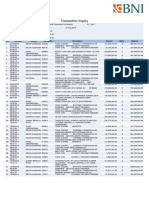

- SMP - Rek Koran Bni Agust 2018Document2 pagesSMP - Rek Koran Bni Agust 2018aruan paulusNo ratings yet

- Allen SollyDocument38 pagesAllen SollyVarun KannanNo ratings yet

- Prof.. Anju Dusseja: Name Roll - NoDocument18 pagesProf.. Anju Dusseja: Name Roll - NoOmkar PandeyNo ratings yet

- Fedex Vs DHL: Darshit Parikh Dhrumil Patel Henil Dudhia Maulik Amin Yasir ShethDocument27 pagesFedex Vs DHL: Darshit Parikh Dhrumil Patel Henil Dudhia Maulik Amin Yasir Shethhemal patelNo ratings yet

- Owl Creek Q2 2010 LetterDocument9 pagesOwl Creek Q2 2010 Letterjackefeller100% (1)

- 1.6 Safety CultureDocument59 pages1.6 Safety CultureAinur Sya Irah100% (4)

- Executive Summary: Recruitment & Selection Trends in ITES-BPO Sector in NCRDocument61 pagesExecutive Summary: Recruitment & Selection Trends in ITES-BPO Sector in NCRleonNo ratings yet

- Take The Money - or RunDocument10 pagesTake The Money - or RunsdfNo ratings yet

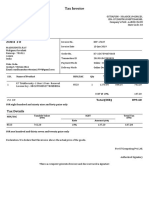

- Sold To: Tax InvoiceDocument1 pageSold To: Tax Invoiceমধু্স্মিতা ৰায়No ratings yet

- Steel Corporation Vs SCP Employees UnionDocument3 pagesSteel Corporation Vs SCP Employees UnionDustin NitroNo ratings yet

- Ch01 5th Ed Narayanaswamy Financial AccountingDocument20 pagesCh01 5th Ed Narayanaswamy Financial AccountingDeepti Agarwal100% (1)

- Sub: Handing Over of Customs Cleared DocumentsDocument11 pagesSub: Handing Over of Customs Cleared DocumentsSrikanth VankamamidiNo ratings yet

- U4A1 AssignmentDocument1 pageU4A1 AssignmentDrippy SnowflakeNo ratings yet

- MS AcessDocument14 pagesMS AcessMridul VashisthNo ratings yet

- Resume Sample Using Novo AppDocument1 pageResume Sample Using Novo AppFrancis GananciasNo ratings yet

- APPSC Group 1 & 2 POSTS @APPSCDocument4 pagesAPPSC Group 1 & 2 POSTS @APPSCOmega RangerNo ratings yet

- Tugas Sesi 7Document5 pagesTugas Sesi 7mutmainnahNo ratings yet

- Online TradingDocument64 pagesOnline Tradingferoz5105No ratings yet

- Housing For All 2022Document100 pagesHousing For All 2022Pranav TripathiNo ratings yet

- April Time TableDocument15 pagesApril Time TableManfred GithinjiNo ratings yet

- Sample TestDocument15 pagesSample TestSoofeng LokNo ratings yet

- Inquiry Letter Writing Tips: Outline and Organise Your InquiryDocument4 pagesInquiry Letter Writing Tips: Outline and Organise Your InquirySaksham GuptaNo ratings yet

- Holiday Inn Media KitDocument25 pagesHoliday Inn Media Kitapi-341539127No ratings yet

- EFFECTIVENESS of Rural Marketing Strategy in FMCG Products at Coimbatore DistrictDocument5 pagesEFFECTIVENESS of Rural Marketing Strategy in FMCG Products at Coimbatore DistrictHebziba BeulaNo ratings yet

- 14.second Brand StrategyDocument3 pages14.second Brand StrategySnigdha Kumar100% (1)

- PCSODocument1 pagePCSOLee YouNo ratings yet

- MBA - SEM 1 NotesDocument99 pagesMBA - SEM 1 NotesumeshNo ratings yet

- Chemical Amplification Resists - History and Development at IBM - IBM JRD 1997, by H ItoDocument12 pagesChemical Amplification Resists - History and Development at IBM - IBM JRD 1997, by H ItofrechalpyNo ratings yet

- Using Predictive Analytics To Optimize Asset Maintenance in The Utilities IndustryDocument6 pagesUsing Predictive Analytics To Optimize Asset Maintenance in The Utilities IndustryCognizant100% (1)