You might also like

- Forest Products: Advanced Technologies and Economic AnalysesFrom EverandForest Products: Advanced Technologies and Economic AnalysesNo ratings yet

- D8Document11 pagesD8neo14100% (1)

- University of Perpetual Help System Dalta: Calamba Campus, Brgy. Paciano RizalDocument6 pagesUniversity of Perpetual Help System Dalta: Calamba Campus, Brgy. Paciano RizalJeanette Lampitoc100% (2)

- This Study Resource Was: InventoriesDocument3 pagesThis Study Resource Was: InventoriesKim TanNo ratings yet

- Ia MidtermDocument4 pagesIa MidtermJim LubianoNo ratings yet

- Review Handouts and Materials: Semester First Semester School Year 2019-2020 Subject Handout # TopicDocument34 pagesReview Handouts and Materials: Semester First Semester School Year 2019-2020 Subject Handout # TopicWilson TanNo ratings yet

- Review 105 - Day 9 Theory of AccountsDocument12 pagesReview 105 - Day 9 Theory of AccountsKathleen PardoNo ratings yet

- Pas 2 InventoryDocument3 pagesPas 2 InventoryHardly Dare GonzalesNo ratings yet

- D7Document11 pagesD7neo14No ratings yet

- Review 105 - Day 7 Theory of AccountsDocument11 pagesReview 105 - Day 7 Theory of AccountsKathleen PardoNo ratings yet

- 09 - Inventories - TheoryDocument3 pages09 - Inventories - Theoryjaymark canayaNo ratings yet

- AC and VCDocument3 pagesAC and VCMila Casandra CastañedaNo ratings yet

- Inventory and LCNRV Theories MCDocument2 pagesInventory and LCNRV Theories MCYvan KimNo ratings yet

- PAS 02 InventoryDocument8 pagesPAS 02 InventoryRia GayleNo ratings yet

- D9Document11 pagesD9Saida MolinaNo ratings yet

- Pas 2 Inventory Practice Exercise For Pas 2 InventoriesDocument8 pagesPas 2 Inventory Practice Exercise For Pas 2 InventoriesSalimNo ratings yet

- Quiz 3 Conceptual Framework 0 Accounting Standards Answer KeyDocument5 pagesQuiz 3 Conceptual Framework 0 Accounting Standards Answer Keymaliaerica738No ratings yet

- Quiz 4 - With Answers Part IIDocument6 pagesQuiz 4 - With Answers Part IIjanus lopezNo ratings yet

- Quiz 3 - Intacc 2Document8 pagesQuiz 3 - Intacc 2Eleina SwiftNo ratings yet

- FA6Document2 pagesFA6KirosTeklehaimanotNo ratings yet

- Drill Prelim To FinalsDocument7 pagesDrill Prelim To FinalsMila Casandra CastañedaNo ratings yet

- InventoriesDocument6 pagesInventoriesheythereitsclaireNo ratings yet

- BSIE Cost AccountingDocument5 pagesBSIE Cost AccountingJoovs JoovhoNo ratings yet

- CFAS 2020 Chapter 15 and MC ProblemsDocument7 pagesCFAS 2020 Chapter 15 and MC Problems4220019No ratings yet

- Practice Set-Inventory (THEORY)Document5 pagesPractice Set-Inventory (THEORY)polxrixNo ratings yet

- Cost Acctg Absorption QuizDocument5 pagesCost Acctg Absorption QuizNah HamzaNo ratings yet

- D14Document12 pagesD14YaniNo ratings yet

- 15 Responsibility Accounting andDocument17 pages15 Responsibility Accounting andmaria ronoraNo ratings yet

- 01 CACM1 4finals PDFDocument8 pages01 CACM1 4finals PDFRonel A GaviolaNo ratings yet

- Pas 2Document4 pagesPas 2Cristine Jane Granaderos OppusNo ratings yet

- Mas 4Document6 pagesMas 4Krishia GarciaNo ratings yet

- Cagayan - Batch 2Document22 pagesCagayan - Batch 2Sarah BalisacanNo ratings yet

- Intermediate Accounting 1Document18 pagesIntermediate Accounting 1Shaina Jane LibiranNo ratings yet

- Inventories ThoeryDocument10 pagesInventories ThoeryAltessa Lyn ContigaNo ratings yet

- Answer-Key Acco-201 Intacc2 Mte 1say2324Document8 pagesAnswer-Key Acco-201 Intacc2 Mte 1say2324John cookNo ratings yet

