You might also like

- Due Diligence-Tax Due Dil - FinalDocument6 pagesDue Diligence-Tax Due Dil - FinalEljoe VinluanNo ratings yet

- Tax Due DiligenceDocument2 pagesTax Due Diligencemiboca8966No ratings yet

- Corporate TaxDocument29 pagesCorporate Taxsu_pathriaNo ratings yet

- Preface: What Is The Tax Planning ?Document29 pagesPreface: What Is The Tax Planning ?su_pathriaNo ratings yet

- Accounts: Assets Owned by A Business or Liabilities Owed by A Business. It Is AlsoDocument9 pagesAccounts: Assets Owned by A Business or Liabilities Owed by A Business. It Is AlsoIfa PeelayNo ratings yet

- Interplay of Accounting and Taxation PrinciplesDocument20 pagesInterplay of Accounting and Taxation PrinciplesChelsea BorbonNo ratings yet

- Buckwold 21e - CH 1 & 2 Selected SolutionDocument15 pagesBuckwold 21e - CH 1 & 2 Selected SolutionLucyNo ratings yet

- Tax Avoidance and Tax EvasionDocument11 pagesTax Avoidance and Tax EvasionYashVardhan100% (1)

- Preface: What Is The Tax Planning ?Document29 pagesPreface: What Is The Tax Planning ?SpUnky RohitNo ratings yet

- CTP 22 QuestionsDocument31 pagesCTP 22 QuestionsNitin MalikNo ratings yet

- Effective Tax ManagementDocument19 pagesEffective Tax ManagementMary Kathe Rachel ReyesNo ratings yet

- Corporate Tax Instructions - FinalDocument15 pagesCorporate Tax Instructions - Finalapi-306226330No ratings yet

- Interview QuestionsDocument12 pagesInterview QuestionsnadeemNo ratings yet

- Accounting Fees 2023Document12 pagesAccounting Fees 2023processingNo ratings yet

- Business Taxation MeaningDocument4 pagesBusiness Taxation MeaningSheila Mae AramanNo ratings yet

- 8TH Sem Tax Paper PDFDocument25 pages8TH Sem Tax Paper PDFAnamika VatsaNo ratings yet

- Chapter 14Document40 pagesChapter 14Ivo_NichtNo ratings yet

- Tax Planning, Evasion, AvoidanceDocument16 pagesTax Planning, Evasion, AvoidanceDr. Nathan WafNo ratings yet

- Re Industrypack Income Tax 2010Document2 pagesRe Industrypack Income Tax 2010So LokNo ratings yet

- PWC Vietnam Pocket Tax Book 2013Document43 pagesPWC Vietnam Pocket Tax Book 2013Angie NguyenNo ratings yet

- Module 13 Regular Deductions 3Document16 pagesModule 13 Regular Deductions 3Donna Mae FernandezNo ratings yet

- Understanding Tax AccountingDocument2 pagesUnderstanding Tax AccountingJonhmark AniñonNo ratings yet

- Homework - Income TaxesDocument3 pagesHomework - Income TaxesPeachyNo ratings yet

- IFRS News: Beginners' Guide: Nine Steps To Income Tax AccountingDocument4 pagesIFRS News: Beginners' Guide: Nine Steps To Income Tax AccountingVincent Chow Soon KitNo ratings yet

- Fta 4 SildeDocument1 pageFta 4 Sildemostafa SaidNo ratings yet

- Student Name: Mac Guiver Castro Sánchez Student ID: VTI18197 BSBFIM601 Manage FinancesDocument25 pagesStudent Name: Mac Guiver Castro Sánchez Student ID: VTI18197 BSBFIM601 Manage FinancesPriyanka AggarwalNo ratings yet

- HC Deb 24 May 2006 Ccwa111-2 Irc V Willoughby & Another (1997)Document4 pagesHC Deb 24 May 2006 Ccwa111-2 Irc V Willoughby & Another (1997)qwerty asNo ratings yet

- M1PLR Introduction To Business TaxesDocument2 pagesM1PLR Introduction To Business TaxesClaricel JoyNo ratings yet

- Canadian Income Tax - Buckwold Kitunen - 14e SolutionsDocument104 pagesCanadian Income Tax - Buckwold Kitunen - 14e SolutionsMilica Kalinic40% (5)

- Income TaxDocument9 pagesIncome TaxAmit Vikram OjhaNo ratings yet

- AX Lanning: by Anup K SuchakDocument27 pagesAX Lanning: by Anup K SuchakanupsuchakNo ratings yet

- Article VAT Refunds and Cashflows Alexander Mapunda 17JUNE2019Document2 pagesArticle VAT Refunds and Cashflows Alexander Mapunda 17JUNE2019James MsuyaNo ratings yet

- Tax 2 On Tax LiabilitiesDocument2 pagesTax 2 On Tax LiabilitiesAlberto NicholsNo ratings yet

- Tax On Corporate Transactions in PhilippinesDocument21 pagesTax On Corporate Transactions in PhilippinesD GNo ratings yet

