You might also like

- Avenue Supermarts LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesAvenue Supermarts LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Coal India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument2 pagesCoal India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Vindhya Telelinks LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument2 pagesVindhya Telelinks LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Aurobindo Pharma LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument10 pagesAurobindo Pharma LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Reliance Industries Rights Issue Update - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument2 pagesReliance Industries Rights Issue Update - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Inox Wind LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesInox Wind LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- V I P Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument4 pagesV I P Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Update On Government Stimulus Package - Part 1 - Size of Economic Package, Stock Recommendations, Total Stimulus Etc - Angel BrokingDocument4 pagesUpdate On Government Stimulus Package - Part 1 - Size of Economic Package, Stock Recommendations, Total Stimulus Etc - Angel Brokingmoisha sharmaNo ratings yet

- Bata India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesBata India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Nestle India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument4 pagesNestle India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Sun Pharmaceuticals Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesSun Pharmaceuticals Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Ashok Leyland LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesAshok Leyland LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Parag Milk Foods LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesParag Milk Foods LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- KEI Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesKEI Industries LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Axis Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesAxis Bank LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- AngelTopPicks (April 2020) - List of Company Profiles, Performance Report, Stock Info & Key Financials - Angel BrokingDocument10 pagesAngelTopPicks (April 2020) - List of Company Profiles, Performance Report, Stock Info & Key Financials - Angel Brokingmoisha sharmaNo ratings yet

- Safari Industries (India) LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesSafari Industries (India) LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Maruti Suzuki India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesMaruti Suzuki India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Mahindra & Mahindra LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesMahindra & Mahindra LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- IRCTC - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesIRCTC - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Affle (India) LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesAffle (India) LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Amber Enterprises India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesAmber Enterprises India LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Blue Star LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument9 pagesBlue Star LTD - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Spandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesSpandana Sphoorty Financial Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- CSB Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesCSB Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Ujjivan Small Finance Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument7 pagesUjjivan Small Finance Bank - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Prince Pipes & Fittings Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument8 pagesPrince Pipes & Fittings Limited - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- Sterling & Wilson Solar LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesSterling & Wilson Solar LTD - Company Profile, Issue Details, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cipla LTD: Company AnalysisDocument13 pagesCipla LTD: Company AnalysisDante DonNo ratings yet

- Solution Manual For Introduction To Accounting An Integrated Approach 6th Edition by AinsworthDocument6 pagesSolution Manual For Introduction To Accounting An Integrated Approach 6th Edition by Ainswortha755883752No ratings yet

- Dividend Policy AfmDocument10 pagesDividend Policy AfmPooja NagNo ratings yet

- Introduction To: Corporate Finance Institute®Document101 pagesIntroduction To: Corporate Finance Institute®df100% (2)

- Working Capital Project ReportDocument91 pagesWorking Capital Project ReportSupash AlawadiNo ratings yet

- Business Studies - XII: Financial Markets ExplainedDocument30 pagesBusiness Studies - XII: Financial Markets ExplainedThe stuff unlimitedNo ratings yet

- Financial Results For The Year 2019 20Document35 pagesFinancial Results For The Year 2019 20Akshaya SwaminathanNo ratings yet

- Working Capital Management Test BankDocument10 pagesWorking Capital Management Test BankLawrence Guzman83% (6)

- Exercises On Stock Valuation With AnswersDocument6 pagesExercises On Stock Valuation With AnswersfatehahNo ratings yet

- Balance Sheet - Ratio AnalysisDocument49 pagesBalance Sheet - Ratio AnalysisKarishmaAshuNo ratings yet

- Specialised Accouning Ques BankDocument31 pagesSpecialised Accouning Ques BankMayra AzharNo ratings yet

- QUICK STUDY 12-1 True Statement: 1,3 and 4Document3 pagesQUICK STUDY 12-1 True Statement: 1,3 and 4denixngNo ratings yet

- An Evaluation of Contractors' Satisfaction With Payment Terms Influencing Construction Cash FlowDocument10 pagesAn Evaluation of Contractors' Satisfaction With Payment Terms Influencing Construction Cash Flowjacom0811No ratings yet

- Muhammad Kashif Raheem 5212 Cost Accounting Sir Naveed AlamDocument8 pagesMuhammad Kashif Raheem 5212 Cost Accounting Sir Naveed AlamKashif RaheemNo ratings yet

- Portfolio Management in IndiaDocument12 pagesPortfolio Management in IndiaiammonelNo ratings yet

- ITC Financial AnalysisDocument21 pagesITC Financial AnalysisDeepak ChandekarNo ratings yet

- 978 613 9 45336 8Document325 pages978 613 9 45336 8drmadhav kothapalliNo ratings yet

- QP Preboard Term 1 Accounts 2021-22Document22 pagesQP Preboard Term 1 Accounts 2021-22dev sharmaNo ratings yet

- Negotiating The Term SheetDocument21 pagesNegotiating The Term SheetDaniel100% (6)

- Tata Motors raises $750m through GDRs and CBsDocument2 pagesTata Motors raises $750m through GDRs and CBsabhiphadkeNo ratings yet

- Private Equity Cheat Sheet Bloomberg TerminalDocument1 pagePrivate Equity Cheat Sheet Bloomberg TerminalAmuyGnopNo ratings yet

- May 23 G1 RTPDocument122 pagesMay 23 G1 RTPMeet BaradNo ratings yet

- M.K Prof. KamaludinDocument21 pagesM.K Prof. Kamaludinwulan akayuanaNo ratings yet

- Assignment: Strategic Financial ManagementDocument7 pagesAssignment: Strategic Financial ManagementVinod BhaskarNo ratings yet

- Review of RatiosDocument5 pagesReview of RatiosJames AlievNo ratings yet

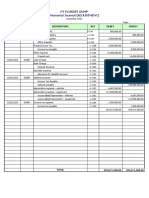

- PT Florist Gump December 2020 Financial StatementDocument9 pagesPT Florist Gump December 2020 Financial StatementSu MiniNo ratings yet

- Chap 7Document27 pagesChap 7Joanne Chau100% (1)

- Midterm - Quiz - AEC6Document4 pagesMidterm - Quiz - AEC6aprilNo ratings yet

- 2018 Interims Manual of AccountingDocument118 pages2018 Interims Manual of AccountingGherasim BriceagNo ratings yet

- MODULE 8 Capital BudgetingDocument16 pagesMODULE 8 Capital BudgetingKatrina Peralta FabianNo ratings yet