You might also like

- Master Budget Case: Toyworks Ltd. (A)Document4 pagesMaster Budget Case: Toyworks Ltd. (A)RIKUDO SENNIN100% (1)

- Unithibs LTDDocument4 pagesUnithibs LTDRobert Daniel AquinoNo ratings yet

- Master Budget Case: Turabi LTDDocument4 pagesMaster Budget Case: Turabi LTDFarwa SamreenNo ratings yet

- Budget Assignment VaDocument4 pagesBudget Assignment Vamiss independent0% (1)

- Building Your Skills22Document2 pagesBuilding Your Skills22chisomaga njokuNo ratings yet

- Requirements. All Raw Materials Are Purchased On Account. 50% of A Quarter'sDocument4 pagesRequirements. All Raw Materials Are Purchased On Account. 50% of A Quarter'sairis nyanganoNo ratings yet

- Tesla Toy Company Budget Project InstructionsDocument4 pagesTesla Toy Company Budget Project InstructionsRisvana RizzNo ratings yet

- BudgetingDocument9 pagesBudgetingshobi_300033% (3)

- Management AccountingDocument5 pagesManagement AccountingHamdan SheikhNo ratings yet

- Case Study #1Document3 pagesCase Study #1mackkshellNo ratings yet

- Pro Forma Financials for Soul Mate Textile (38Document11 pagesPro Forma Financials for Soul Mate Textile (38Nadia NathaniaNo ratings yet

- C 10chap10Document103 pagesC 10chap10Aya ObandoNo ratings yet

- Management Accounting SundayDocument5 pagesManagement Accounting SundayAhsan MaqboolNo ratings yet

- Cash Management: Why Organisations Hold CashDocument15 pagesCash Management: Why Organisations Hold CashAjay Kumar TakiarNo ratings yet

- 1 - MB Group Assignment I 21727Document2 pages1 - MB Group Assignment I 21727RoNo ratings yet

- TACC507GroupAssignmentReportandPresentation 82339240Document6 pagesTACC507GroupAssignmentReportandPresentation 82339240Zain NaeemNo ratings yet

- Modul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662Document30 pagesModul Akuntansi Manajemen II 2019-2020-Converted-Converted - 209630662hendy DidoNo ratings yet

- FINC 301 Tutorial Set 5Document3 pagesFINC 301 Tutorial Set 5Anita SmithNo ratings yet

- CH 23 Exercises ProblemsDocument4 pagesCH 23 Exercises ProblemsAhmed El KhateebNo ratings yet

- Chapter 4Document12 pagesChapter 4jeo beduaNo ratings yet

- Solutions in AppendixDocument13 pagesSolutions in Appendixtfytf70% (2)

- Required: Using These Data, Construct The December 31, Year 5 Balance Sheet For Your AnalysisDocument3 pagesRequired: Using These Data, Construct The December 31, Year 5 Balance Sheet For Your AnalysisJARED DARREN ONGNo ratings yet

- The Grady Tire Company Manufactures Racing Tires For Bicycles GradyDocument2 pagesThe Grady Tire Company Manufactures Racing Tires For Bicycles GradyAmit PandeyNo ratings yet

- Profit Planning Viettien CorpDocument7 pagesProfit Planning Viettien CorpThành ChiếnNo ratings yet

- Lecture-7 Overhead (Part 1)Document22 pagesLecture-7 Overhead (Part 1)Nazmul-Hassan Sumon100% (2)

- Chapter 5-Master Budgeting Offline Quiz-1 PDFDocument2 pagesChapter 5-Master Budgeting Offline Quiz-1 PDFMARY ALODIA BEN YBARZABALNo ratings yet

- Ae 191 F-Test 1Document3 pagesAe 191 F-Test 1Venus PalmencoNo ratings yet

- Completing A Master BudgetDocument2 pagesCompleting A Master BudgetPines MacapagalNo ratings yet

- IPE 481 - Term Final Question - January 2020Document6 pagesIPE 481 - Term Final Question - January 2020Shaumik RahmanNo ratings yet

- CAT T-10 Mock TestDocument4 pagesCAT T-10 Mock TestPrashant PokharelNo ratings yet

- Solution and AnswerDocument4 pagesSolution and AnswerMicaela EncinasNo ratings yet