- SWIFT Notes To Financial StatementsDocument11 pagesSWIFT Notes To Financial StatementsArvin TejonesNo ratings yet

- SynopsisDocument7 pagesSynopsisJagruti KisnaniNo ratings yet

- English Final Assignment: Unit Six Tax Accounting DiscussionDocument5 pagesEnglish Final Assignment: Unit Six Tax Accounting DiscussionHendraSaepulBaktiNo ratings yet

- Accounting ConceptsDocument11 pagesAccounting ConceptssyedasadaligardeziNo ratings yet

- Ifp 29 Tax PlanningDocument5 pagesIfp 29 Tax Planningsachin_chawlaNo ratings yet

- Entrepreneur's World #2Document2 pagesEntrepreneur's World #2Lex ValoremNo ratings yet

- Transfer Pricing in The PhilippinesDocument8 pagesTransfer Pricing in The PhilippinesJayson Berja de LeonNo ratings yet

- Tax Management: Planning and ComplianceDocument12 pagesTax Management: Planning and ComplianceNidheesh TpNo ratings yet

- Setting Up The BusinessDocument2 pagesSetting Up The BusinessJohn Bohorquez JimenezNo ratings yet

- Chapter 16 Taxation 2018 PDFDocument63 pagesChapter 16 Taxation 2018 PDFNeo WilliamNo ratings yet

- TaxHelpForParishTreasurers OCADocument13 pagesTaxHelpForParishTreasurers OCAConnor McloudNo ratings yet

- Vat Audit by Chetan SarafDocument33 pagesVat Audit by Chetan Sarafchetan saraf100% (1)

- Aktin PresentDocument12 pagesAktin PresentErin SinagaNo ratings yet

- "Avoid Surprises On Deferred Income Taxes" by Lucy L. Chan and Armin F. Tulio (October 24, 2011)Document3 pages"Avoid Surprises On Deferred Income Taxes" by Lucy L. Chan and Armin F. Tulio (October 24, 2011)badette PaningbatanNo ratings yet

- Confirm Vat Audit ProjectDocument33 pagesConfirm Vat Audit ProjectkennyajayNo ratings yet

- Tax Classifications Outline Fall 2021Document3 pagesTax Classifications Outline Fall 2021MacKenzieNo ratings yet

- 2 Tax GropDocument3 pages2 Tax GropPeter MNo ratings yet

- Tax Rate and Double Taxation - PPTDocument15 pagesTax Rate and Double Taxation - PPTAlex CruzNo ratings yet

- SomethingDocument6 pagesSomethingGanya BishnoiNo ratings yet

- Sample Audit Procedute Tax PHDocument3 pagesSample Audit Procedute Tax PHborgyambuloNo ratings yet

- Deferred Tax and Business Combinations: IFRS 3/IAS 12Document15 pagesDeferred Tax and Business Combinations: IFRS 3/IAS 12direhitNo ratings yet

- Moses Kulaba - How To Curb Transfer Mispricing and Illicit Tax Evasion in The Extractive Sector 2020Document7 pagesMoses Kulaba - How To Curb Transfer Mispricing and Illicit Tax Evasion in The Extractive Sector 2020Moses KulabaNo ratings yet

- BSBFIM601 Manage Finances Task 1Document16 pagesBSBFIM601 Manage Finances Task 1Kathleen RamientoNo ratings yet

- Chapter 14Document37 pagesChapter 14Angel SweetNo ratings yet

- 1601-C Monthly Remittance Return: of Income Taxes Withheld On CompensationDocument1 page1601-C Monthly Remittance Return: of Income Taxes Withheld On CompensationEljoe Vinluan0% (1)

- 2020 0605 Return MspaduaDocument1 page2020 0605 Return MspaduaEljoe VinluanNo ratings yet

- Tax Return Receipt Confirmation: From: To: DateDocument1 pageTax Return Receipt Confirmation: From: To: DateEljoe VinluanNo ratings yet

- Due Diligence-Fin Due DilDocument7 pagesDue Diligence-Fin Due DilEljoe VinluanNo ratings yet

- Due Diligence-Asset Due DilDocument7 pagesDue Diligence-Asset Due DilEljoe VinluanNo ratings yet

- 49940annex A-Rmo26 - 2010Document3 pages49940annex A-Rmo26 - 2010Eljoe VinluanNo ratings yet

- STRATEGIC DUE DILIGENCE - HanaDocument7 pagesSTRATEGIC DUE DILIGENCE - HanaEljoe VinluanNo ratings yet

- Bharti Airtel LTD.: Your Account Summary This Month'S ChargesDocument5 pagesBharti Airtel LTD.: Your Account Summary This Month'S ChargesMadhukar Reddy KukunoorNo ratings yet

- Denodo Job RoleDocument2 pagesDenodo Job Role059 Monisha BaskarNo ratings yet

- Managerial Economics-CasesDocument3 pagesManagerial Economics-Casessherryl caoNo ratings yet

