0% found this document useful (0 votes)

983 views26 pagesStat 476 Life Contingencies II

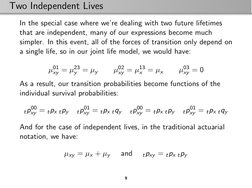

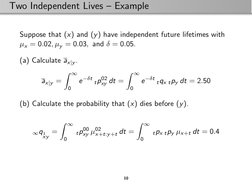

This document discusses models for multiple life insurance products. It introduces joint life models that allow for transitions between states based on the statuses of two insured lives. It also discusses multiple decrement models that allow for individuals leaving a population due to different causes. Expressions are provided for probabilities and expected present values involving multiple lives or decrements. An example calculates values for a term life policy on two independent lives.

Uploaded by

Ranjana DasCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

983 views26 pagesStat 476 Life Contingencies II

This document discusses models for multiple life insurance products. It introduces joint life models that allow for transitions between states based on the statuses of two insured lives. It also discusses multiple decrement models that allow for individuals leaving a population due to different causes. Expressions are provided for probabilities and expected present values involving multiple lives or decrements. An example calculates values for a term life policy on two independent lives.

Uploaded by

Ranjana DasCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

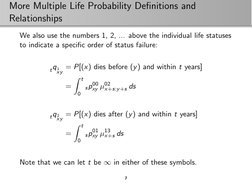

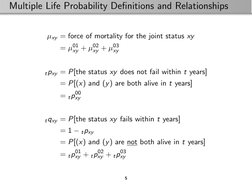

![Multiple Life Probability Definitions and Relationships

tpxy = P[the status xy does not fail within t years]

= P[(x) or (y) or](https://screenshots.scribd.com/Scribd/252_100_85/188/461079735/6.jpeg)