- Financial Management PORTFOLIO MidDocument8 pagesFinancial Management PORTFOLIO MidMyka Marie CruzNo ratings yet

- Financial Management PORTFOLIO MidDocument8 pagesFinancial Management PORTFOLIO MidMyka Marie CruzNo ratings yet

- Assignment Accounting For BusinessDocument5 pagesAssignment Accounting For BusinessValencia CarolNo ratings yet

- T2 Exercises QuestDocument3 pagesT2 Exercises QuestXin XiuNo ratings yet

- Drills - Comprehensive BudgetingDocument11 pagesDrills - Comprehensive BudgetingDan RyanNo ratings yet

- General Case Study - Student - BudgetingDocument6 pagesGeneral Case Study - Student - Budgetingmika.tov1997No ratings yet

- Referral Deferral Assessement 2 2020 21Document2 pagesReferral Deferral Assessement 2 2020 21KakaNo ratings yet

- Sample IA QuestionDocument3 pagesSample IA QuestionElisa Ferrer RamosNo ratings yet

- The Grilton Tire Company Manufactures Racing Tires For Bicycles GriltonDocument2 pagesThe Grilton Tire Company Manufactures Racing Tires For Bicycles GriltonAmit PandeyNo ratings yet

- Planning, Performance and EvaluationDocument26 pagesPlanning, Performance and EvaluationJoan LauNo ratings yet

- Accounting For Managers-Assignment MaterialsDocument4 pagesAccounting For Managers-Assignment MaterialsYehualashet TeklemariamNo ratings yet

- Prepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4UDocument31 pagesPrepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4USaiful IslamNo ratings yet

- IMAC Budgeting Project Semester 2 2021Document4 pagesIMAC Budgeting Project Semester 2 2021TashaNo ratings yet

- Cost II Chap3Document11 pagesCost II Chap3abelNo ratings yet

- 8.1 Manact Mid Class4 ch8 สอนเนื้อหา 2-2022Document4 pages8.1 Manact Mid Class4 ch8 สอนเนื้อหา 2-2022Chokthawee RattanawetwongNo ratings yet

- Cash Budget for Calgon Products for September 20x4Document11 pagesCash Budget for Calgon Products for September 20x4신두No ratings yet

- Budgeting CSECDocument4 pagesBudgeting CSECTyanna TaylorNo ratings yet

- FDNACCT Quiz-3 Set-A Answer-KeyDocument4 pagesFDNACCT Quiz-3 Set-A Answer-KeyPia DigaNo ratings yet

- Prac 1 Final PreboardDocument10 pagesPrac 1 Final Preboardbobo kaNo ratings yet

- IF2 - Project 1 PDFDocument6 pagesIF2 - Project 1 PDFBillNo ratings yet

- FDNACCT Quiz-3 Set-B Answer-KeyDocument4 pagesFDNACCT Quiz-3 Set-B Answer-KeyPia DigaNo ratings yet

- Case 2 - Dynamic TechnologyDocument3 pagesCase 2 - Dynamic TechnologysanjitypingNo ratings yet

- Unit 3 - Essay QuestionsDocument4 pagesUnit 3 - Essay QuestionsJaijuNo ratings yet

- FDNACCT Quiz-3 Set-C Answer-KeyDocument4 pagesFDNACCT Quiz-3 Set-C Answer-KeyPia DigaNo ratings yet

- AE24 Lesson 5Document9 pagesAE24 Lesson 5Majoy BantocNo ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Nondepository Credit Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Tenses TableDocument5 pagesTenses Tableapi-314670535No ratings yet

- Tenses TableDocument5 pagesTenses Tableapi-314670535No ratings yet

- Tenses TableDocument5 pagesTenses Tableapi-314670535No ratings yet

- Tenses TableDocument5 pagesTenses Tableapi-314670535No ratings yet

- 32 Ielts Essay Samples Band 9Document34 pages32 Ielts Essay Samples Band 9mh73% (26)

- Tenses TableDocument5 pagesTenses Tableapi-314670535No ratings yet

- Ielts Orientation British CouncilDocument33 pagesIelts Orientation British CouncilJoyCe Labang25% (4)

- 32 Ielts Essay Samples Band 9Document34 pages32 Ielts Essay Samples Band 9mh73% (26)