- Customer Information Sheet (CRL-FM-ADMN-049) - r1Document1 pageCustomer Information Sheet (CRL-FM-ADMN-049) - r1alvin salmingoNo ratings yet

- MCP3913 Rev. A Silicon Errata and Data Sheet ClarificationDocument4 pagesMCP3913 Rev. A Silicon Errata and Data Sheet ClarificationAldo HernandezNo ratings yet

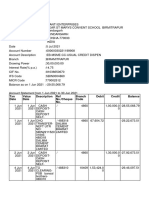

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument7 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaideep MishraNo ratings yet

- CASE No. 51 Lanuza vs. de Leon Lanuza vs. de Leon, 20 SCRA 369Document2 pagesCASE No. 51 Lanuza vs. de Leon Lanuza vs. de Leon, 20 SCRA 369Al Jay MejosNo ratings yet

- Chapter 1 - The First Big Question - Where Is The Organization NowDocument7 pagesChapter 1 - The First Big Question - Where Is The Organization NowSteffany Roque100% (1)

- G Ym 6 F 8 HEtoev 4 GEbDocument6 pagesG Ym 6 F 8 HEtoev 4 GEbPrakhar AgarwalNo ratings yet

- DownloadDocument1 pageDownloadRasika JadhavNo ratings yet

- An Analysis of Delta Air Lines - Based OnDocument5 pagesAn Analysis of Delta Air Lines - Based OnYan FengNo ratings yet

- Guidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFDocument200 pagesGuidelines On PD and LGD Estimation (EBA-GL-2017-16) - Chapters 1,2,3 (Only PD Estimation Part) PDFShankar RavichandranNo ratings yet

- Summary Of: The Value of Saving A Life: Evidence From The Labor MarketDocument2 pagesSummary Of: The Value of Saving A Life: Evidence From The Labor MarketFreed DragsNo ratings yet

- CHP 3 Insurer Ownership, Financial & - Operational StructureDocument24 pagesCHP 3 Insurer Ownership, Financial & - Operational StructureIskandar Zulkarnain Kamalluddin100% (1)

- Essay Plans 1: Across The Economy and Thus Stimulate Lending, Borrowing, AD and Economic GrowthDocument24 pagesEssay Plans 1: Across The Economy and Thus Stimulate Lending, Borrowing, AD and Economic GrowthAbhishek JainNo ratings yet

- SR - No. Security - Name Isin Scrip - ID Intraday Stock ListDocument10 pagesSR - No. Security - Name Isin Scrip - ID Intraday Stock ListSashang S VNo ratings yet

- Aeb4101 Engineering and Design: Module - 3Document14 pagesAeb4101 Engineering and Design: Module - 3saiNo ratings yet

- Consumer Perceptions About Different Brands of WatchesDocument32 pagesConsumer Perceptions About Different Brands of Watchesgoodluckrai100% (1)

- िदली िविवालय University of Delhi: Fee ReceiptDocument1 pageिदली िविवालय University of Delhi: Fee ReceiptramanNo ratings yet

- Atf-Ls-4.5 Subcontracting of Tests - Final 0 3Document2 pagesAtf-Ls-4.5 Subcontracting of Tests - Final 0 3Jeji HirboraNo ratings yet

- Fdocuments - in PNB Training ReportdocxDocument87 pagesFdocuments - in PNB Training ReportdocxAviral Pratap Singh KhareNo ratings yet

- Construction Safety & Health Management System: (Accident Prevention Program)Document8 pagesConstruction Safety & Health Management System: (Accident Prevention Program)carlito alvarezNo ratings yet

- 21 00202 Proposed Construction of Basketball Court Roofing at Bugallon PlazaDocument84 pages21 00202 Proposed Construction of Basketball Court Roofing at Bugallon PlazaJN CNo ratings yet

- Developing A Business Mindset: Business in Action 8e Bovée/ThillDocument33 pagesDeveloping A Business Mindset: Business in Action 8e Bovée/ThillTehreem AhmedNo ratings yet

- 2.2 - Decades of Research On Foreign Subsidiary Divestment, What Do We Really Know About Its AntecedentsDocument18 pages2.2 - Decades of Research On Foreign Subsidiary Divestment, What Do We Really Know About Its AntecedentsNabila HanaraniaNo ratings yet

- 2 - Dilemma in Hiring PDFDocument5 pages2 - Dilemma in Hiring PDFmanik singhNo ratings yet

- Thesis Statement Examples For Child LaborDocument7 pagesThesis Statement Examples For Child Laborafbtbegxe100% (2)

- Powerpoints and CopyrightDocument4 pagesPowerpoints and CopyrightqwbnswergrmnpjxpozNo ratings yet

- Wind Turbine Operation and Maintenance Literature ReviewDocument4 pagesWind Turbine Operation and Maintenance Literature Reviewwaleedishaque50% (2)

- Brand DecisionsDocument38 pagesBrand Decisionssonalidhanokar9784100% (2)