- Responsibility Accounting and Transfer Pricing CTDI October 2016 IMDocument17 pagesResponsibility Accounting and Transfer Pricing CTDI October 2016 IMFerdi LlasosNo ratings yet

- Conceptual FrameworkDocument4 pagesConceptual FrameworkVenus PalmencoNo ratings yet

- AC1011.7.1 Midterm Examinations Questions and AnswersDocument20 pagesAC1011.7.1 Midterm Examinations Questions and AnswersrheaNo ratings yet

- Pas 2 InventoryDocument8 pagesPas 2 InventoryMark Lord Morales BumagatNo ratings yet

- Absorption & Variable CostingDocument1 pageAbsorption & Variable CostingAthNo ratings yet

- Quiz 4 - With AnswersDocument6 pagesQuiz 4 - With Answersjanus lopezNo ratings yet

- Intangible Assets PDFDocument9 pagesIntangible Assets PDFFery AnnNo ratings yet

- Quiz-Inventory TheoryDocument4 pagesQuiz-Inventory TheoryCaila Nicole ReyesNo ratings yet

- Ias 2 Test Bank PDFDocument11 pagesIas 2 Test Bank PDFAB Cloyd100% (1)

- TOA2 - (Cost Accounting - SMEs Advanced Accounting) With Answer KeyDocument35 pagesTOA2 - (Cost Accounting - SMEs Advanced Accounting) With Answer KeySophia Christina BalagNo ratings yet

- Chapter 8 OkDocument37 pagesChapter 8 OkMa. Alexandra Teddy Buen0% (1)

- Chapter 8 Quiz - InventoriesDocument8 pagesChapter 8 Quiz - InventoriesDarleen CantiladoNo ratings yet

- Pas 2 Inventories Accounting Standard That Is Useful in Understanding Financial Accounting ReportingDocument9 pagesPas 2 Inventories Accounting Standard That Is Useful in Understanding Financial Accounting ReportingJANISCHAJEAN RECTONo ratings yet

- Bs. Accountancy (Aklan State University) Bs. Accountancy (Aklan State University)Document9 pagesBs. Accountancy (Aklan State University) Bs. Accountancy (Aklan State University)JANISCHAJEAN RECTONo ratings yet

- FA2Document2 pagesFA2KirosTeklehaimanotNo ratings yet

- Material 3 PDF FreeDocument6 pagesMaterial 3 PDF FreeIshi Erika OrtizNo ratings yet

- 09 Chapter # 9 - Inventories PDF Cost of Goods Sold InventoryDocument1 page09 Chapter # 9 - Inventories PDF Cost of Goods Sold InventoryZKS EditsNo ratings yet

- Theory On PPEDocument1 pageTheory On PPEExcelsia Grace A. ParreñoNo ratings yet

- 209384Document9 pages209384Vher Christopher DucayNo ratings yet

- Absorption CostingDocument22 pagesAbsorption CostingLeanFlor SegundinoNo ratings yet

- Cost Concepts and ClassificationsDocument19 pagesCost Concepts and ClassificationssarahbeeNo ratings yet

- Acdc MCQDocument4 pagesAcdc MCQCherryjane RuizNo ratings yet

- Recent Trends in Valuation: From Strategy to ValueFrom EverandRecent Trends in Valuation: From Strategy to ValueLuc KeuleneerNo ratings yet

- Sources of Obligation - Oblicon Lecture and Notes 1Document15 pagesSources of Obligation - Oblicon Lecture and Notes 1Francis SantosNo ratings yet

- Sources of Obligation - Oblicon Lecture and Notes 1Document15 pagesSources of Obligation - Oblicon Lecture and Notes 1Francis SantosNo ratings yet

- Revenue Total Expenses Ebitda Depreciation EbitDocument2 pagesRevenue Total Expenses Ebitda Depreciation EbitFrancis SantosNo ratings yet

- Intro and Summary Written Document CH5Document3 pagesIntro and Summary Written Document CH5Francis SantosNo ratings yet

- Intro and Summary Written Document CH5Document3 pagesIntro and Summary Written Document CH5Francis SantosNo ratings yet

- NIL III. Negotiation Sec. 30-50Document18 pagesNIL III. Negotiation Sec. 30-50Francis SantosNo ratings yet

- Sociological Perspective: The Self As A Product of SocietyDocument14 pagesSociological Perspective: The Self As A Product of SocietyFrancis SantosNo ratings yet

- CHP 7 Strategy and StructureDocument21 pagesCHP 7 Strategy and StructureBBHR20-A1 Wang Jing TingNo ratings yet

- Mahindra Logistics Ltd-1Document4 pagesMahindra Logistics Ltd-1Ashish GowdaNo ratings yet