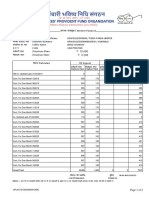

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- Management Skills For EntrepreneursDocument21 pagesManagement Skills For EntrepreneursDhruv ChaudharyNo ratings yet

- Barangay transparency monitoring form titleDocument1 pageBarangay transparency monitoring form titleOmar Dizon100% (1)

- Durado RRLDocument3 pagesDurado RRLJohneen DungqueNo ratings yet

- KALAMAZOO Case Study SolutionDocument13 pagesKALAMAZOO Case Study SolutionSanskriti sahuNo ratings yet

- Rajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Document1 pageRajasthan Technical University, Kota: Syllabus IV Year-VIII Semester: B. Tech. (Civil Engineering)Bhavy Kumar JainNo ratings yet

- Marketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Document2 pagesMarketing Plan Guidelines:: Bus314 Marketing Management (Ncy)Murgi kun :3No ratings yet

- GUCCI - Case Only110910Document39 pagesGUCCI - Case Only110910sabastien_10dec5663No ratings yet

- Communication Plan September 27Document24 pagesCommunication Plan September 27Rosemarie T. BrionesNo ratings yet

- Construction of Health Center ProjectDocument50 pagesConstruction of Health Center ProjectChinangNo ratings yet

- Anush IpDocument24 pagesAnush IpAnsh SharmaNo ratings yet

- Max AR Final 130812 PDFDocument731 pagesMax AR Final 130812 PDFsnjv2621No ratings yet

- C&I JSA 09 GeneralDocument1 pageC&I JSA 09 Generalamit kumarNo ratings yet

- IBS Selection Process GuideDocument24 pagesIBS Selection Process GuideApna time aayegaNo ratings yet

- Export Oriented UnitsDocument10 pagesExport Oriented UnitsMansi GuptaNo ratings yet

- Homeroom Guidance: Siyahan Nga Bahin - Modyul 2: An Akon GintikanganDocument10 pagesHomeroom Guidance: Siyahan Nga Bahin - Modyul 2: An Akon GintikangansaraiNo ratings yet

- The Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasDocument24 pagesThe Expenditure Cycle: Purchasing and Cash Disbursements: Magister Akuntansi PerbanasTitan HerdiantoNo ratings yet

- 1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFDocument380 pages1271 XII Accountancy Study Material Supplementary Material HOTS and VBQ 2014 15 PDFBalaji TkpNo ratings yet

- Implied JoinDocument4 pagesImplied JoinramyasidNo ratings yet

- Top 20 Customer Relationship Manager Interview QuestionsDocument8 pagesTop 20 Customer Relationship Manager Interview QuestionsYifredewNo ratings yet

- Forms For Permission Under OMR 1984Document5 pagesForms For Permission Under OMR 1984karpanaiNo ratings yet

- Abacus Securities V AmpilDocument4 pagesAbacus Securities V AmpilThameenah ArahNo ratings yet

- WillaWare v Jesichris ManufacturingDocument2 pagesWillaWare v Jesichris ManufacturingloschudentNo ratings yet

- Jurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNDocument8 pagesJurnal Penelitian Dosen Fikom (UNDA) Vol.10 No.2, November 2019, ISSNkiki rifkiNo ratings yet

- INTERVIEW GUIDE For BMADocument6 pagesINTERVIEW GUIDE For BMAJale Ann A. EspañolNo ratings yet

- Whatsapp Download Protect-1Document2 pagesWhatsapp Download Protect-1jaisoumya567No ratings yet

- Asialink Loan Application v7 FillableDocument2 pagesAsialink Loan Application v7 FillableJovelyn MarimonNo ratings yet

- Kajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in WorldDocument10 pagesKajaria Ceramics: Production and Consumption Trend of Ceramic Tiles in Worldapi-556903190No ratings yet

- Chapter 7 (Basic Elements of Planning and Decision Making)Document21 pagesChapter 7 (Basic Elements of Planning and Decision Making)babon.eshaNo ratings yet

- Certificado Reparación Carcasas Bombas y CompresoresDocument3 pagesCertificado Reparación Carcasas Bombas y CompresoresdanyNo ratings yet