- Product CategoryDocument5 pagesProduct CategoryAaon EnterprisesNo ratings yet

- The Dynamics of Windfall Taxation System20092Document9 pagesThe Dynamics of Windfall Taxation System20092Mouni SheoranNo ratings yet

- RecruitmentDocument11 pagesRecruitmentThushara VinayNo ratings yet

- Strategy MapDocument24 pagesStrategy MapRichard JavierNo ratings yet

- Aakash Sharma: Career ObjectiveDocument3 pagesAakash Sharma: Career ObjectiveAAKASH SHARMANo ratings yet

- CHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebDocument6 pagesCHAPTER 4: Differential Cost Analysis (Relevant Costing) KaebMark Gelo WinchesterNo ratings yet

- Evergreen Corporation: Sti College Santa Rosa, LagunaDocument16 pagesEvergreen Corporation: Sti College Santa Rosa, LagunaChristine Joyce Magote100% (1)

- Assignment For 10 Points Each, Answer The FollowingDocument2 pagesAssignment For 10 Points Each, Answer The FollowingJohn Phil PecadizoNo ratings yet

- PMP QuestionDocument84 pagesPMP Questionrashdan rosmanNo ratings yet

- Solved Bonnie Opens A Computer Sales and Repair Service During The PDFDocument1 pageSolved Bonnie Opens A Computer Sales and Repair Service During The PDFAnbu jaromiaNo ratings yet

- Managerial Accounting Tools For Business Decision Making 7Th Edition Weygandt Solutions Manual Full Chapter PDFDocument63 pagesManagerial Accounting Tools For Business Decision Making 7Th Edition Weygandt Solutions Manual Full Chapter PDFcomplinofficialjasms100% (13)

- HKB 18 Manpowerpolicy InwardremittancesDocument50 pagesHKB 18 Manpowerpolicy InwardremittancesFahimNo ratings yet

- TDW PIGG SpecificationsDocument157 pagesTDW PIGG SpecificationsKhwanas LuqmanNo ratings yet

- Strategy Formulation, Business StrategyDocument29 pagesStrategy Formulation, Business StrategyMohamed SalahNo ratings yet

- Advantages of Online ShoppingDocument5 pagesAdvantages of Online ShoppingPatrickNo ratings yet

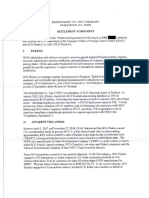

- Scgplastics SettlementDocument5 pagesScgplastics SettlementTCIJNo ratings yet

- Sober Living Home Business PlanDocument22 pagesSober Living Home Business PlanAdrianaZarate89% (28)

- Gap Inc. Case Study: Quality and Productivity Through TrustDocument10 pagesGap Inc. Case Study: Quality and Productivity Through TrustJennilyn HenaresNo ratings yet

- Samsung Mobile Devices: Running Head: Final Strategic Plan 1Document21 pagesSamsung Mobile Devices: Running Head: Final Strategic Plan 1Darryn Urueta50% (2)

- Entrepreneurship Quarter 1 - Module 1 Overview of EntrepreneurshipDocument18 pagesEntrepreneurship Quarter 1 - Module 1 Overview of EntrepreneurshipBert Batoon MonteNo ratings yet

- Beiersdorf Equity Story FY 2022Document19 pagesBeiersdorf Equity Story FY 2022linna ismawatiNo ratings yet

- Is It Ever OK To Break A Promise?: Executive SummaryDocument7 pagesIs It Ever OK To Break A Promise?: Executive SummaryNamit BaserNo ratings yet

- Correctional Administration Q & ADocument62 pagesCorrectional Administration Q & AClarito Lopez100% (26)

- ASM1 - 530 - Global Business EnvironmentDocument19 pagesASM1 - 530 - Global Business EnvironmentBảo Trân Nguyễn NgọcNo ratings yet

- Ifc 8thconf 4c4papDocument29 pagesIfc 8thconf 4c4papgauravpassionNo ratings yet

- Chapter 02 - CONCEPTUAL FRAMEWORK: Objective of Financial ReportingDocument6 pagesChapter 02 - CONCEPTUAL FRAMEWORK: Objective of Financial ReportingKimberly Claire AtienzaNo ratings yet

- Design Thinking AssignmentDocument3 pagesDesign Thinking AssignmentOpeyemi OyewoleNo ratings yet

- e-StatementBRImo 714201036008532 Dec2023 20231227 164433Document5 pagese-StatementBRImo 714201036008532 Dec2023 20231227 164433umiyahraditNo ratings yet